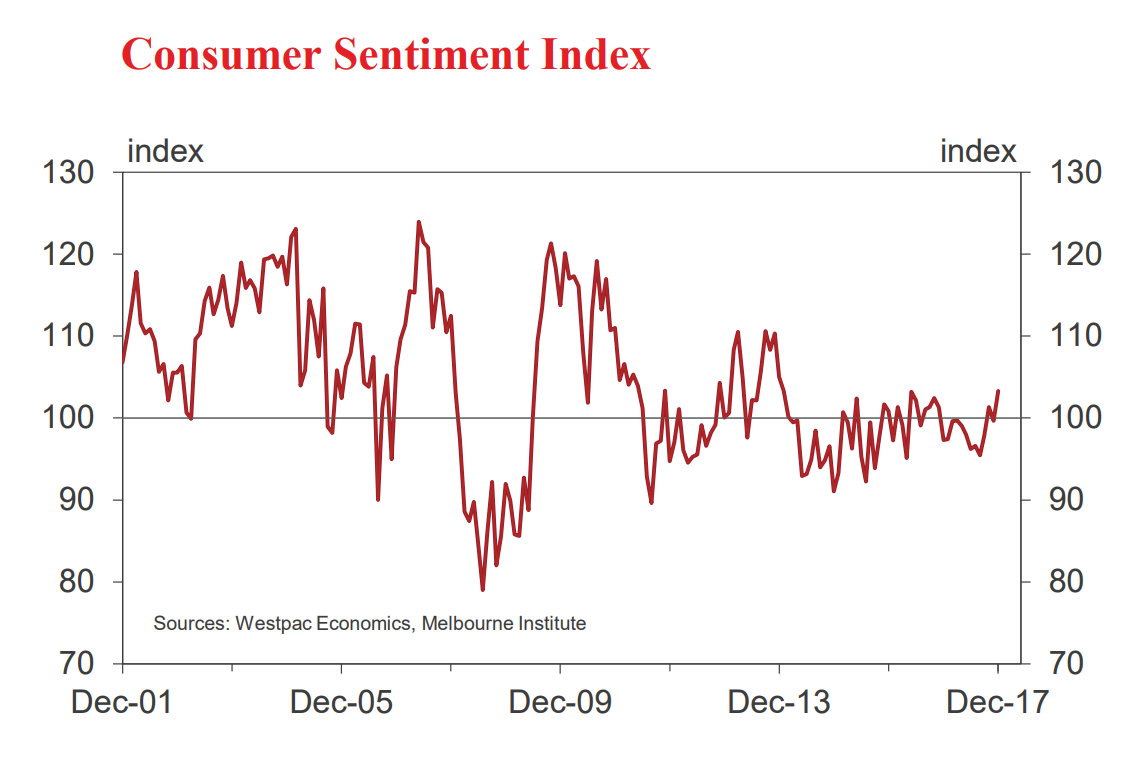

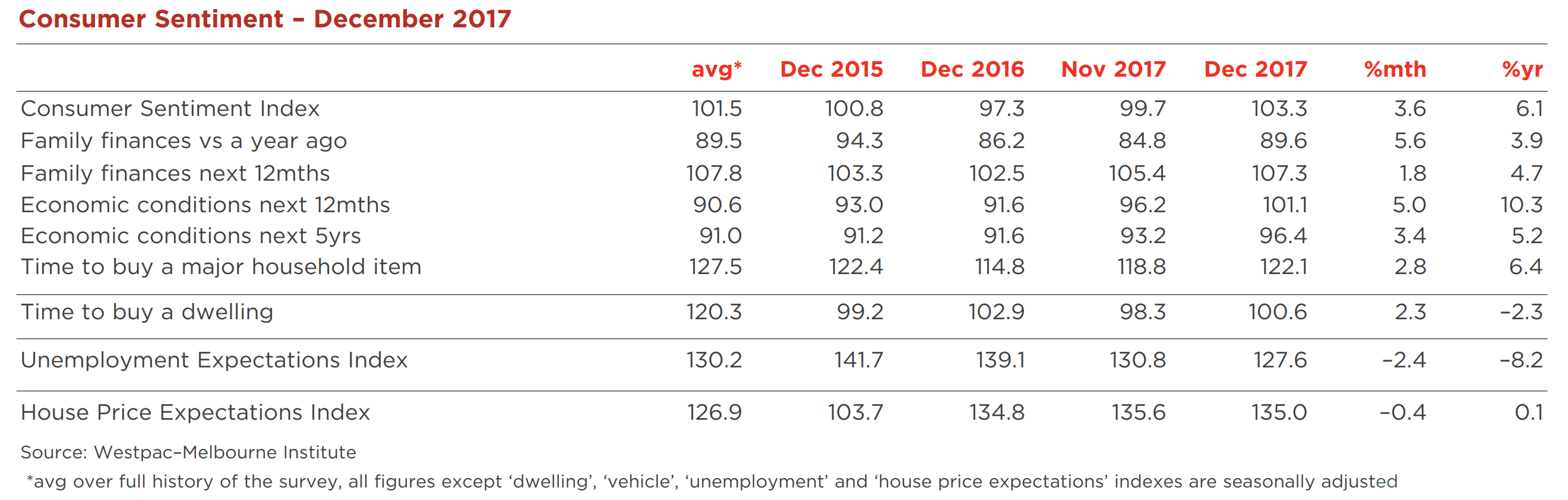

• The Westpac Melbourne Institute Index of Consumer Sentiment rose 3.6% to 103.3 in December from 99.7 in November.

This is a surprisingly strong result and confirms the lift we have seen in the Index over the last three months. The average reading for the Index in the December quarter is 5% above the average for the September quarter when we saw a disturbing slump in consumer spending. This result is supportive of the view that consumer confidence may have bottomed out during that September quarter.

In turn, growth in consumer spending is likely to have also bottomed out in the September quarter. However, with ongoing weak income growth; a low savings rate; and high debt levels we cannot be confident that consumers have the capacity to sharply lift spending despite higher confidence.

A less threatening outlook for interest rates appears to have boosted confidence. During that September quarter households were spooked by media and many commentators saying that interest rates were likely to start rising in the new year. That effect has now calmed down significantly.

Also supporting a more positive assessment for respondents’ finances is coverage of the government’s recent speculation around possible tax cuts.

With the labour market remaining strong respondents are generally more confident about the domestic economy and there is likely to have been a ‘feelgood effect’ from the passing of marriage equality legislation.

Media coverage of tax cuts in the US combined with easing tensions in North Korea, may also be supporting an improved outlook for international conditions.

All five components of the Index improved in December. Responses on family finances support the assessment around interest rates and tax cuts although it is unlikely that respondents are experiencing any relief in terms of wage increases. The ‘finances vs a year ago’ sub-index posted the biggest gain, rising 5.6% to 89.6 – an 18 month high but still well below the 100 mark indicating more consumers are seeing their finances deteriorate than improve. The forward view continues to be more positive the ‘finances, next 12mths’ sub-index posted a further 1.8% rise to 107.3, the most positive reading in a little over two years.

Views on the economy also posted solid gains, the ‘economic conditions, next 12 months’ sub-index rose 5% and the ‘economic outlook over the next five years’ sub-index was up 3.4%.

The ‘time to buy a major household item’ sub-index rose 2.8% but at 122.1 remains well below the long run average of 127.5 and still pointing to subdued consumer spending plans for the Christmas period. 13 December 2017

The December survey included additional questions on news recall that provide insight into the factors shaping sentiment. Overall, recall levels were again low suggesting consumers are getting less exposure to news in general. The highest recall rates were for news on ‘economic conditions’ (19%); ‘budget and taxation’ (19%); interest rates (19%); inflation (10%); jobs (10%); and international conditions (9%). News on all of these topics was viewed as more favourable than three months ago, with particularly big improvements around international conditions, the economy and interest rates.

Consumers continue to become more comfortable about the outlook for jobs. The Westpac Melbourne Institute Unemployment Expectations Index declined 2.4% to 127.6 in December, the index reaching its lowest level since May 2011 (recall that lower reads mean more consumers expect unemployment to fall in the year ahead). The index can be viewed as a measure of consumers’ sense of job security. Qld consumers showed a particularly big improvement in December. Notably, all major states now have index reads below their long run averages, meaning consumer expectations for labour markets are marginally better than average.

The ‘time to buy a dwelling’ index rose 2.3% to 100.6, the first reading over 100 since the start of the year. The state detail continues to show materially weaker reads in NSW (90) and Vic (88) as affordability remains a constraint whereas there are much more positive assessments in Qld (121) and WA (122).

The Westpac Melbourne Institute Index of House Price Expectations edged 0.4% lower to 135. Price expectations continue show a sharp slide in NSW where the state index fell a further 12% in December to be down by 24% over the year. In contrast the Vic index was up 2% for the month and 10% for the year, with Qld and WA posting strong gains in the month (up 8% and 9% respectively). The variations mainly reflect the sharper slowdown in price growth evident in the Sydney market.

Responses to additional questions on the ‘wisest place for savings’ continue to indicate high levels of risk aversion. Nearly two thirds of consumers still favour safe options – deposits, superannuation or paying down debt – with only 12.8% nominating real estate and 8% nominating shares. About the same proportion of consumers favour ‘pay down debt’ (20.4%) as favour real estate and shares combined.

The Reserve Bank Board next meets on February 6. As discussed above, markets and general commentary have cooled their fervour for rate hikes in 2018. In turn that has helped boost Consumer Sentiment along with other factors discussed above.

However we doubt whether this welcome lift to confidence will be sufficient to see the Bank achieve its ambitious growth forecast in 2018 of 3.25%. Constraints around incomes; savings; and debt are still likely to keep consumer spending growth below trend. T

he Bank’s forecasts for core inflation (1.75% in 2018) and the cooling in the Sydney property market (which is once again apparent in this survey) are also likely to be significant headwinds to higher interest rates.

We confirm our view that the cash rate is likely to remain on hold at 1.5% through 2018.

I wonder if the energy bill shock has faded a bit too. I agree that this is not a change in trend. If adjusted for where we are the business cycle, confidence is garbage.

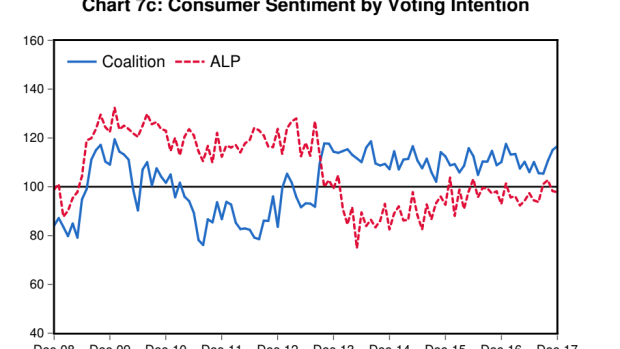

Then again, maybe its gay marriage as the lift was driven entirely by Coalition voters:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.