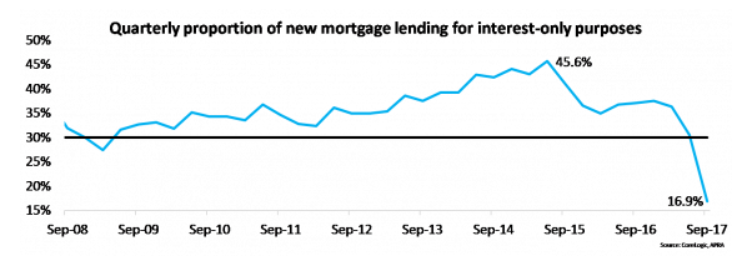

CoreLogic’s Cameron Kusher has published some interesting charts showing how the Australian Prudential Regulatory Authority’s (APRA) macro-prudential curbs on interest-only lending have been a major success, driving interest-only lending to record low levels:

The total value of interest-only lending over the September 2017 quarter was $16.603 billion which was -44.8% lower than the value over the June 2017 quarter and -52.8% lower than it was a year ago. We have recently seen the implementation on the cap of new interest-only lending, limiting it to 30% of new mortgages. Over the September 2017 quarter, interest-only mortgages accounted for 16.9% of new mortgage lending which was the lowest proportion on record and well down on the 30.5% the previous quarter. It is a little surprising to see the proportion of lending to investors fall so much over the quarter, especially considering that the cap is 30%. This potentially indicates that the higher mortgage rates being incurred by interest-only borrowers are actually curtailing demand more so than the cap.

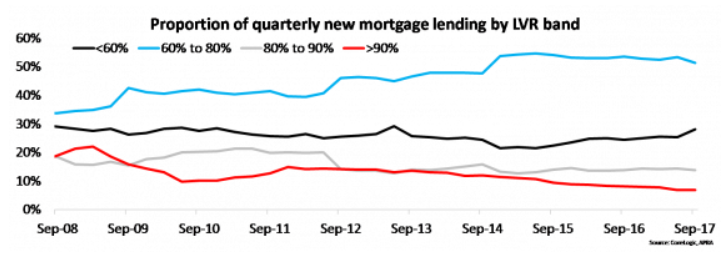

The changes to macroprudential policies has resulted in (not-surprisingly) more prudent borrowing. As a result there has been an ongoing decline in new mortgages being written on high loan to valuation ratios (LVRs). Over the quarter, $6.676 billion in mortgages were for LVRs above 90%. Based on this figure, the value of mortgages on LVRs above 90% was -2.3% lower over the quarter, -13.3% lower over the year and it was the lowest quarterly value of mortgages greater than 90% LVR since March 2011. Over the quarter, the value of mortgages with an LVR of between 80% and 90% was $13.547 billion which was -4.1% lower over the quarter but 3.6% higher year-on-year. Over the September 2017 quarter, an historic low 20.6% of new mortgages had an LVR greater than 80%.

Clearly, APRA’s macro-prudential controls on lending have worked. Shame APRA didn’t implement them early in the housing cycle, rather than well after the horse had bolted.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.