by Chris Becker

It was all about tech stocks in Asia today, with profit taking the motive, well except if you own Aussie banks, then its a case of covering risk. Markets are cautious even after a wave of risk taking on Wall Street as OPEC meets later tonight amid a barrage of key economic reports that will provide heady catalysts for bond and currency markets.

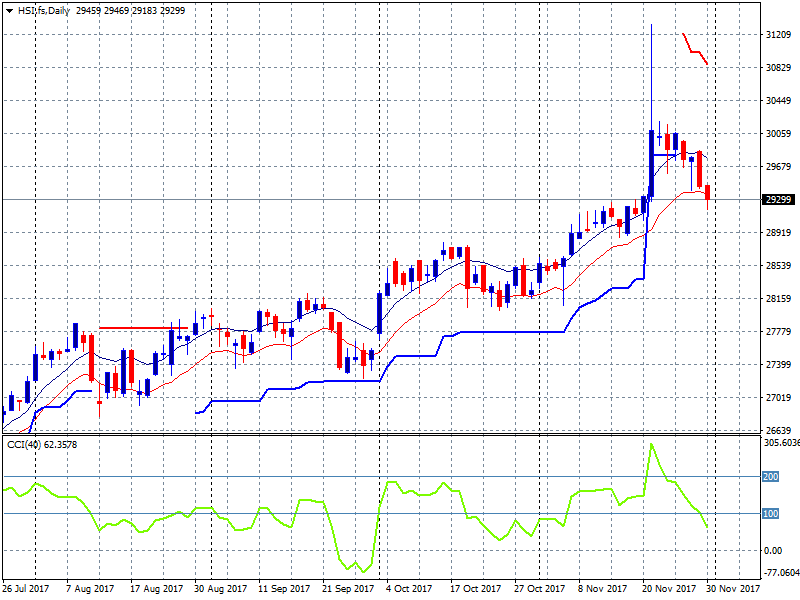

In mainland China the Shanghai Composite is again attracted more to support and selling off, sharply closing 0.8% lower to just above critical support at the 3300 point level. The Hang Seng Index is going even further, losing 1.3% to 29,228 points in a clear breakdown from its daily uptrend. The previous inability to make a new daily high coupled with a fall below the low moving average at 29300 signals a potentially wider rout down to support at the 28500 level:

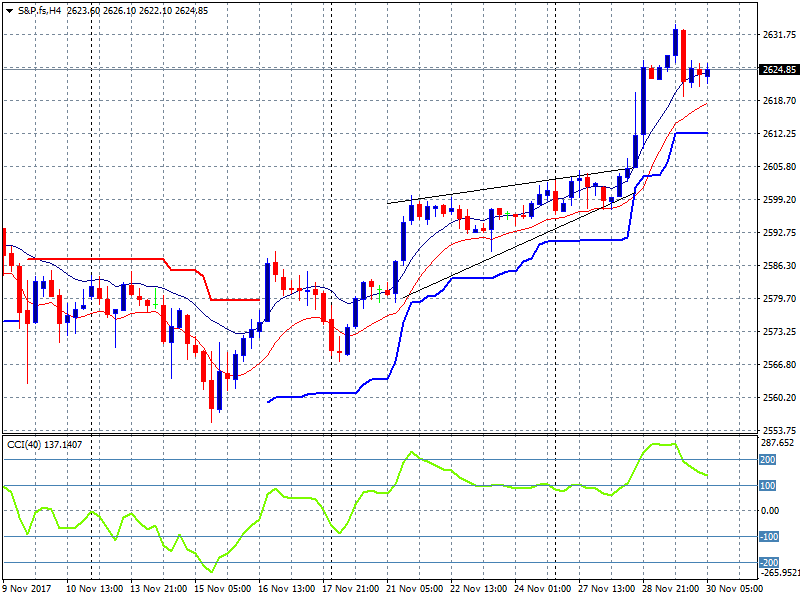

S&P futures are still steady, as all eyes are on the tax cut for the rich prize for Wall Street:

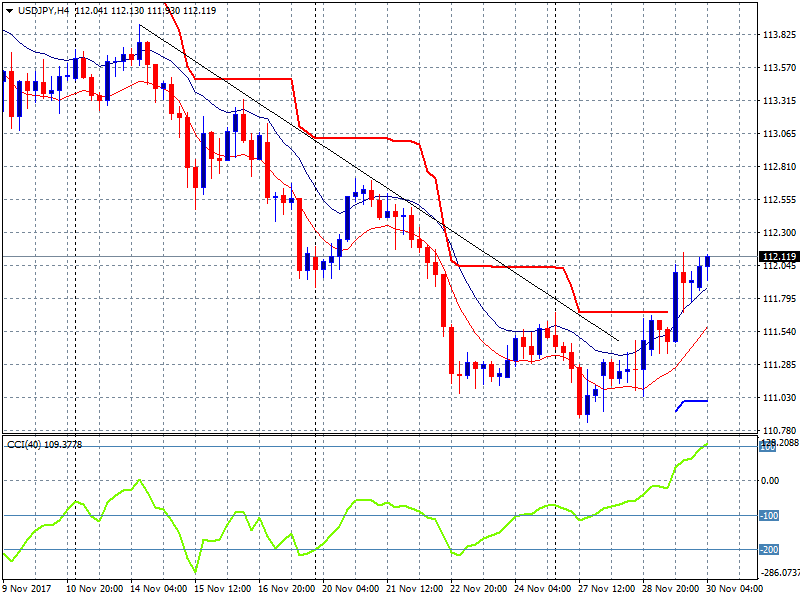

Japanese stocks were positive on the selloff in Yen instead, with the Nikkei closing nearly 0.6% higher to 22724 points, finally making a new daily high as this consolidation phase plays out. The USDJPY pair has broken the the daily downtrend and ATR resistance overhead at the 111.80 area to be above the 112 handle in what looks like a damn fine reversal:

The ASX200 was back above 6000 for a few minutes yesterday, but slammed back to reality today losing 0.7% to 5969 points as the banking sector sold off in the wake of the limp wristed inquiry that Turnbull announced today. CBA lost nearly 2% while retailers actually did surprisingly well after the Oroton news with Myer (MYR) spiking 0ver 6%!

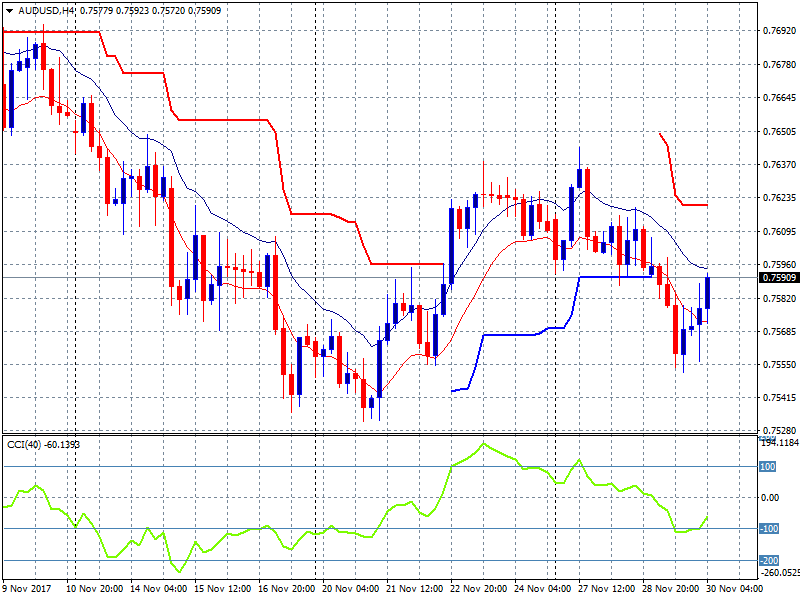

The Australian dollar was pulled down overnight but is slowly recovering here almost making it back up to the 76 handle against USD The overnight releases will continue to weigh on the Pacific Peso so watch the crosses as well, particularly EUR and JPY:

The data calendar tonight includes the only unemployment number that matters in Europe – Germany’s – followed by EZ wide CPI, the opening of the OPEC meeting and to round it all out, the US PCE (personal consumption expenditure) print. A doozy!