It is true that the October rise in employment was softer than expected, +3.7k vs market expectations of an 18k rise, but this should be put into context that October was the 13th consecutive monthly rise in total employment. This is longest stretch of positive employment prints since the run of 15 months from May 1993. The next longest run was 14 consecutive months from August 1979. As such it is not surprising that there are expectations for a negative print sometime soon, even just from survey volatility.

However, we are not going to pick some random month for this to occur even more so given that October was a soft month for both employment and participation which may have been a signal that sample volatility was behind the softer number. For more information please see our October Labour Force Economic Bulletin.

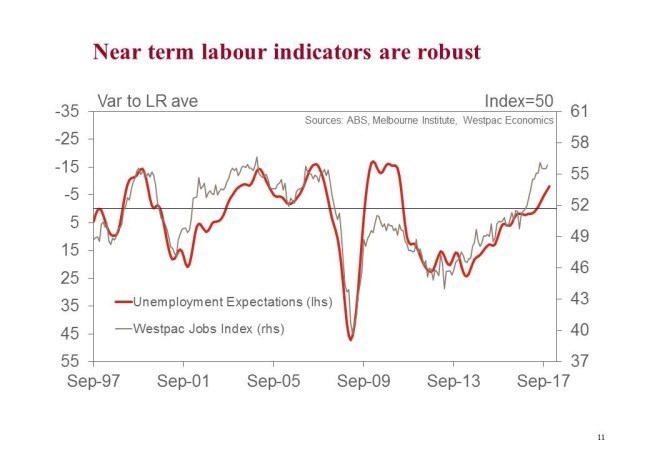

Westpac’s Job’s Index is currently poiting to an annual pace of employment growth around 2.6%yr and it suggest that it can hold this pace well into Q2 2018. In the October Labour Force Survey total employment growth was running around 3.0%yr, a bit higher than the Jobs Indexis pointing to but not out of the bound of the normal volatility in this relationship.

In addition, the Westpac/Melbourne Institute Unemployment Expectations Index (remember rising unemployment expectations suggest that household are expecting a deterioration in labour market conditions) have fallen 8.2% in the year to December taking the trend to 8% below the 10 years average, a very strong signal that household are experiencing a robust labour market. The last time the index was stronger than this was the –12% print back in April 2011.

For these reasons we are not looking for any meaningful moderation in the pace of employment growth. Our above market forecast for a 25k rise in employment will see the annual pace of growth ease back a touch to 2.8% year and the three month average change drop a touch to +21.7k in November from +23.3k in October.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.