This is the second interim report of the Australian Competition and Consumer Commission’s (ACCC) inquiry (‘the Inquiry’) into gas supply arrangements in Australia. The ACCC is

focussing on the operation of the East Coast Gas Market, where there are continuing immediate and longer-term concerns.

In the September 2017 report, the ACCC reported on the supply-demand outlook for 2018.

The ACCC found that there was likely to be a substantial gas supply shortfall in 2018 and that commercial and industrial (C&I) users were experiencing difficulties in obtaining gas supply for 2018. In the first part of 2017 in particular, C&I users had few suppliers offering them gas for supply in 2018. Where gas was offered, it was generally at prices well above the ACCC’s estimates of benchmark prices. The ACCC also reported that there was insufficient participation during this period by the Queensland liquefied natural gas (LNG) producers in offering gas to the domestic market for supply in 2018, given that they were collectively forecasting significant LNG export spot sales for 2018.

On 3 October 2017, the Australian Government reached a Heads of Agreement with the LNG producers. In the Heads of Agreement, the Government acknowledged that the east coast LNG industry is a net supplier to the domestic market. However, to ensure the security of supply of gas to Australian users, the Government obtained an agreement from the LNG producers that they would offer sufficient gas to the domestic market to meet the expected supply shortfall in 2018 and 2019 and that those offers would be made on reasonable terms.

Information obtained by the ACCC since the September 2017 report shows that LNG producers have made significant additional quantities available to the domestic market over the past few months and there have been some improvements in the availability of gas and prices offered to gas users in the East Coast Gas Market. However, the East Coast Gas

Market is still not functioning effectively and domestic prices are still in excess of the ACCC’s estimates of benchmark prices.

Over the past few months, the Queensland LNG producers have diverted significant quantities of gas into the domestic market. The LNG producers have contracted 42 petajoules (PJ) of gas under long-term gas supply agreements (GSAs) to domestic buyers for supply in 2018 since the September 2017 report. This was enabled by the LNG producers reducing their planned exports for 2018. Collectively, the LNG producers reduced their LNG export contract and LNG feed gas requirements for 2018 by 34 PJ and their planned LNG spot sales by 29 PJ. The LNG projects are still forecasting to sell 34 PJ on the international LNG spot markets in 2018.

The bulk of the gas sales by the LNG producers were to aggregators and retailers. While a substantial portion of this gas will be used to supply customers that were already contracted, the rest of the gas was used to enter into new GSAs with C&I users and gas powered generators (GPG). In total, aggregators and retailers have sold 32 PJ of gas for supply in 2018 since the September 2017 report.

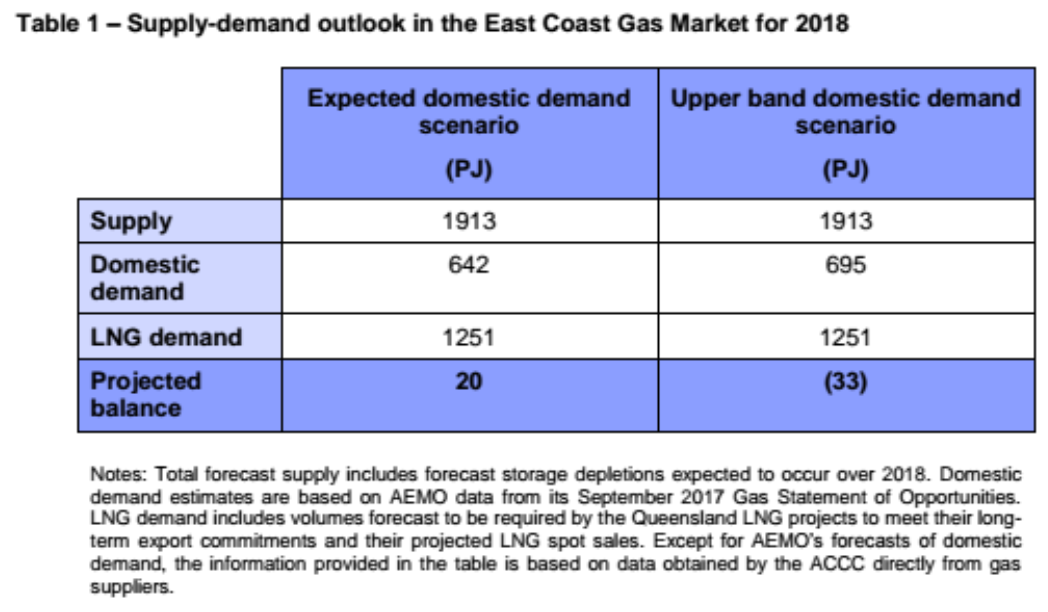

As a result of additional supply being made available and a reduction in planned exports, there is now a lower likelihood of a supply shortfall in the East Coast Gas Market in 2018, as shown in table 1. However, the gas supply-demand balance in the market remains tight.

