by Chris Becker

Today’s Chinese inflation data figures did nothing to dampen risk appetite here in Asia with most bourses rallying to new highs. Currency markets have been active with the Kiwi up on news the RBNZ may hike rates earlier than planned, while the Yen strengthened late in the session also.

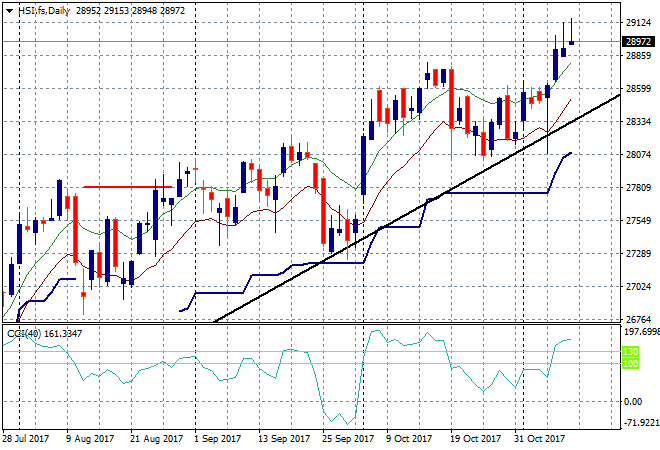

In mainland China the Shanghai Composite is still holding above 3400, sliding a few points to 3412 absorbing the strengthening inflation print. The Hong Kong based Hang Seng Index is up 0.4%, pushing ever higher to be just above 29000 points. Again we’re getting more high wicks on the candle’s here on the daily chart, a sign of selling pressure from high:

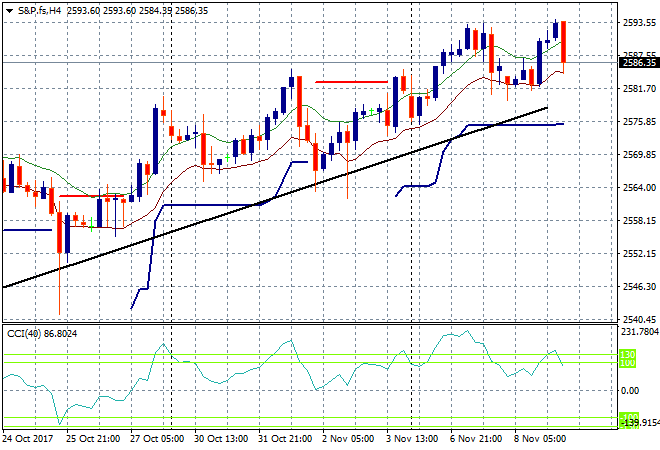

S&P futures are sliding back as this trend mean reverts, unable to break through 2600 points yet:

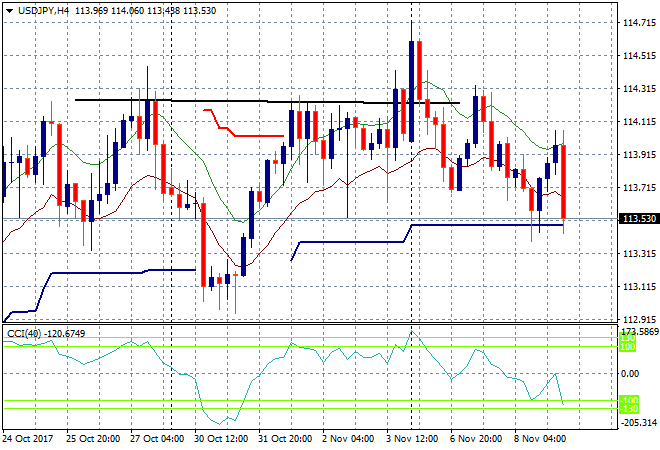

Japanese stocks were doing well but sold off in late afternoon trade as Yen strengthened. The Nikkei closed down 1% lower in what could be the start of a wider dip or corrective phase from its blowoff rally to close at 22677 points. The USDJPY pair has fallen straight to ATR support at the 113.50 level after earlier making gains, indicating there’s an unwillingness to go back above last weeks high:

The ASX200 is making good on its recent breakout above 6000 points, closing 0.5% higher to 6049 points mainly on the back of bank stocks.

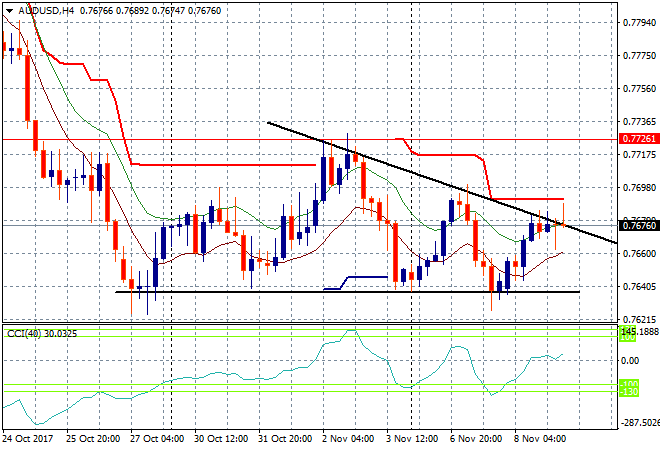

The Australian dollar remains depressed here, unable to make any meaningful change in the last 24 hours almost stuck at 76.70 against the USD. Its wanting to get back to the week and half long bottom at the 76.40 level where if it breaks we could be in for a rout as USD bidders move away from the Pacific Peso:

The data calendar tonight is a little light on, with US initial jobless claims the only major agenda item.