Following passage of the Trump Administration’s tax package, the Business Council of Australia (BCA) and the Australian Chamber of Commerce and Industry (ACCI) have been quick to demand that Australia drop its corporate tax rate or place Australian investment and jobs at risk. From The Australian:

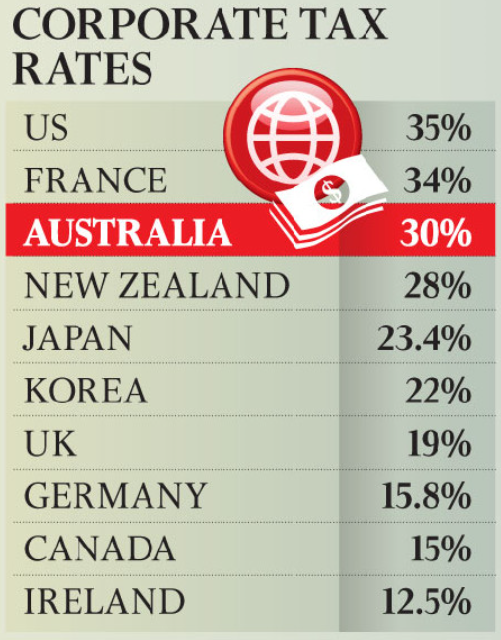

Australian businesses yesterday called for the opposition and crossbenchers to support the government’s stalled plan to cut the corporate tax rate from 30 per cent to 25 per cent, warning not to do so would put jobs and investment at risk…

The cuts would bring the US tax rate from above Australia’s 30 per cent to as much as a third lower, unless the Turnbull government’s enterprise tax plan to cut the rate to 25 per cent over 10 years is passed…

Business Council of Australia chief executive Jennifer Westacott said developments in the US tax system made the case for cuts to Australian company tax even more urgent.

“Safe-guarding Australian jobs, living standards and economic growth will require action to keep us competitive — the enterprise tax plan will help do that,” she said. “The IMF and Treasury are clear; without reform we will see capital sucked out of the Australian economy.”

Ms Westacott said business investment as a share of gross domestic product in Australia was already at its lowest level since the tail end of our last recession. “US reform will suck even more capital away from Australia,” she said.

Business tax cuts are estimated to cost the budget $50 billion, but new modelling from Treasury, backed by business surveys, indicates the cost will be offset by increased economic growth and the income flowing from new investment and job creation.

James Pearson, chief executive of the Australian Chamber of Commerce and Industry, said not passing the tax cuts risked jobs and the livelihoods of Australians.

“We know from experience that when Australian business tax rates are lowered, the budget is better off overall in just a few years,” he said…

Thankfully, economist Saul Eslake has been quick to hose down the business lobbyists’ arguments. Separately from The Australian:

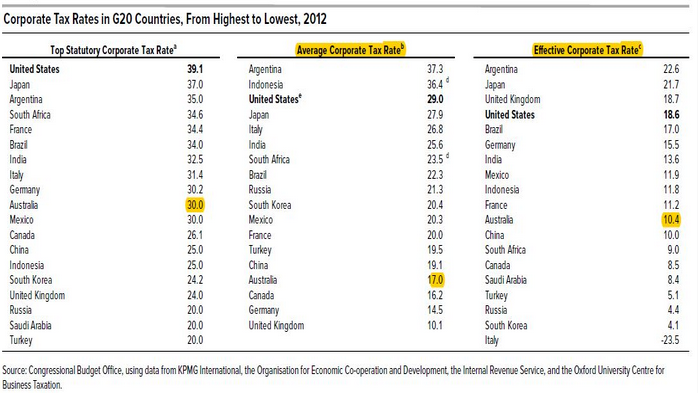

[Eslake] says a comparison of the headline rates in the US going from 35 per cent to 20 per cent under the Trump plan, which is being used to argue the case for cutting Australia’s corporate rate, is misleading.

A 2012 US Congressional Budget Office study found that at just 10.4 per cent Australia was in the bottom half of G20 economies for effective tax rates, which take into account investment allowances and depreciation rates. The average rate in Australia is 17 per cent…

Mr Eslake, Vice-Chancellor’s Fellow at the University of Tasmania and a former chief economist at both ANZ and Bank of America Merrill Lynch, says the primary beneficiaries of a cut in company tax rates in Australia will be the foreign shareholders of Australian companies and the majority owners of foreign interests.

“There is no guarantee that if they are allowed to keep more of their Australian earnings than they are at the 30 per cent tax rate that they would invest more of it in Australia,” Mr Eslake said.

Advertisement

Spot on. Here’s the US Congressional Budget Office’s analysis via Ian Verrender:

As you can see, Australia’s average and effective corporate tax rate is already competitive.

Advertisement

Fairfax’s Michael Pascoe has also done a good demolition job against the scaremongering over company tax cuts:

“Ze modelling! Ze modelling!” the Treasurer and BCA incant in desperate attempts to breathe life into their centrepiece reform policy – maybe their only reform policy – tax cuts for big business.

Our diminished Treasury’s modelling is promising higher wages in our times if we just follow the Trumpian promise of cutting company tax. According to BCA CEO Jennifer Westacott, ze modelling ze modelling “tells us a company tax cut delivers a higher pay-off than other ways of using the same taxpayers’ dollars”.

No, seriously, the BCA and ze modelling ze modelling reckon the very best way to spend $65 billion of your money over 10 years is on cutting the corporate tax rate – primarily the big business tax rate – from 30 to 25 per cent. According to ze modelling ze modelling, it would magically result in a net 1 per cent lift in GDP, $17 billion a year in today’s dollars…

If the BCA is genuine in asking how the money might be better spent, it might come up with such ideas as using the cash to bridge the income gap for states willing to swap our worst tax – stamp duty – for about the best tax, a no-exceptions land tax.

Or perhaps directly subsidising R&D instead of relying on vague and theoretical pledges by Big-End-of-Town CEOs to invest more if the tax rate was lower.

Or the Big Business lobby could at least propose some offsets – some healthy criticism of such lurks as the salary packaging industry’s bread and butter, my personal yardstick of fiscal integrity or lack thereof. But no – it’s purely ze modelling, ze modelling.

And there’s that other little problem: Treasury can model all it likes, but when the real-world examples aren’t there, it looks more than a little doctrinaire and dodgy…

A massive leap of faith is required to imagine the cargo cult play dropping billions of extra investment dollars.

How the Coalition’s company tax cut package would be funded is the threshold issue in this debate. According to the Australian Treasury’s initial modelling, released early last year, the full company tax cut package was estimated to cost the Budget some $8.2 billion a year. The Treasury’s more recent modelling, released last month, conveniently downgraded the cost of the Turnbull Government’s company tax cut package to around $4 billion a year.

Advertisement

Either way, this hefty cost to the Budget will need to be made up somehow, most likely by increasing the tax burden on workers.

And herein lies the fundamental problem with the Coalition’s company tax cut plan. The Treasury’s own modelling shows minimal benefits to either jobs or growth – primarily because the benefits flow to foreign business owners/shareholder – but a seismic shift in the tax burden from companies to individuals.

There are far better ways to use scarce taxpayer funds than this expensive lemon.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.