As reported in the September 2017 report, there will be insufficient production in the Southern States in 2018 to meet forecast domestic demand. This means that gas users in the Southern States are relying on gas produced in Queensland to be transported into the Southern States to meet their needs. The gas shortfall in the Southern States can add at least $2/GJ and possibly up to $4/GJ to the prices paid by gas users in those states. In addition, access to pipeline capacity, particularly on the key north to south transport routes, is increasingly important to market participants.

At present, most of the key pipelines necessary to deliver gas from Queensland to the Southern States are close to fully contracted in 2018. The two largest retailers have contracted a significant proportion of the firm transportation capacity on these key pipelines.

This means that, in the short term, other parties seeking to transport gas from Queensland into the Southern States who do not hold firm capacity on these pipelines could alternatively:

negotiate with an existing capacity holder for secondary capacity

acquire capacity from pipeline operators through as-available or interruptible services, or

enter into gas swap arrangements.

The ACCC examined whether retailers who control the pipeline capacity on key pipelines to move gas south were making unused capacity available to other market participants. The

ACCC generally did not find evidence to suggest retailers are purposely withholding capacity. The retailers that hold the firm capacity rights on the key north to south pipelines are generally using their capacity, although in non-peak periods throughout the year there is spare capacity which could be made available through secondary capacity trading.

However, the ACCC did receive some claims alleging that on some other pipelines, retailers’ unwillingness to trade secondary pipeline capacity restricted competition for the supply of gas to C&I users connected to those pipelines. Following the ACCC’s investigation into the conduct of those retailers, we have observed that those retailers are now making spare capacity available on those pipelines for use by other market participants. This has resulted in more competitive outcomes by giving gas users a greater choice for sourcing gas supply.

The ACCC will continue to monitor the utilisation of pipeline capacity and whether retailers are making spare pipeline capacity available to the market on reasonable terms.

In the absence of firm capacity, there is demand for as-available or interruptible services on the key north to south pipelines. However, these services are lower in priority than firm services and the prices of interruptible services on some of the key north to south transport routes are set at a relatively high multiple of the firm transportation rate.

Some market participants have entered into gas swap arrangements to overcome pipeline congestion on the key north to south transport routes and are paying fees that are lower than transportation costs. While there are benefits in engaging in gas swaps, there are limits on how much gas can be swapped between locations.

Critically, pricing for pipeline services has remained high, with little change from the monopoly pricing identified in the ACCC’s 2015 inquiry. However, the ACCC expects that prices should come down as a range of regulatory reforms in respect of access to firm and secondary pipeline capacity begin to take effect.

On the whole, limited access to reliable and reasonably priced transportation capacity on key pipelines appears to be constraining the ability of some market participants to bring gas from Queensland into the Southern States, which is limiting the level of competition for gas supply in the Southern States.

