By Chris Becker

Last night saw a raft of European-centric economic releases, with 3Q German GDP powering ahead while UK inflation remained high, sending Pound Sterling higher. EZ wide GDP, helped by the central power remains well above 2% which sent Euro significantly higher against USD, and European stocks selling off slightly. In the US the falls were heavier due to the falls in oil prices overnight on the back of lower demand growth and the ongoing saga that is the stalled GOP Congress.

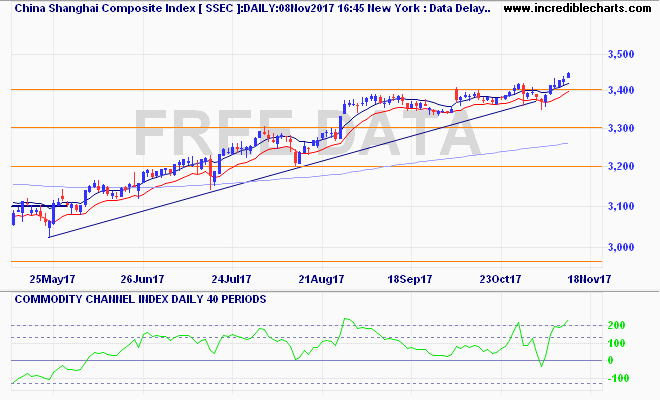

Recapping Asia yesterday first where in mainland China the Shanghai Composite was down over half a percent before lunch, before recovering somewhat to be only off 0.25% towards the close, at 3439 points. The daily chart shows momentum heading into near blowoff mode, so this should continue here to my upside target at 3600 but with a heightened possibility of a dip soon: