by Chris Becker

Its risk on across Asia today, with Japanese stocks soaring on the positive mood overnight in US stock markets, plus a weakening Yen. Commodity prices are the catalyst here with industrial metals in particular rallying as bullish forecasts from Glencore provide the impetus, with Bitcoin also going, well – nuts. Its going to be a very busy economic calendar tonight and the risk on mood should carry over until Friday nights NFP.

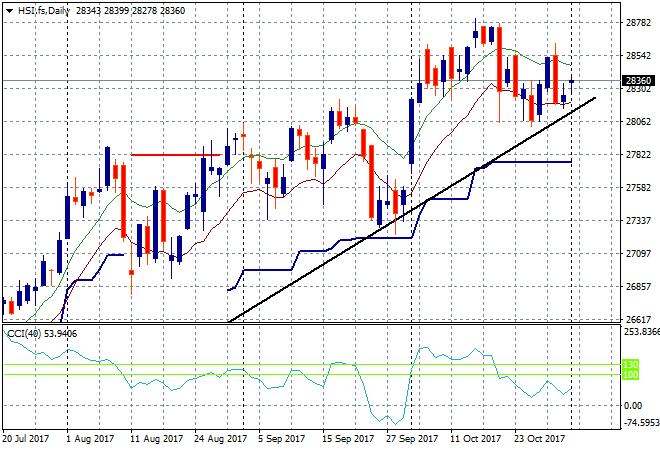

In mainland China the Shanghai Composite is putting in a positive session finally, but is still just below previous resistance at 3400 points, up 0.15% at 3398 points. The Hong Kong based Hang Seng Index is much better off, recovering all of the losses earlier in the week to close up 0.8% higher at 28478 points. Going long on mean reversion and respect of that daily uptrend line is working:

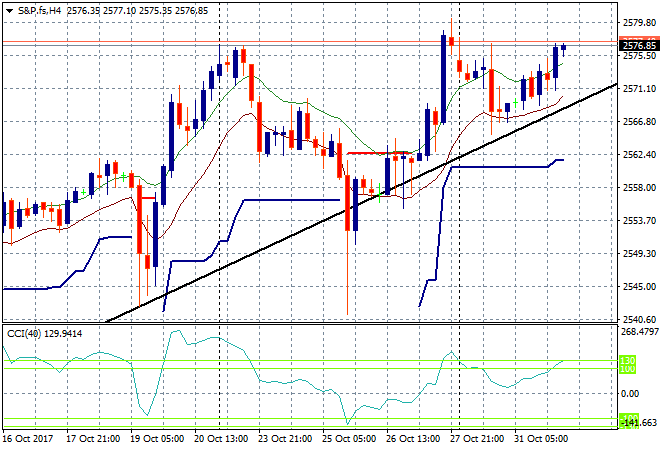

S&P futures are on a roll as risk goes full on with more earnings and key data – including what should be a still dovish Fed meeting (for one more month at least) tonight:

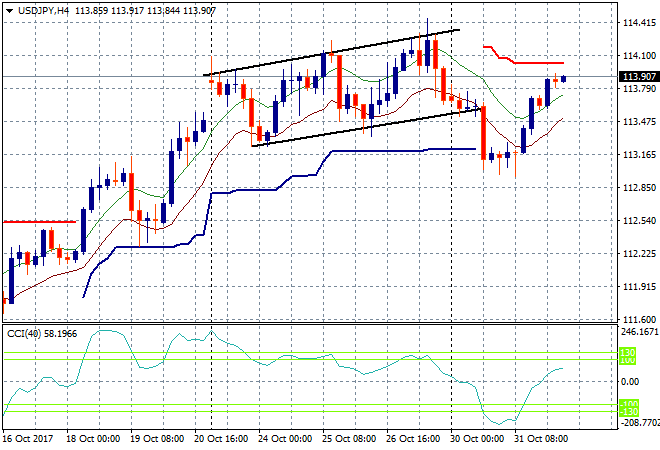

Japanese stocks have led the way in the region with the Nikkei closing up over 1.7% higher to 22429 points as Yen weakened strongly overnight and into the Asian session. The USDJPY pair is just below the 114 handle as long USD holders double down on a good data spread tonight. I’m watching overheard ATR resistance at the 114.10 level to come under pressure and then target last Friday’s high:

The ASX200 finally had a good day, closing up 0.5% absorbing the Caixin PMI to finish 0.5% higher at 5937 points. A few bad results from locals – looking at you Myer – weren’t enough to curb the enthusiasm, with the banks leading the way.

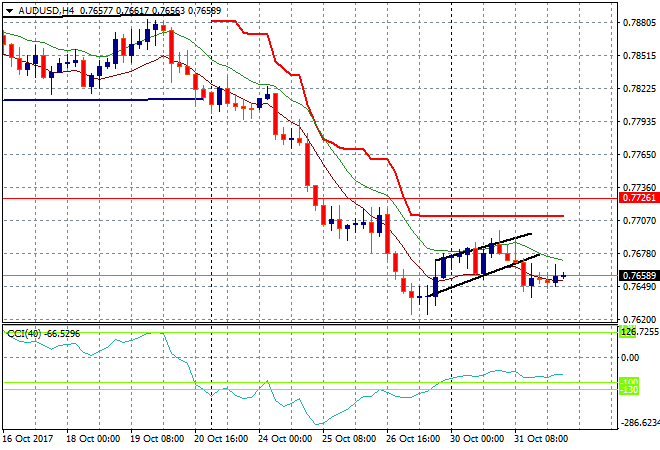

The Aussie dollar is crawling along the bottom here, still stuck at the mid 76s against the USD while it recovers significantly against Yen. For long USD holders though, this is looking good with the potential to retest last Friday’s low if tonights US-centric data is as strong as expected:

The data calendar is US focused tonight with a preview of Friday’s NFP via the ADP private employment report, then the very important ISM Manufacturing print for October. Later on its all about the Federal Reserve with its meeting.