Bloxo wants you go short Aussie bonds:

Although the Q3 CPI print showed that underlying inflation was a little lower than expected and that inflation remains below the RBA’s 2-3% target band, it still confirmed that inflation is past its trough. The average of the RBA’s preferred measures of underlying inflation – the trimmed mean and weighted median – was 1.85% y-o-y in Q3. This was below market expectations of 2.0%, but well above the low point for these measures of 1.45% y-o-y in Q2 and Q3 2016.

At the same time, the collection of jobs market indicators for Australia has been universally strong, suggesting that the labour market is tightening up. Employment growth is running at its fastest pace since 2008, at 3.1% y-o-y, and the timely indicators of conditions, such as job advertisement and job vacancies, suggest that strong jobs growth is set to continue in the coming months. The pick-up in job creation has been driven by full-time positions, which suggests declining ‘underemployment’. Jobs growth has also been strong in the mining states, such that Australia’s growth is now becoming more broad-based. In addition, there are signs in the business surveys that firms are starting to find it more difficult to get ‘suitable labour’, which is a typical precondition for a pick-up in wages growth.

We continue to expect GDP growth to pick up in the coming quarters, as the mining drag fades. The lift in growth, combined with a tighter labour market, is expected to support a gradual pick-up in wages growth and inflation. This should see the RBA start to lift its cash rate next year, as it heads back towards a more normal policy setting.

We have held the view that the RBA would start to lift its cash rate in 2018 since December 2016 (see The RBA Observer: Game Changer: Commodities and Trump, 2 December 2016). We tweaked our view, by pushing back the timing for the next hike from Q1 to Q2 2018, following the recent CPI print, which was a bit weaker than expected (RBA Observer Update: It might take just a little longer, 25 October 2017).

On fixed income strategy, we continue to favour the long-end. There is potential for a modest re-pricing of the front-end but this RBA meeting is unlikely to be the catalyst.

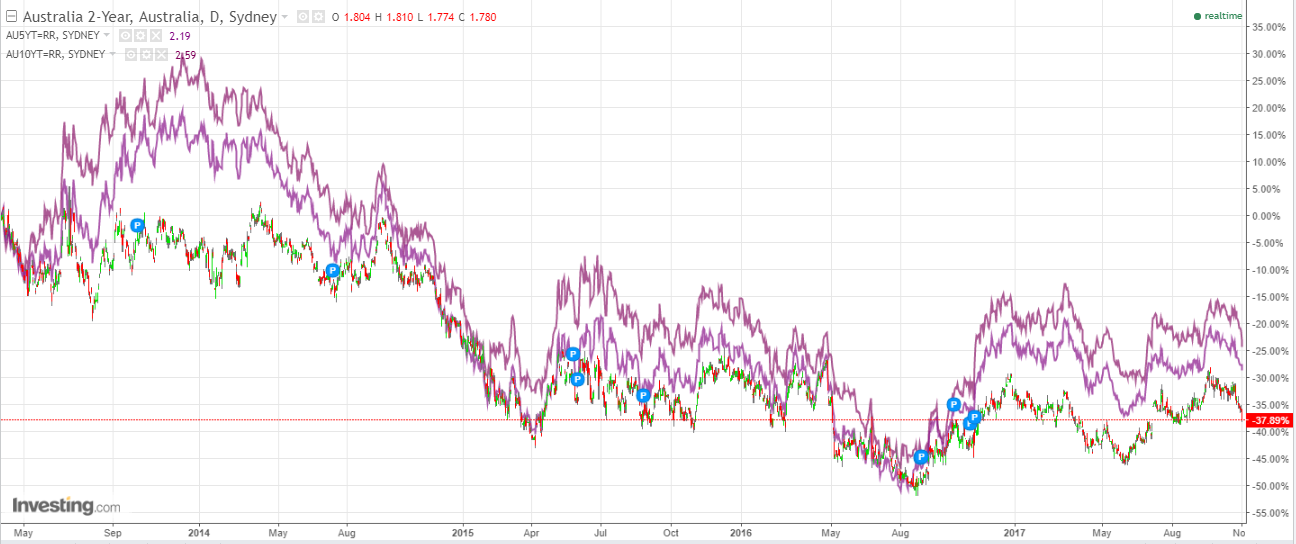

But the Bloxobuster trade is rampaging the other way as households die, with the second illusory rate hike all but gone as the 2 year hit 1.76%:

The good news is that stocks loved it, breaking to new 2017 highs:

There’s nothing like falling growth and profits to get the bid moving!