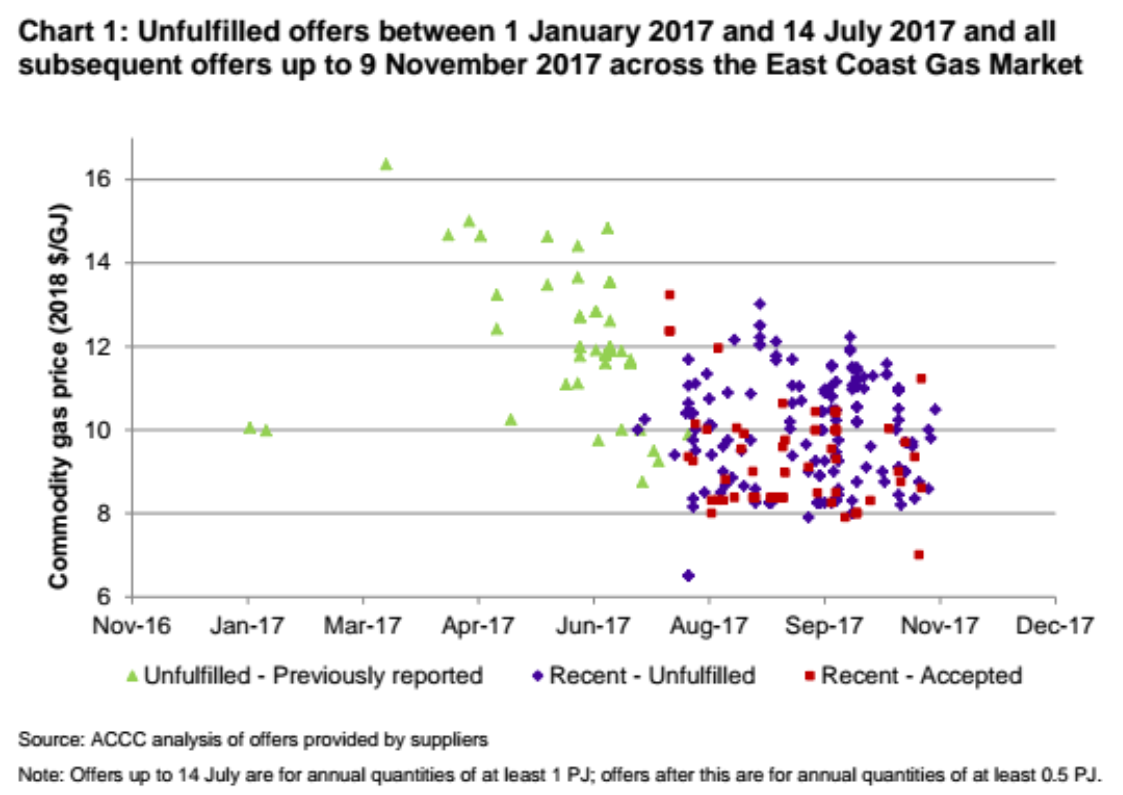

Prices offered to C&I users have fallen substantially since early 2017, but contracted prices remain higher than the ACCC’s benchmark estimates Gas prices offered to large C&I users that consume more than one petajoule of gas per annum reached a peak of $16/GJ in early 2017, while some prices offered to smaller C&I users by retailers were even higher. Given these high prices, many C&I users chose to delay contracting for 2018 supply at the time. Since July 2017, commodity gas prices offered to large C&I users have eased and have generally been made at $8–12/GJ, as shown in chart 1.

As offered prices declined, C&I users have become more willing to enter into GSAs, with around 12 large C&I users recently contracting with retailers or aggregators for 2018 supply.

While 2018 prices under recently agreed GSAs are considerably lower than prices that were being offered in early 2017, prices that are expected to be paid in 2018 under the recently struck GSAs are similar to, or higher than, those prices that were agreed for 2018 supply under GSAs entered into in 2016.5 Further, the recently agreed 2018 prices remain largely at the upper end of, or above, the prices that would be likely to prevail in a well-functioning and competitive market.

In Queensland, wholesale gas prices set by LNG producers for 2018 supply between June and November 2017 have averaged $8.38/GJ. This is higher than the forecast average spot LNG netback price at Wallumbilla for 2018, which ranged between $5.87/GJ and $7.85/GJ over this period.

In the Southern States, wholesale gas prices set by producers between June and November 2017 have averaged $9.74/GJ. This is at the upper end of, or higher than, the ACCC’s estimates of benchmark prices in the Southern States, which range between $6.55/GJ and $9.93/GJ. The benchmark estimates vary depending on a gas user’s location, with the upper limit of the range relevant for users in Victoria and the lower limit for users in South Australia.

Following the publication of the September 2017 report, the ACCC sought updates from C&I users that were uncontracted during the previous round of consultation and contacted some smaller C&I users about their experiences in the market. On the whole, C&I users informed the ACCC that market conditions have improved since the September 2017 report. Some C&I users thought that the government’s focus on the gas industry and the ACCC’s market monitoring were likely contributors to these improvements. However, user experiences varied depending on size.

Over the past few months, large C&I users consuming over one petajoule of gas per annum have received substantially lower price offers than in early 2017 and have had more engagement from suppliers. Nearly all of the 10 large C&I users we recently spoke to have entered into GSAs for supply in 2018, with the one remaining uncontracted user in negotiations. These users generally had 2-3 competing suppliers making offers to them and two users had offers from six different suppliers.

The experience of C&I users that consume smaller quantities of gas has been somewhat different. These C&I users are typically not large enough to enter into negotiations directly with producers and have to rely on retailers for gas supply. They informed the ACCC that prices offered to them by retailers have come down from around $18-19/GJ in the first half of 2017 to about $11/GJ or less. However, in some cases they are still only receiving offers from one or two retailers, with some users reporting that retailers continue to claim to have no gas available.

Recent behaviour of some retailers towards C&I users who were seeking to re-contract is not what would be expected in a well-functioning market. In some instances, unwillingness by a retailer to offer gas to long-term customers whose contracts were expiring put these C&I users into a difficult position in respect of their ongoing operations into 2018, potentially creating significant effects in local economies and beyond.

