by Chris Becker

Risk in Asia can’t get started this week with more falls across stock markets following a lacklustre lead overnight on Wall Street. Commodities lead the way actually with oil dropping the second day in a row as OPEC gets ready for its meeting, with currency markets relatively quiet as the USD remains steady.

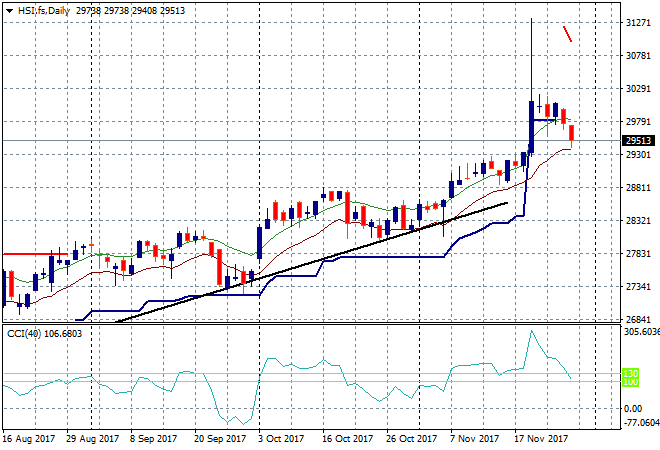

In mainland China the Shanghai Composite continues to stumble, almost going through key support at 3300 before bouncing back after lunch, losing 0.2% to be at 3315 points. The Hang Seng Index is doing worse, down nearly 1% to be at 29,419 points. This inability to make a new daily high coupled with a fall below recent session lows mean I’m watching the low moving average at 29300 for a possible breakdown:

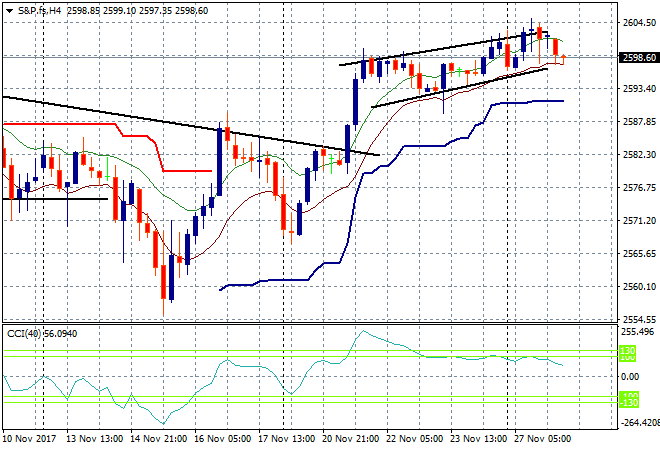

S&P futures are receding to the edge of the flat pattern on the four hourly chart with all eyes on support not far away at 2590 points:

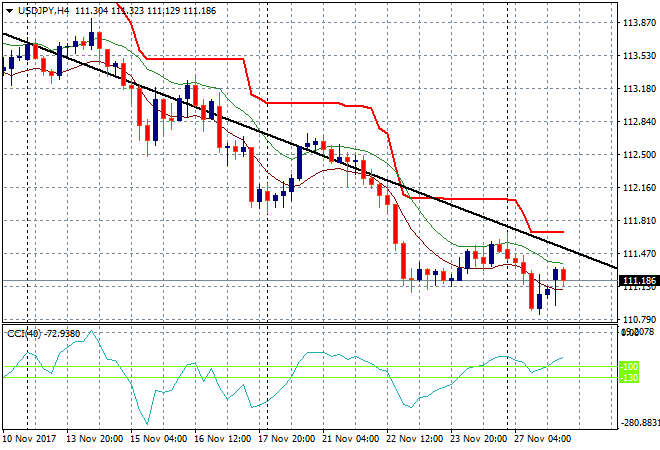

Japanese stocks slipped even as the Yen slightly lost ground against the USD, with the Nikkei down 0.2% to 22463 points, still unable to make headway since its early November blowoff. The USDJPY pair found support at the 110.90 level overnight and has slightly bounced above the 111 handle in the Asian session, but is not yet threatening the daily downtrend:

The ASX200 put in a scratch session, still unable to get above 6000 after being the only Asian bourse to have a positive start to the week. It was very mixed across the top 50 and across the sectors with banks basically treading water while the major commodity players retreated with BHP and Fortescue losing nearly 2%

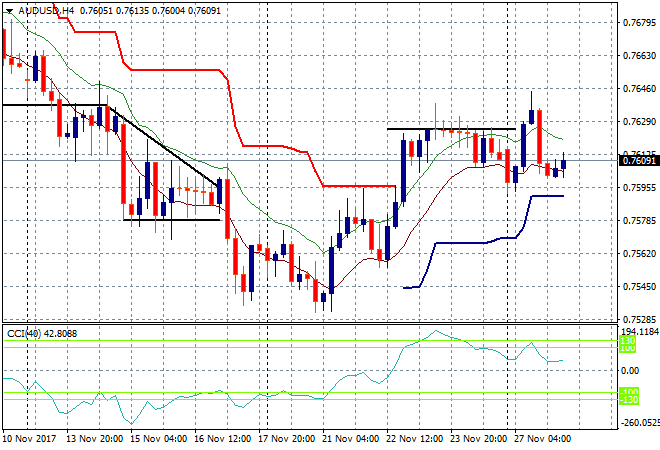

The Australian dollar is being attracted to the 76 handle against USD after a false breakout last night did not turn into a full rout this morning. The overnight releases will weigh on the Pacific Peso as will the commodity markets when London and Chicago open:

The data calendar gets busy tonight with the OECD releasing its economic outlook for Europe, followed by the October advanced trade goods balance in the US, plus house prices and consumer confidence (but I repeat myself) for November.