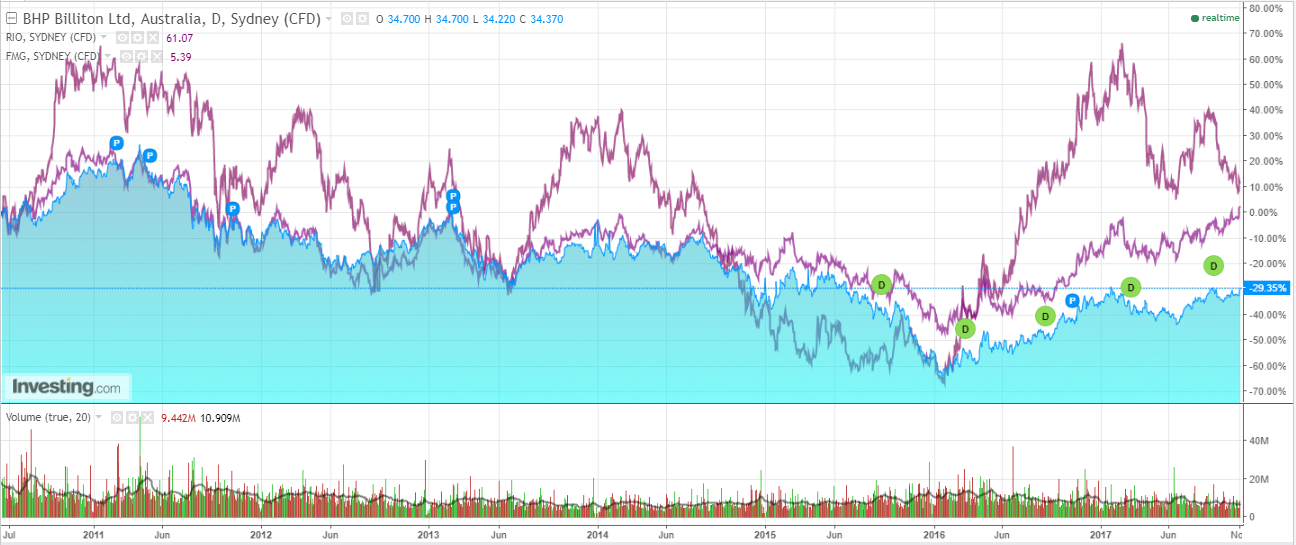

Big Iron is bifurcated with RIO and BHP’s bullish charts still running but FMG falling the other way:

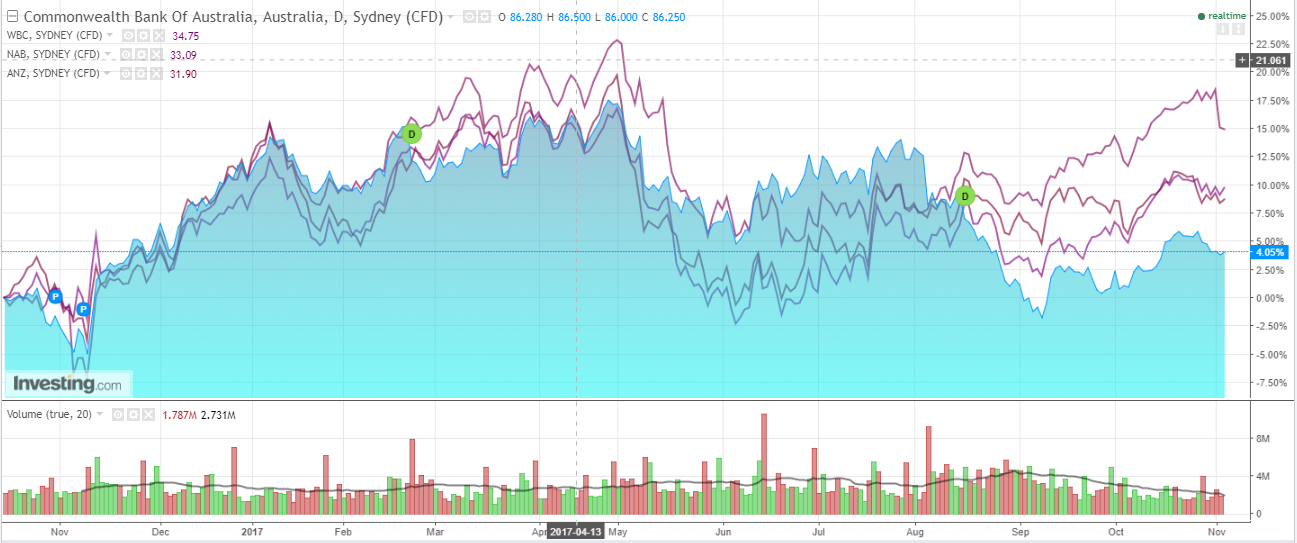

The Pensioner Killers are unstoppable:

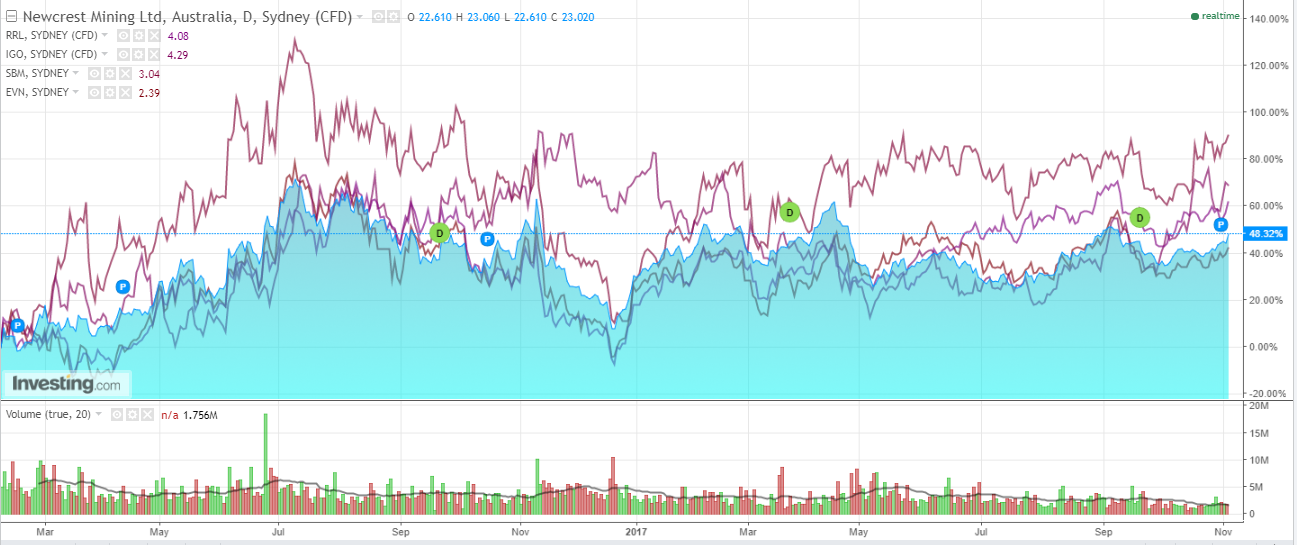

So is Big Gold:

In fact, today it’s a case of if it digs then buy it!