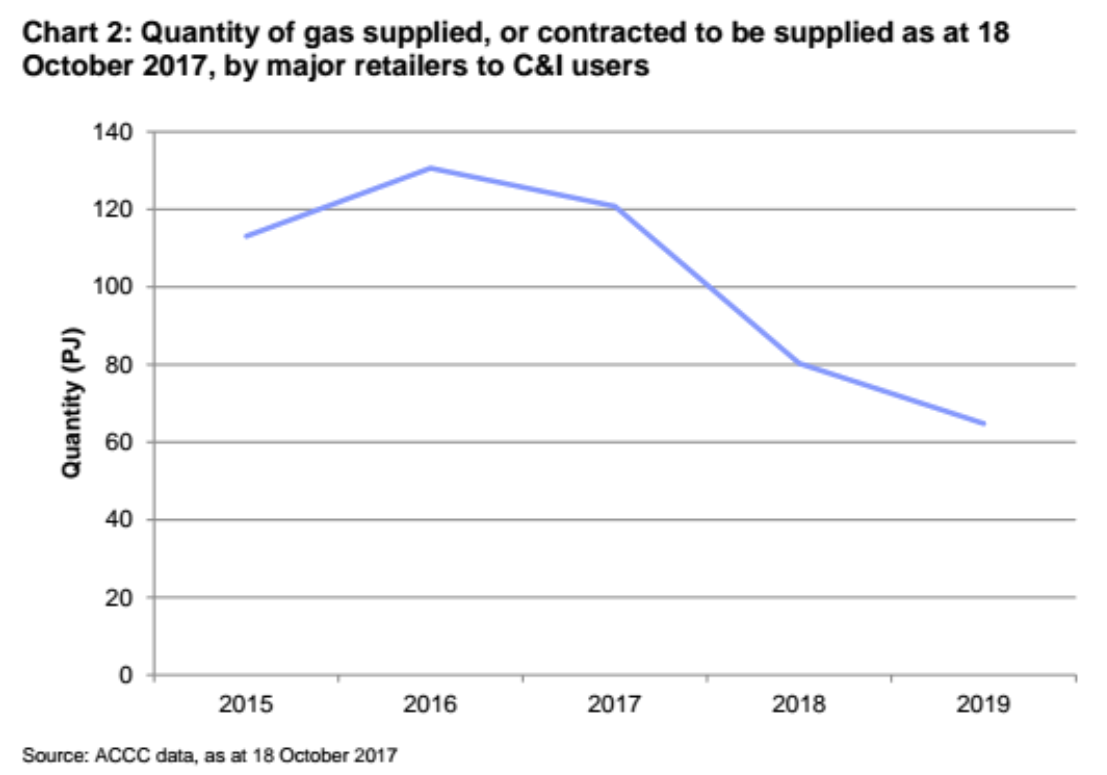

Information received by the ACCC from the three major retailers shows a significant reduction in the quantity of gas that some of them have contracted for 2018 and 2019 compared to the previous years, as shown in chart 2.

It appears that due to limited gas supply and higher gas prices, some retailers consider that they now face higher risks in supplying C&I users than they had in the past. In particular, some retailers are concerned that, given the current high gas prices, if they purchase large quantities of gas before signing up customers, they may not be able to sell the entire quantity of gas under long-term GSAs and would have to sell it at lower prices on the domestic spot markets instead. Some retailers are also concerned that, at current gas prices, C&I users are at higher risk of market exit, which could again put the retailer into the position of having to sell undelivered quantities of gas into the domestic spot markets.

While price offers received by both large and smaller C&I users are now lower than they were earlier in the year, many C&I users consider that current prices are unsustainable for their businesses over the long term. This has led to some choosing to hold off entering into GSAs for 2019 in the hope prices will improve further. This is an issue of great concern. A number of small C&I users have also joined together to form a larger buying group. This enables these users to negotiate directly with gas producers and aggregators, opening up greater opportunities for gas supply and resulting in improved offers.

Over the period May–July 2017, the Gippsland Basin Joint Venture used a blind tender process to sell gas in Victoria. All of the successful bidders were retailers and/or gas powered generators (GPGs). The results of this tender appear to indicate that if the East Coast Gas Market is short on gas and different types of buyers are required to compete for gas supply, C&I users may be crowded out by other gas users, particularly GPGs. In circumstances where GPGs are increasingly setting prices in electricity markets, they are more likely to be able to pass on higher gas prices to their customers than C&I gas users, a number of which produce trade exposed products.

Some improvement but don’t be fooled. This disaster has only just begun. With everyone on short term contracts now, as the AUD falls, the export net-back price that the ACCC is using for its fair price benchmark will go through the roof.

They never learn these economic eggheads, only ever edging away from their perfect market hypotheses. We need a draconian solution to the complete collapse of the market. Fixed domestic quotas and prices in Australian dollars. Regulate price for the pipeliners.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.