After last week’s Productivity Commission (PC) report included a recommendation for the states to shift from stamp duty to land taxes, and the property lobby endorsed the idea, attention has turned to how the reform could be implemented in practice.

Kevin Davis, research director of the Australian Centre of Financial Studies, believes he has the answer: something called ‘Bowie bonds’. From Peter Martin:

[The most obvious approach] would be to eliminate stamp duty immediately and to apply the land tax only to those properties that were bought stamp duty free. Eventually, after most properties changed hands, the land tax would be near universal.

But the main reason none of the states have done it is the short-term hit to revenue. Stamp duty is collected infrequently. Land tax would be collected more frequently at a much lower rate, every year or every quarter. But if the rate was set to make no-one worse off, the government would to wait years after properties had been sold to get back in land tax what would have earned immediately in stamp duty…

[Ken Davis’ proposal] is for state governments to sell their right to some of their future land tax collections in return for upfront payments.

“In each year following the abolition of stamp duty, the government will no longer receive the large revenue amount which would arise from stamp duty on house sales in that year,” his paper says.

“Suppose that were $5 billion (a conservative estimate for the larger states). It would be fairly straightforward for the government to issue $5 billion worth of securities which provide the holders with the entitlement to the corresponding future stream of property tax revenue for the next 30 years.”

Professor Davis says a byproduct would be the creation of a new low-risk, long-term asset class suitable for superannuation funds of the kind they get now by buying shares in privately run toll-roads and airports. For funds that wanted it, the payments could be designed to give them exposure to the residential property market…

He says an immediate advantage would be to reward older homeowners who downsized. They would be tens of thousands of dollars better off, instead of no better off as they often are now after paying stamp duty. Australians would find it easier to move for work, and the land tax would impose a penalty on Australians who held onto land rather than using it.

I have previously argued that state governments should give home buyers a credit for the stamp duty already paid, and then deduct the theoretical land tax that would have applied since the home was purchased.

For example, if someone purchased a home in October 2011 and paid $30,000 in stamp duty, and their annual land tax bill would have been $3,000 per year had the new regime been in effect, then their credit would be $12,000, which can be applied against future years’ bills.

But Professor Davis’ plan would work equally well (if not better), especially if it can bridge the funding gap discouraging the states to reform.

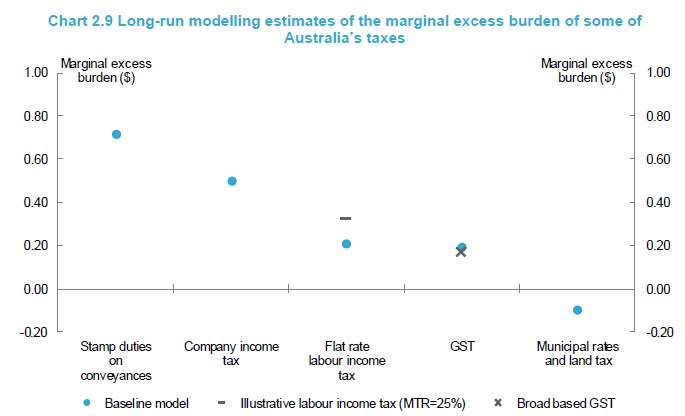

Another option would be for the federal government to bridge the states’ revenue gap. This makes sense for the federal government, given there is a productivity pay-off in switching from stamp duties to land taxes (see below chart) – much of which would flow to federal government coffers via the broader tax system (since it takes in roughly 80% of all tax revenue).

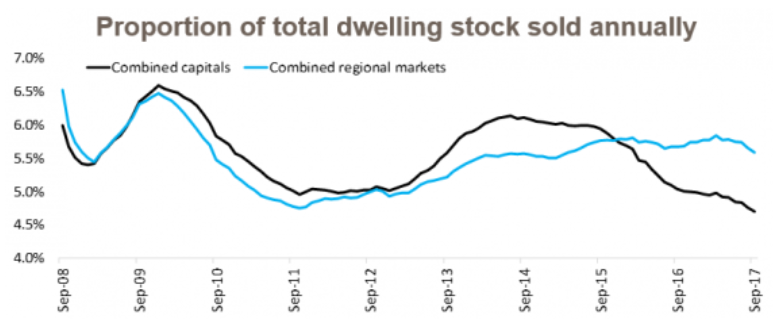

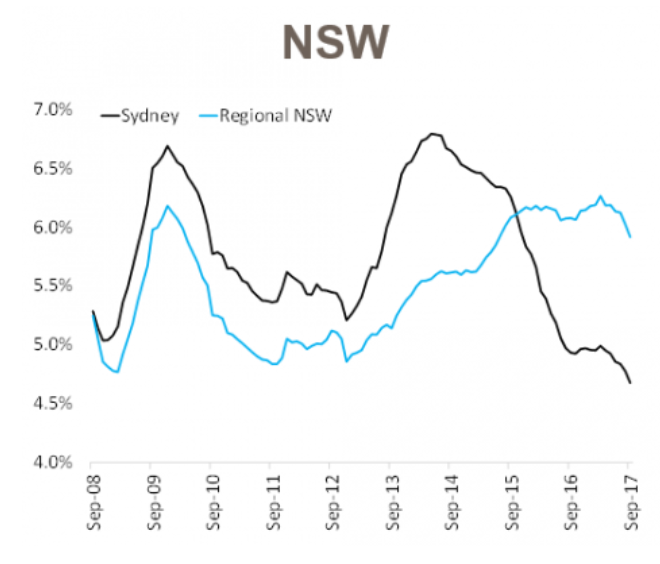

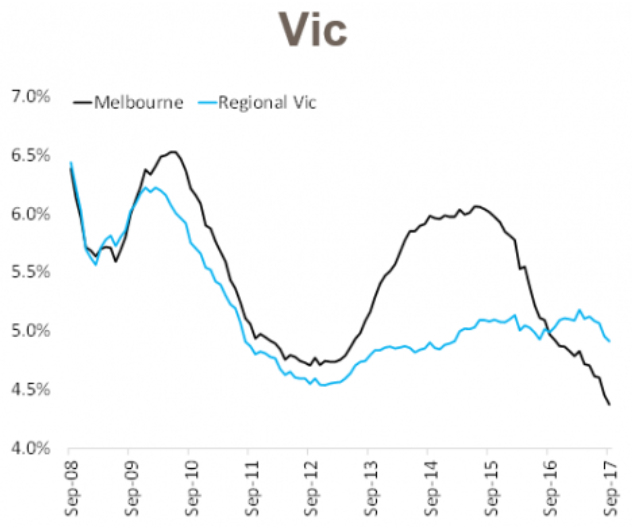

Another factor working in favour of reform is the collapse in transaction volumes, especially in Sydney and Melbourne:

As transaction volumes collapse, stamp duties become a less reliable (and lucrative) revenue source, whereas land tax is far more stable.

In short, the states should reduce their reliance on stamp duties while they can. And the federal government should help facilitate the switch, given they too will be winners.