October survey data signalled a further marginal improvement in manufacturing operating conditions across China. While new orders rose at a slightly quicker pace, production increased at the softest rate for four months. At the same time, companies continued to shed staff amid reports of company-downsizing policies and efforts to raise efficiency. This in turn contributed to a further increase in outstanding business, which rose solidly. Strict environmental policies meanwhile contributed to a sharp rise in input costs and weighed on vendor performance. As a result, companies raised their factory gate prices at a solid pace.

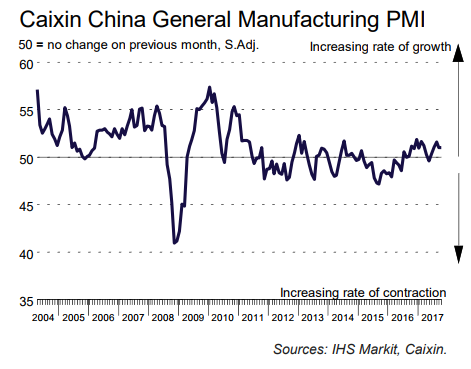

The seasonally adjusted Purchasing Managers’ Index™ (PMI™) – a composite indicator designed to provide a single-figure snapshot of operating conditions in the manufacturing economy – was unchanged from September’s reading of 51.0 in October to signal a further marginal improvement in the health of the sector. Operating conditions have now strengthened in each of the past five months.

Manufacturing companies in China reported a further increase in new business during October. The rate of expansion picked up slightly since September, but remained moderate overall. New export sales rose at a similarly modest pace, following a marginal upturn in September.

In contrast, production increased only slightly in October. Moreover, the rate of growth was the weakest seen for four months. At the same time, confidence towards the 12-month outlook for production moderated to its second-lowest level since August 2016.

Chinese manufacturing employment fell again in October, thereby extending the current sequence of job shedding to four years. Some panellists mentioned lowering workforce numbers in order to boost efficiency. That said, the rate of reduction remained moderate. Reduced staffing levels and higher than expected new orders led to a further increase in backlogs of work.

Notably, the rate of accumulation was the joint-steepest since March 2011 (on par with July 2016). Firms continued to raise their purchasing activity at the start of the fourth quarter, albeit at a marginal pace. However, stocks of inputs declined for the second month running as a number of firms commented on the increased use of current inventories to meet production requirements.

Stocks of finished goods held by Chinese manufacturers also declined slightly in October. Stringent environmental inspection policies and low stock levels among suppliers contributed to a further deterioration in delivery times. These factors also contributed to a further sharp increase in average purchasing costs.

The rate of input price inflation edged down only slightly since September and was among the highest seen since early-2011. In order to protect their margins, firms raised their selling prices again in October. That said, the rate of increase was not as steep as the previous month.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.