Australia’s labour market is tightening up. The official survey is showing the strongest y-o-y jobs growth in the post-Global Financial Crisis period and the timely indicators suggest that this momentum is likely to continue. The unemployment rate has fallen to 5.5% from a peak of 6.4% in October 2014. In addition, over the past year, most of the job creation has been full-time positions, which has seen a lift in hours worked and is driving a decline in ‘underemployment’.

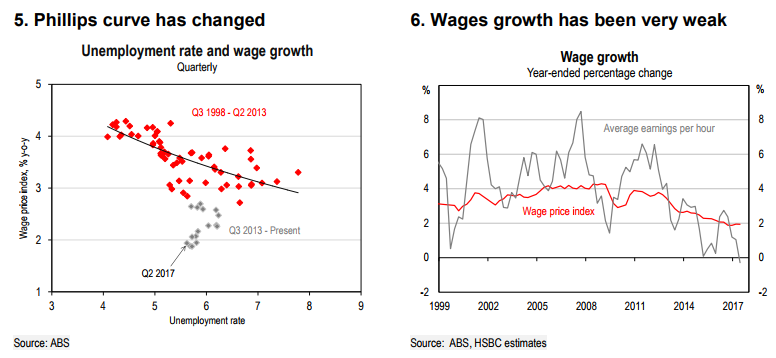

As spare capacity in the labour market is absorbed, it is typically the case that wages growth starts to pick up. However, much like in other countries, the inverse relationship between the unemployment rate and the wages growth (the ‘Phillips curve’) has not been working as it has done in the past. The historical Phillips curve estimates would suggest that the 0.9ppt fall in the unemployment rate over the past two years, should already be lifting wages growth. The relationship has changed.

Globally, the arguments for the ‘flattening’ of the Phillips curve have included: technology’s effect on the nature of work; offshoring as a result of globalisation; increased workforce casualization; and, decreased unionisation, amongst others.

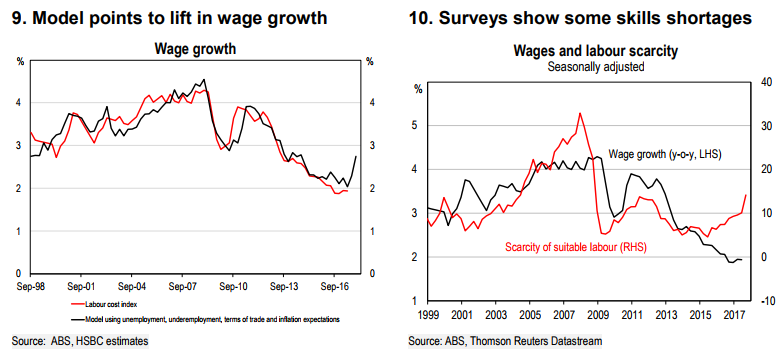

For Australia though, augmenting the traditional Phillips curve using the measure of ‘underemployment’ and incorporating the impact of the resources cycle, seems to help explain recent history quite well. As we have noted before, a key reason for the slowdown in wages growth has been the end of the resources boom and its effect on national income.

Our augmented Phillips curve model suggests that the resources cycle’s effect acts with a lag and predicts that wages growth will pick up in 2018. This is in line with reports in business surveys that it is becoming more difficult to find ‘suitable labour’ and the RBA’s recent reported liaison with its own business contacts, which points to a ‘modest improvement in private sector wages over the year ahead’.

Given that wages lag the cycle, we expect the RBA will start to lift its cash rate once it is convinced that wages growth has passed its trough.

The hidden assumption here is that the labour market will keep tightening but why would it as:

house prices roll over and dwelling construction slumps;

household spending falls;

the car industry shutters;

mass immigration weighs down wages;

the terms of trade resume falls, and

political chaos grows.

We’ll have mass immigration supporting demand and infrastructure spending adding to growth next year but that’s about it as we head into a Labor Government that will make households poorer at a good clip.

Advertisement

Curves schmurves. There’s no trend repair coming to wages and no rate hikes coming, either.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.