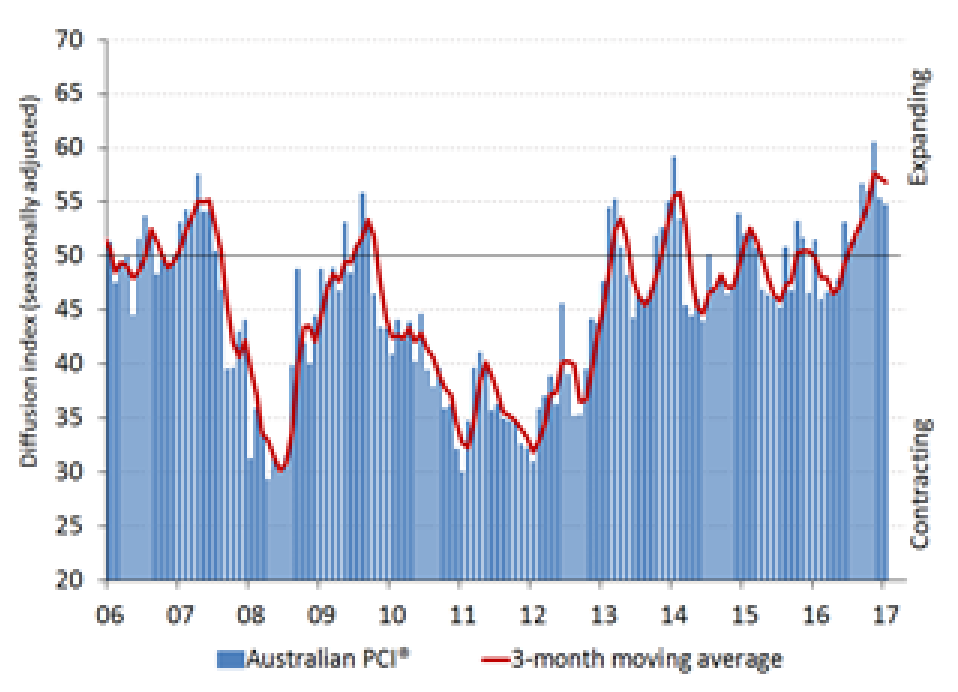

The AIG construction PMI is out and growth slowed again in October to 53.2, still solidly expansionary but well off the boom highs above 60 points:

▪ The national construction industry expanded for a ninth consecutive month in October with a slight easing in growth momentum from September.

▪ The Australian Industry Group/Housing Industry Association Australian Performance of Construction Index (Australian PCI®) fell by 1.5 points to 53.2 points in October, signalling a slower rate of industry growth (readings above 50.0 points indicate expansion with higher numbers indicating a faster pace of expansion).

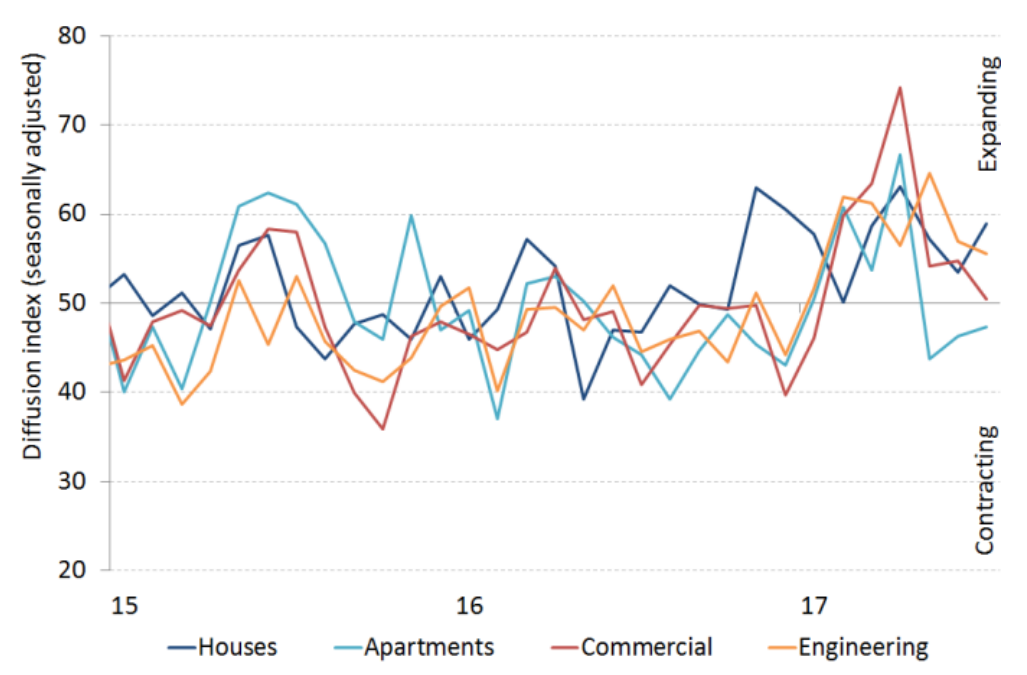

▪ Across the four construction sub-sectors, engineering construction was again the strongest performing area of construction activity with its rate of expansion at a 10-year high on the back of rising levels of non-mining infrastructure work. House building activity also recorded continued growth (albeit at a slower pace) in response to a solid backlog of work and on-going firm demand.

▪ Commercial construction activity was again stable in October while apartment building remained in negative territory although the sector’s rate of decline moderated in comparison with the sharp contraction of the previous month.

▪ Australian PCI® data for October showed that both activity and new orders continued to rise, at rates that were broadly unchanged from September. This was associated with continued expansions in deliveries from suppliers and employment.

▪ Respondents to the Australian PCI® again linked the rise in engineering construction to the upturn in transport infrastructure activity as the roll-out of major new road and rail projects gathers pace.

▪ House builders were generally positive in their assessment of business conditions, pointing to resilient new orders and a relatively solid level of new home builds in October. However, apartment builders cited the constraining influences on activity from soft new orders, a reduction in investor activity and the completion of some major projects.

This swill be a key index to watch. Although it is terrible as a guide to overall national construction, it is a good guide to the east coast. It should measure how the coming collapse in apartment construction is offset or not by houses and infrastructure. Check out how all of the components worked together over much of 2017, delivering the jobs boomlet. No such luck next year.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.