by Chris Becker

Asia starts the week in a mixed fashion, given the strong lead from Wall Street on Friday night, with most stocks dropping or putting in scratch sessions. The Yen fell as Trump waffled in Japan about manufacturing as their continues to be no sign of inflation, as the BOJ continues to hold off on any interest rate rise. Commodities lifted, mainly oil on the back of the Saudi Arabian “coup” in the barbaric kingdom.

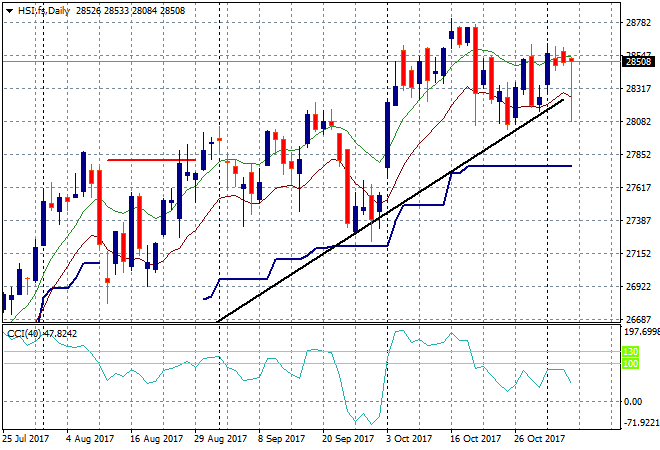

In mainland China the Shanghai Composite lifted after a slow start, rising 0.4% to be at 3388 points, still below previous resistance at 3400 points, but it could be ready to break through this week. The Hong Kong based Hang Seng Index is drifting however, down 0.2% to close at 28536 points. Price remains around the high moving average here on the daily chart which reinforces the bullish mood, but the lack of a new daily high will weigh soon:

S&P futures are steady as traders weigh up the Saudi risk and Trump’s comments on his Asian trip (the adult daycare staff are doing double time!)

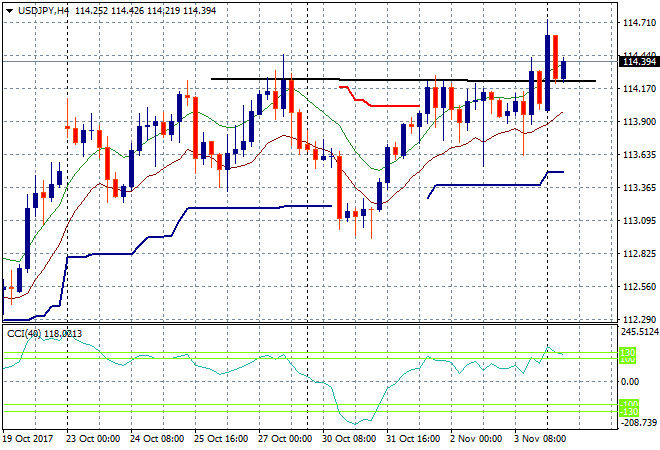

Japanese stocks reopened after their holiday with the Nikkei up only a few points and the broader Topix down the same amount. The USDJPY pair gapped higher on the usual Monday morning nonsense before settling at just above the 114 handle and last week’s resistance level. If it maintains above this level, we could be in for a breakout:

The ASX200 had a poor start to the week finishing with a scratch session, down 6 points to 5953, listless and unable to gain momentum. The banks fell in sympathy with the Westpac result, with that division of Megabank down 2%

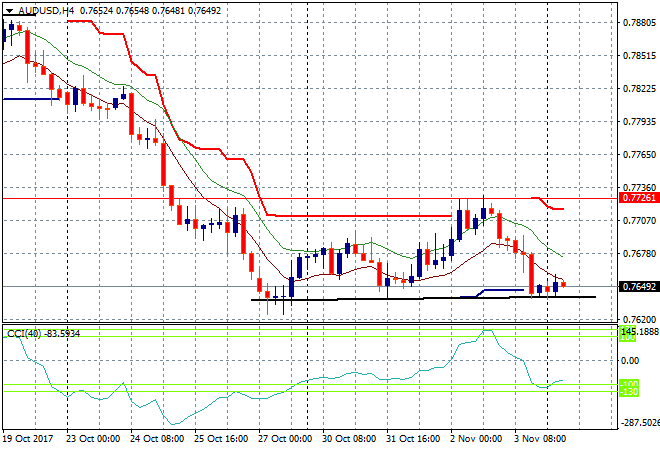

The Australian dollar is trying to push to new lows here, gapping down slightly to setup the overnight trading session at the 76.50 level against USD. Having now stuck below the long held 77.25 level all of last week, if you turn this four hourly chart upside down it looks like a breakout (down) is imminent no?

The data calendar starts the week slowly with some lower tier releases in Europe as all eyes will be on Trump’s Asia visit and the ongoing earnings season.