by Chris Becker

While it was a “yes” here in Australia, Asia is saying no to risk with stock markets continuing to selloff amid a broadening correction. The solid GDP print in Europe overnight was followed by a positive, but no upside surprise in Japan today, but sentiment sent stocks down as the Yen appreciated.

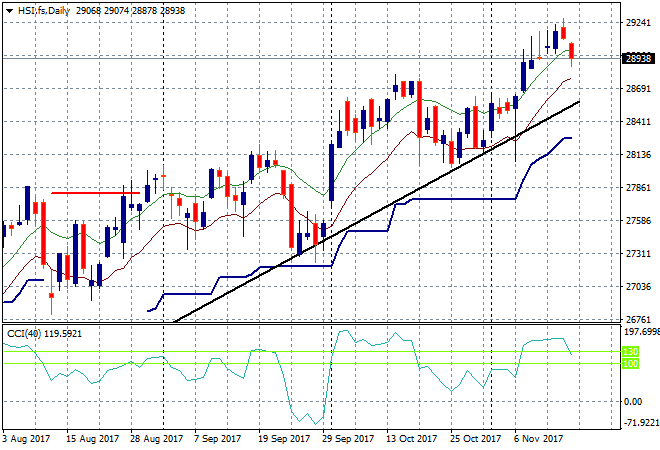

In mainland China the Shanghai Composite is down nearly one percent towards the close, to be just above critical support at the 3400 point level. Similarly, the Hang Seng Index is down below 29,000 points by falling nearly 0.7% as yesterday’s candle signalled an apex here on the daily chart. This should revert to the trendline down to 28600 or so:

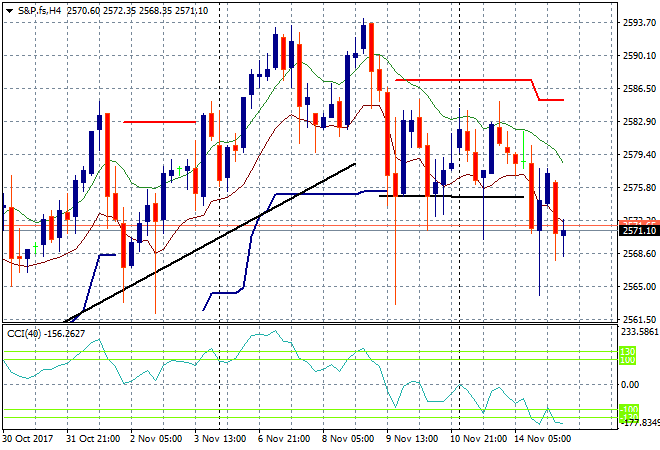

S&P futures continue to retreat on the risk off move, straight down to key support at 2575 points:

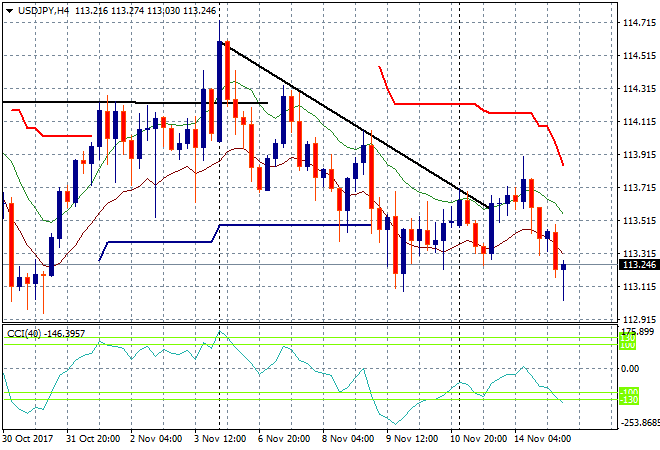

Japanese stocks have fallen the most in the region with the Nikkei down 1.6% to be just above 22000 points as it plummets through daily support as part of a wider correction. The USDJPY pair sold off before the GDP print and went below the 113 handle briefly, holding on here but I expect further falls tonight as the US CPI print comes in:

The ASX200 slumped again today, following the Aussie dollar lower on the wage print, closing 0.6% lower to 5934 points. The losses were again shared equally among banks and miners, but commodity prices are really starting to weigh here on the materials sector, so watch out below.

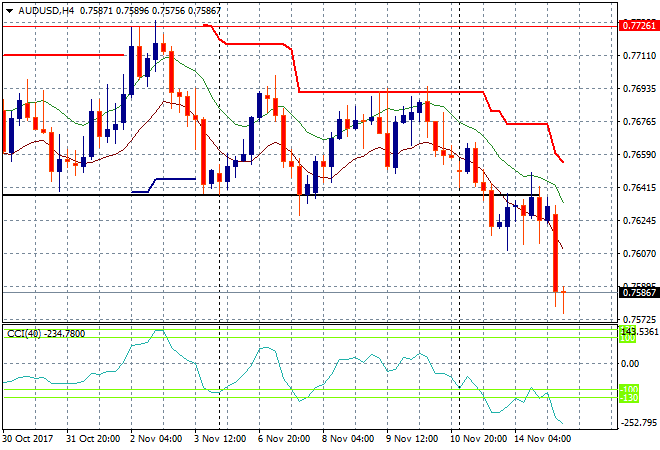

The Australian dollar has had it now, flopping straight through the 76 handle on the back of todays wage “growth” print. This could get ugly (or beautiful depending on your point of view – there’s beauty in chaos and shorting things!) as there’s SFA support down to 73.50, and then 71 very quickly:

The data calendar includes a big one tonight – US CPI – then retail sales and for the oil watchers, the DOE crude oil inventory report.