Via Westpac:

We confirm our forecast that the AUD will drift even lower in 2018 ending the year at around USD 0.70.

- Readers will be aware that one core driver of this expected deterioration in the AUD is our view that the overnight yield differential between Australia and the US will narrow significantly. Our target has been that by end 2018 the RBA overnight cash rate will be 38bps below the US Federal Funds. This dynamic is now well underway and is a key reason for the progressive weakening in the AUD in recent months.

Recall that in that 1999-2000 period when Australia’s overnight yield differential held below the US, the AUD eventually fell a precipitous 16c vs the USD compared to our current call of cumulative decline of around 12c in the current move.

- Currencies are not only affected by interest rate differentials and confidence.

- For Australia, commodity prices and the ongoing current account deficit are also important.

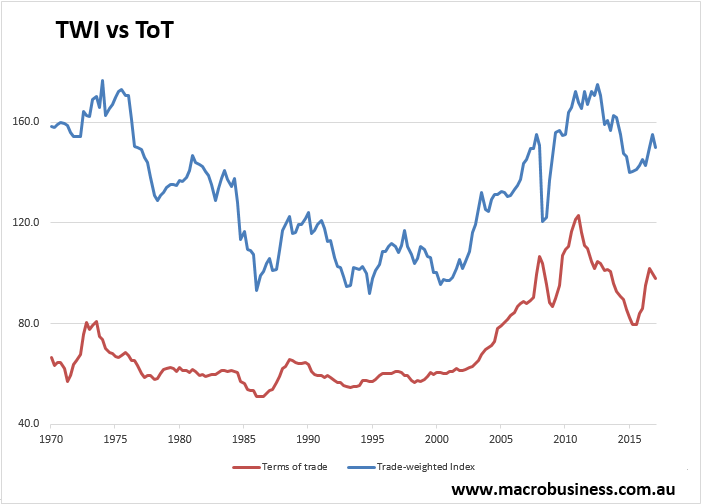

- Back in 1999-2000 Australia’s current account deficit was averaging around 5% of GDP. We expect that over the next two years the deficit will average nearer 2.5% of GDP, thanks of course to the emergence of China’s industrialisation miracle – indeed, despite Australia’s terms of trade are around 55% higher now than we saw during that last period of negative interest rate differentials.

