by Chris Becker

Asian stocks were mixed in response to the poor lead from Wall Street overnight with all eyes on the RBA today seeing the Aussie dollar spike above 76 cents against the USD. Chinese data also surprised to the upside, but domestic stocks aren’t having it with risk off the table going into Friday nights NFP print.

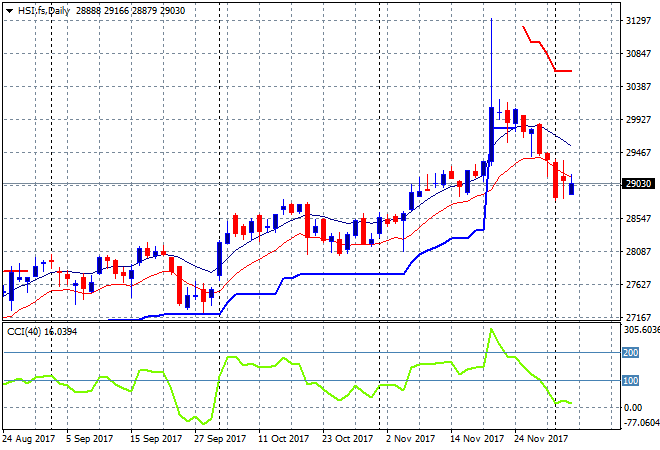

In mainland China the Shanghai Composite is clinging desperately to support at 3300 points, down 0.2% to be just above at 3302. If it breaks, the 3200 level beckons quite fast. The Hang Seng Index is playing catch up after gapping down to the Friday close, its recovered somewhat, but still down nearly 0.6% or 180 points to be back below the 29000 point level. As I said yesterday, the lack of a new daily or session high is telling here with the target still down to support at the 28500 level:

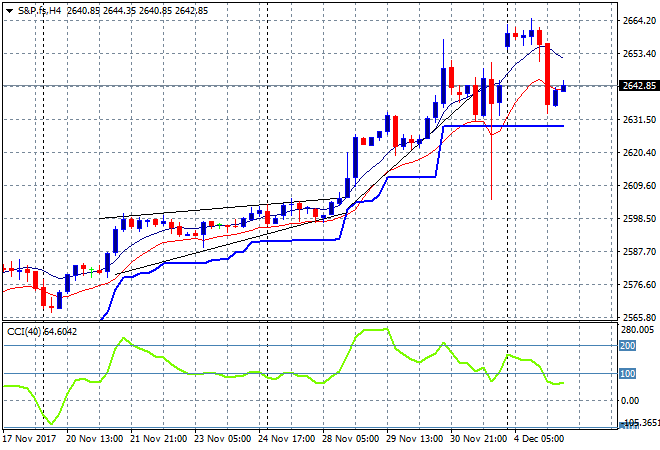

S&P futures have come back slightly but its relative given the slump overnight, with all eyes on tech stocks. The ATR trailing support level at 2630 must remain firm here:

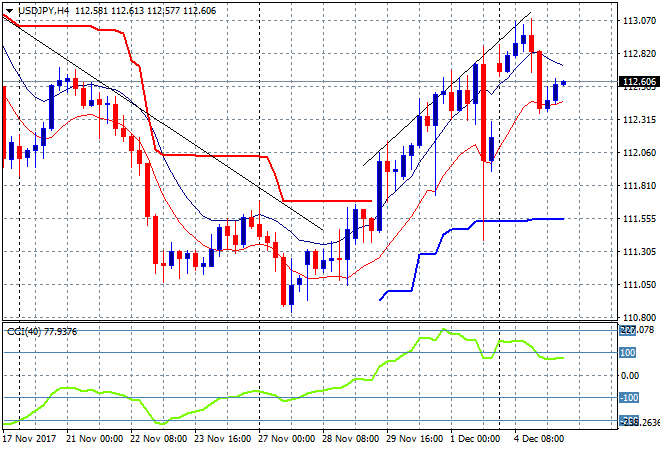

Japanese stocks were mixed given the reaction to the overnight strengthening in Yen, as the broader TOPIX gained, the Nikkei closed 0.4% lower to 22622 points, continuing to retrace its previous gains and setting up a potential bearish double top pattern on the daily chart. The USDJPY pair recovered about half of its overnight losses, getting back to the 112.60 level but looking weak here going into some strong economic data prints tonight:

The ASX200 gapped down at the open on the poor lead from Wall Street but recovered to finish slightly off, down 0.2% to 5971 points. The 6000 point level is proving strong resistance and the inability to make a new daily high is starting to weigh on the market.

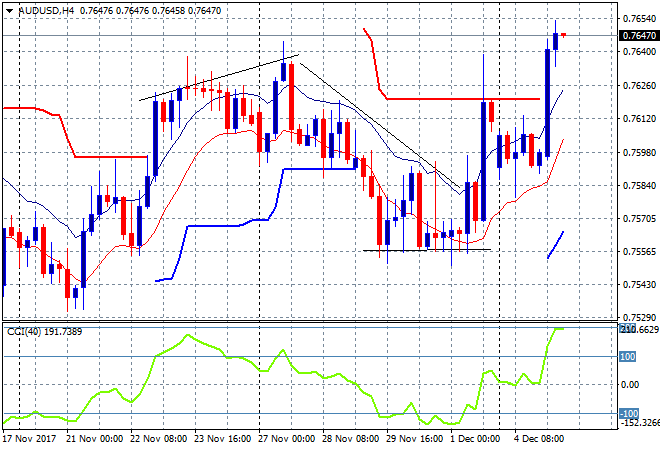

The Australian dollar has shot ahead on the lack of any easing suggestions by the RBA, bursting straight through the 76 handle against USD plus making a new three week high. While this is overdone and a short term retracement is to be expected, we could be in for a new run back up to the daily resistance level at 77 cents:

The data calendar has a slew of lower tier preliminary releases in Europe to wade through, plus the fallout from the Brexit talks, but the big one tonight is US services PMI print for November.