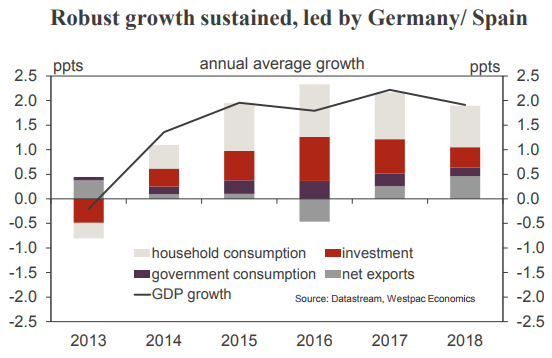

The second estimate for Euro Area GDP confirmed a 0.6% gain for the September quarter. Following March’s 0.6% and June’s 0.7%, that leaves annual growth materially above-trend at 2.5%yr.

However, what got the market’s attention was not this headline result, but rather the acceleration in growth in Germany. There, annual growth rose from 2.3%yr to 2.8%yr, continuing an uptrend in train since the cycle-low of 1.3%yr at end-2015.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.