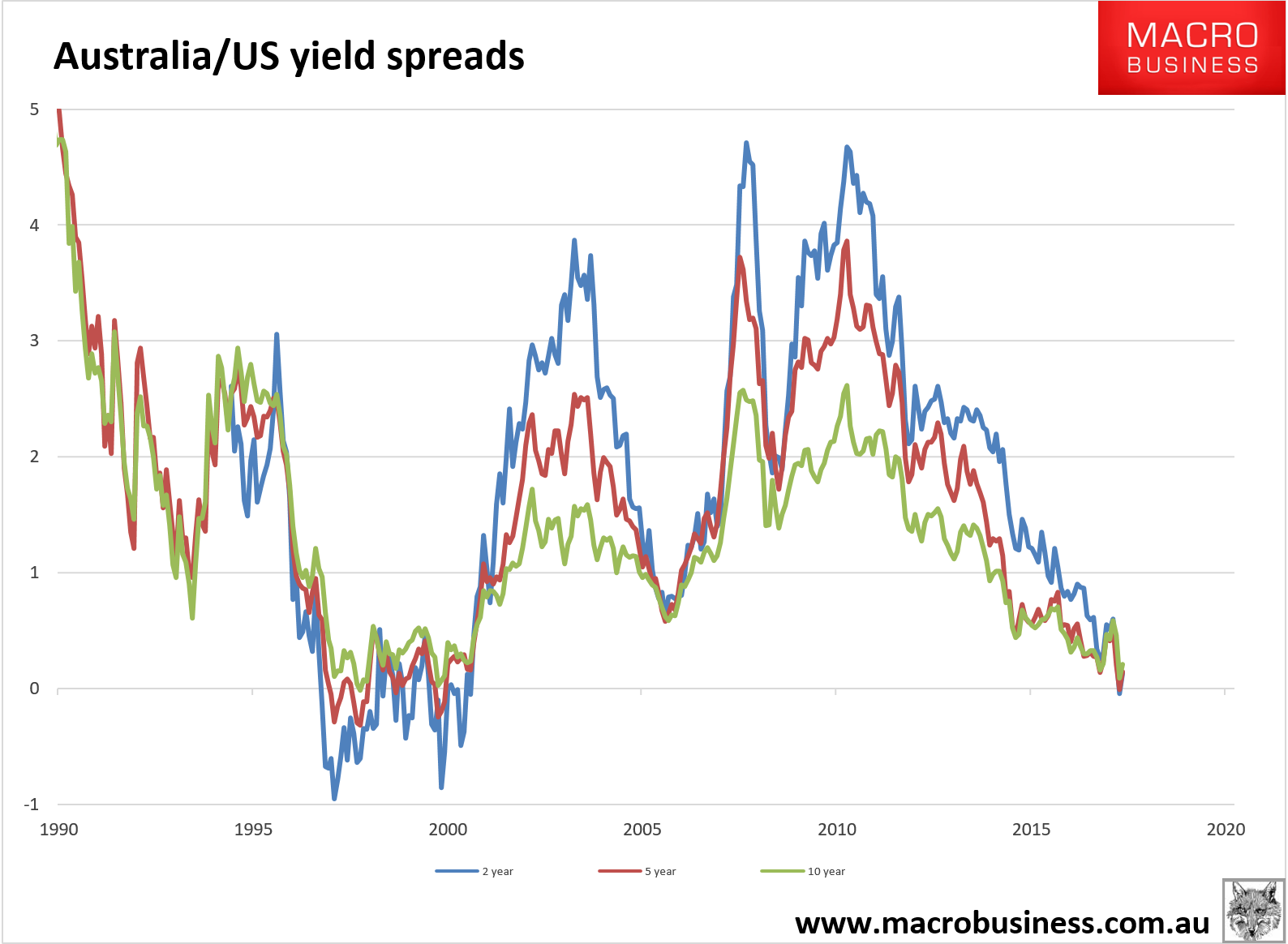

A couple of charts. The interest rate differential has recently rebounded to the positive but the trend is the Fed outpaces the RBA tightening:

And the terms of trade is also on its way down again. By this time next year we expect it to be materially lower, pressuring the AUD:

Where one goes, the other follows. Any rebound the AUD today should be treated as an opportunity to get offshore.

———————————————————————–

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long local bonds and international equities that offer superior growth and benefit from a falling AUD so he is definitely talking his book.

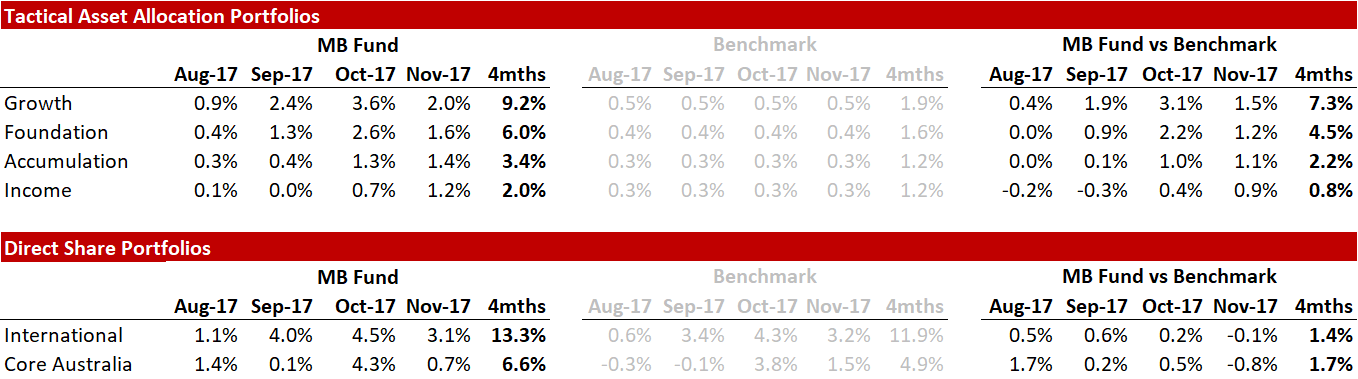

Here’s the recent fund performance:

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If the themes in this post and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.