by Chris Becker

The fallout from the drop in US stocks continued in Asia today, taking the edge of what was a good week for traders. While earnings seasons around the globe indicate strong corporate growth, the legislative chaos that is the US Congress is forestalling any further risk in markets. Next week’s APEC meeting and the continued Saudi Arabian “crackdown” and warmongering in the Middle East will be hotspots as well.

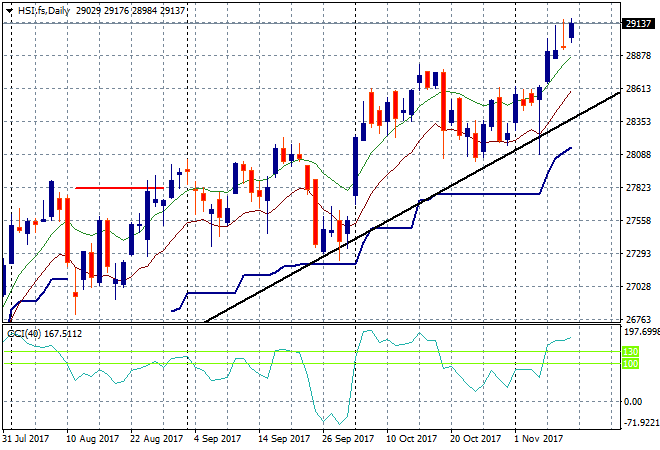

In mainland China the Shanghai Composite is building above its recent breakout above 3400, up 0.2% after the long lunch break to be at 3439 points going into the close. The Hong Kong based Hang Seng Index is up 0.3%, pushing ever higher to be well above 29000 points. It looks like any upside resistance has been brushed aside as this goes into blowoff mode:

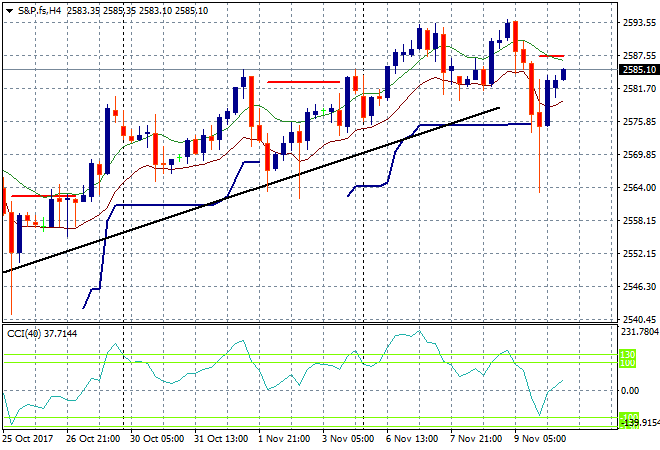

S&P futures are recovering ever so slightly on the mixed Asian lead:

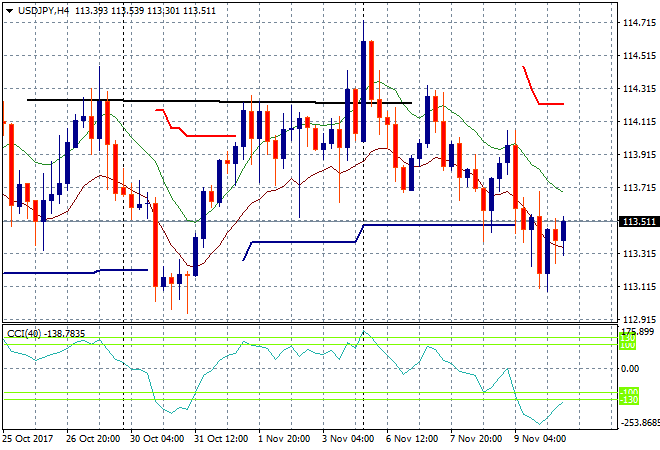

Japanese stocks continue to correct from their stratospheric highs with the Nikkei closing down 0.7% lower in what could be the start of a wider dip or corrective phase from its blowoff rally to close at 22693 points. The USDJPY pair remains below ATR support at the 113.50 level after the falls of last night, marking the previous weekly low in what looks like another move lower:

The ASX200 finishes the week with a whimper, closing down 0.3% to 6029 points in response to the poor lead from overnight markets. BHP fell almost 2%, RIO a little more while the banks were relatively unscathed.

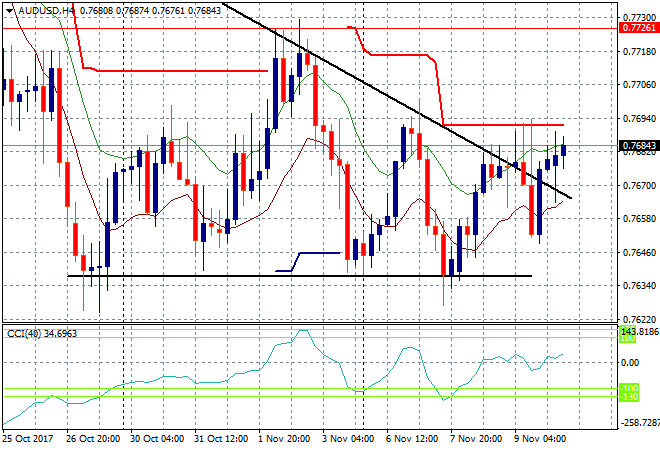

The Australian dollar is fighting back, slowly melting higher on the back of a weaker USD, getting back up to its early week high, but not above trailing ATR resistance. While the downtrend from the daily highs has been broken, significant overhead resistance must be breached before getting excited:

The data calendar finishes the week with some secondary manufacturing and construction numbers in the UK, before the University of Michigan confidence print and the private Hughes oil rig count in the US.