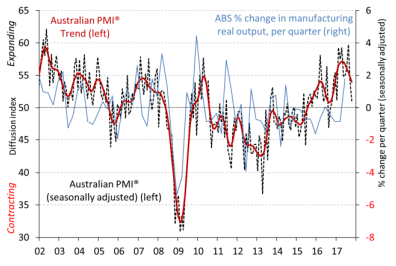

▪ The Australian Industry Group Australian Performance of Manufacturing Index (Australian PMI® ) fell 3.1 points to 51.1 points in October (seasonally adjusted), indicating slower growth after a run of stronger monthly expansions over the previous six months. Results above 50 points indicate expansion with higher results indicating a stronger expansion.

▪ September marked a thirteenth month of expanding or stable conditions for the Australian PMI® and the longest run of expansion since 2007. Growth has slowed since mid-2017 however, with October indicating the slowest monthly growth since January 2017.

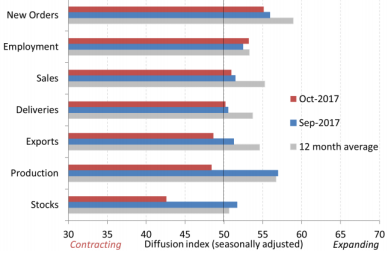

▪ Of the seven activity sub-indexes in the Australian PMI® , three expanded, three contracted and one was stable in October (seasonally adjusted). New orders and sales expanded (results over 50 points), but at slower rates than in September. Employment expanded more strongly, while supplier deliveries were stable for a second month. Exports, production and stocks (inventories) all contracted in October (results under 50 points).

▪ Six of the eight sub-sectors in the Australian PMI® expanded in October (trend) and two contracted. The non-metallic minerals sub-sector remained at a record high (72.2 points) due to strong demand for building-related products. The food and beverages sub-sector also performed well in October, while other sub-sectors expanded at slower rates.

▪ October marked the end of automotive assembly in Australia, with the closure of the last car assembly lines at GMH in Adelaide and Toyota in Melbourne. This was reflected in lower results (and an absolute contraction) in the Australian PMI® in South Australia.

▪ Outside the automotive sub-sector, conditions appeared to be relatively buoyant, if a touch slower, in October. Positive sources of local demand for manufacturers included apartment and infrastructure construction; defence, mining and agricultural equipment; renewables and utilities. Higher input costs for electricity, gas, milk and butter are biting into margins.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.