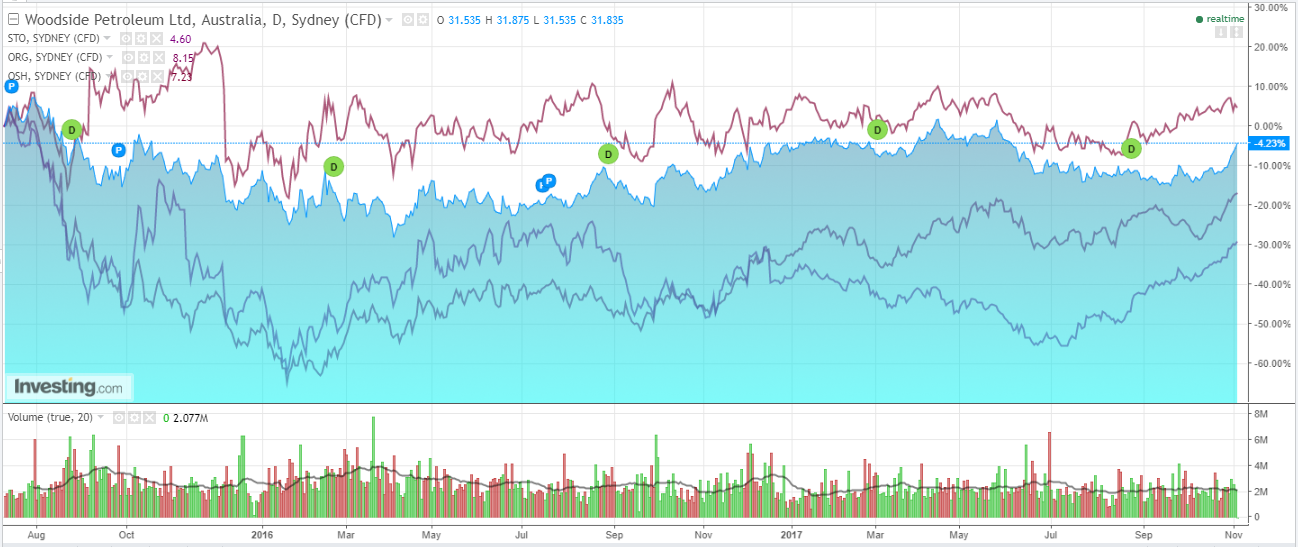

Big Sleazy is still struggling:

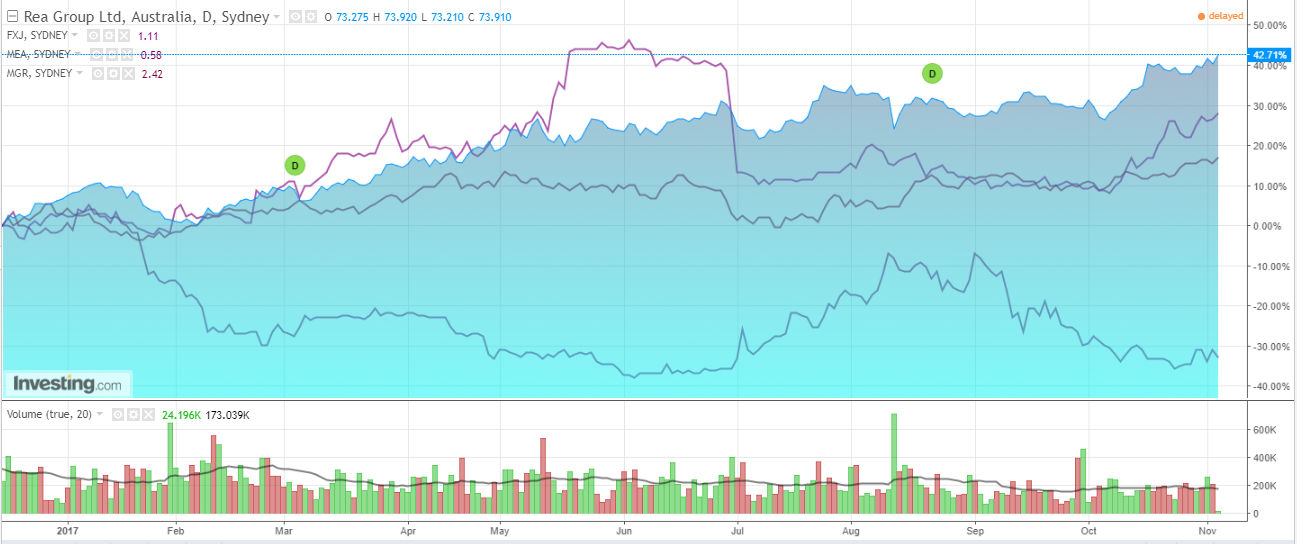

But Big Gonad is rising (ex MEA) because a property bust is sooo good for it!:

Avagoodweekend.