Chinese manufacturing sector operating conditions continued to improve in November, albeit at a marginal pace. Output and new orders both rose only modestly, leading to a softer expansion in buying activity. At the same time, companies faced a further sharp increase in average input costs, that led to a notable rise in selling prices. Efforts to cut costs contributed to another fall in staffing levels, with the rate of decline quickening to a three-month record.

Subdued growth in new work and a sustained fall in employment coincided with a reduction in business confidence towards the one-year outlook. Notably, firms expressed the joint-weakest degree of optimism on record.

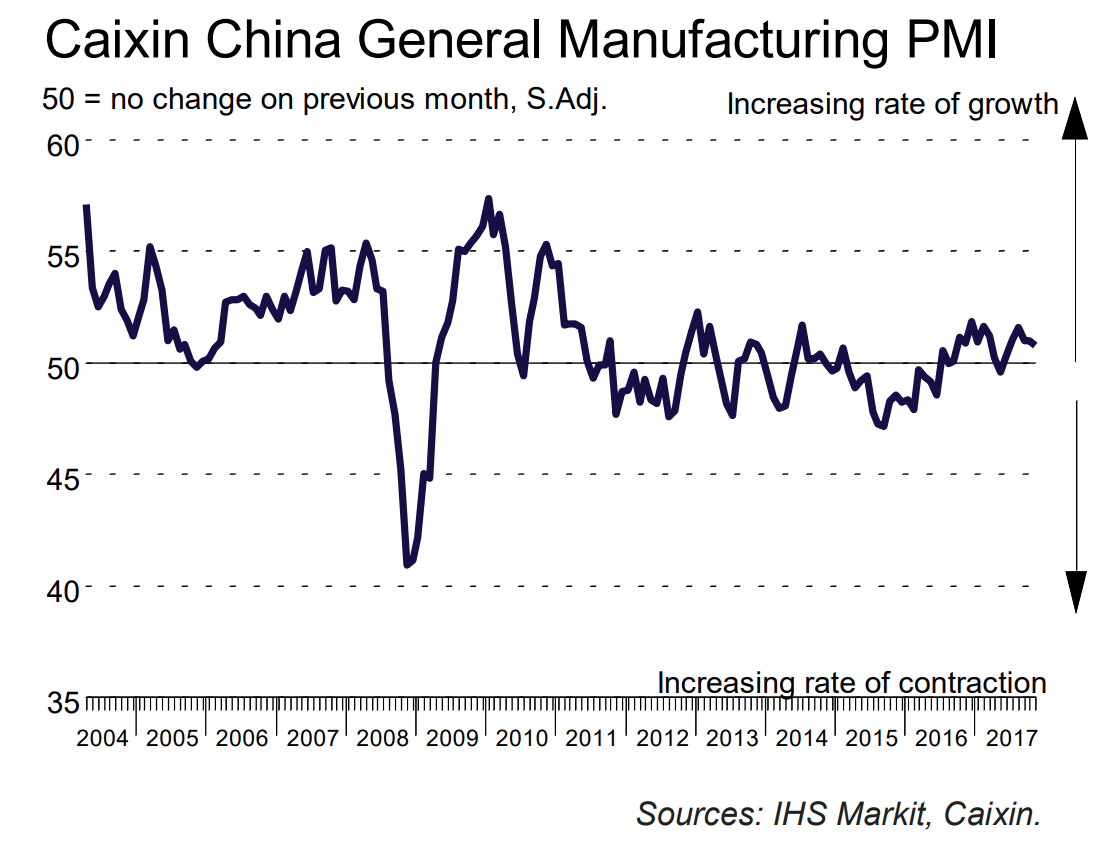

The seasonally adjusted Purchasing Managers’ Index™ (PMI™) – a composite indicator designed to provide a single-figure snapshot of operating conditions in the manufacturing economy – registered 50.8 in November, down from 51.0 in October. While remaining above the crucial 50.0 value, the index dipped to its lowest level for five months to signal only a marginal upturn in operating conditions.

Chinese goods producers continued to increase their production levels in November. Although the pace of expansion picked up slightly from October, the rate of growth was modest overall.

Total new orders rose at a similarly modest pace in November. Companies that registered higher new work commented on greater client bases and the launch of new products. Nonetheless, data indicated that client demand was relatively subdued across both the domestic and external markets, as new export sales also rose modestly.

As has been the case in each month since November 2013, staff numbers at Chinese manufacturers declined during November. Though modest, the rate of job shedding was the fastest seen in three months. As a result, companies registered a further increase in the amount of unfinished business at their units. The rate of backlog accumulation remained marked, despite softening since October.

Reflective of only modest growth in production, firms raised their buying activity marginally in November. At the same time, inventory levels of both purchased and finished items were little-changed from the previous month, as efforts to raise stock holdings at some firms were largely offset by more cautious inventory policies elsewhere.

Issues with logistics and stricter environmental policies added further pressure to supply chains in November. That said, the degree to which vendor performance deteriorated was the least marked for four months.

Difficulties in obtaining inputs alongside higher raw material prices in international markets underpinned a further sharp rise in input costs faced by Chinese manufacturers. As a result, companies raised their prices charged at a solid pace.

Relatively muted growth in new work coincided with weaker optimism towards the 12-month outlook for production. Notably, the degree of positive sentiment was the joint-weakest seen since the series began in April 2012.

More consistent with circumstantial evidence than the official version this month.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.