From Westpac late today:

Since mid October the Australian dollar has softened from around USD 0.7825 to USD 0.76. That is in line with our targeted 2017 year end level of USD 0.76. We confirm our forecast that AUD will drift even lower in 2018 ending that year at around USD 0.70.

Readers will be aware that one core driver of this deteriorating outlook for the AUD is our expectation that the overnight yield differential between Australia and the US will narrow significantly. Our target has been that by end 2018 the RBA overnight cash rate will be 38bps below the US federal funds rate.

Further, the yield differential between Australian and US 10 year bonds will collapse to zero by end 2018.

Those dynamics are now well underway.

Back in September, markets assessed the differential between the RBA overnight cash rate and the federal funds rate by end 2018 as around 40bps, a long way from our forecast of minus 38bps.

But in recent weeks that expected margin has narrowed close to zero, still a long way from our target of minus 38bps but a very substantial move in the right direction.

Equally, the spread between the Australian 10 year bond rate and the US 10 year bond rate has contracted from 55bps on September 15 to around 23bps today.

The market’s lowering of expectations for RBA hikes and relative bullish sentiment towards Australian bonds is an appropriate response to the run of recent information.

Following the below consensus Q3 CPI print of 0.6% for headline inflation and 0.35% for the core average, the ABS released the CPI reweight. Incorporating the changed weights, we struggle to see a peak in headline inflation any higher than 2.0%yr for the foreseeable future.

That belief proved to be shared by the RBA, as the November Statement on Monetary policy saw significant changes to the policy sensitive inflation outlook. Underlying inflation is now forecast at 1 ¾% for 2017; 1 ¾% for 2018; and 2% for 2019. The August forecasts had underlying inflation at 1½% – 2½% in 2017; 1½% – 2½% in 2018 and 2% – 3% in 2019.

It is our view that the decision to lower the forecasts to below the bottom of the band in 2018 and at the bottom of the band in 2019 has significant policy implications. We are now assessing a central bank which is expecting that it will undershoot its core inflation target for another year, and that, even one year out, inflation will still be at the bottom of the target zone.

We are not changing our view that rates in Australia will remain on hold in 2018 and 2019, but we have always been uncomfortable that the central bank’s forecasts were implying that it was expecting it would be raising rates in 2018. These forecasts no longer portray a central bank that expects to raise rates.

In addition to the benign inflationary environment, retail sales data showed volumes up only 0.1% in Q3. This highlights downside risk to the consumption figures in the upcoming GDP release for the September quarter.

Earlier this week, the November Westpac-MI Consumer Sentiment survey fell to 99.7 from 101.4 in October. The detail cast further doubt on the consumption outlook for Q4.

Responses to our annual question on Christmas spending plans point to moderate activity. Just under a third of Australians expect to spend less on gifts this year than last, with 54% expecting to spend about the same and just 11% spending more – the lowest proportion since we began running this question in 2009. Overall the net balance of ‘more minus less’ is marginally more negative than last year, suggesting we’re in for a repeat of last year’s lacklustre Christmas spend. The state responses show consumers in Victoria and NSW are a little less inclined to restrain spending while those in SA and WA are tilting more towards cutting back.

It is no surprise that consumers are thinking about reducing spending given their very subdued income growth. This week’s Q3 WPI data indicated that wages growth is tracking at 2.0%yr, remaining near historic lows. That was despite the Fair Work Commission’s annual wage review decision to increase the minimum wage by an above normal 3.3%. Given last year’s minimum wage rise was 2.4%, expectations were for an uplift in quarterly wages growth to 0.7%. However, the actual result came in at 0.5% reflecting softness in wages growth across the broader labour market.

Persistently low income growth is a constraint on consumer spending, particularly given the high level of household debt.

As a country that runs significant current account deficits and high associated foreign liabilities, Australia needs to offer attractive yields in order to fund these liabilities in a world where Australia’s assessed risks are not reducing. As we have discussed previously, Australia’s housing markets are deteriorating. In the main market, Sydney, house price momentum (6 month annualised) has slowed from 20% in January this year to –0.5% in October.

We are also seeing disturbing headwinds around regulation; taxes; and bank interest rates unnerve investors. This group still explains the dominant component of new lending for housing but in September, we saw a sharp 6.3% fall in lending to investors.

Australia’s reliance on foreign investors to fund our large accumulated overseas debt is dependent on offering an attractive yield or a cheaper currency. These factors will be exacerbated if there is some waning in investor confidence. Our housing markets attract relentless scrutiny from foreign investors. Recent developments in the housing market and the near term risks are unlikely to go unnoticed.

The last time Australian rates fell below US rates was in the June 1999 – December 2000 period. The yield differential ranged from minus 25bps to minus 50bps. The AUD entered that period at around USD 0.66 and gradually fell, settling at USD 0.50.

We certainly expect that the targeted yield differential by end 2018 of minus 38bps can be sustained well into 2020 as we expect the overnight cash rate to remain on hold in 2019 as well. There is some consolation in the spread, in that the Federal Funds rate is also expected to remain steady in 2019. This sustained period of a negative interest rate differential is expected to take its toll on the AUD. By mid 2019 we are looking for the AUD to move down to USD 0.68 with the risks pitched to the downside.

Currencies are not only affected by interest rate differentials and confidence. For Australia, commodity prices and the ongoing current account deficit are also important.

Back in 1999–2000, Australia’s current account deficit was averaging around 5% of GDP. We expect that over the next two years this deficit will average nearer 2.5% of GDP, thanks of course to China’s industrialisation miracle. Australia’s terms of trade are around 55% higher now than we saw during that last period of negative interest rate differentials.Overall around a cumulative US10¢ fall in the AUD is expected. We are not expecting the precipitous US16¢ fall we saw in 1999 and 2000.

So long as the terms of trade do not also plunge and they will owing to a slowing Chinese property market. A repeat of the big millennial falls is quite possible in that scenario

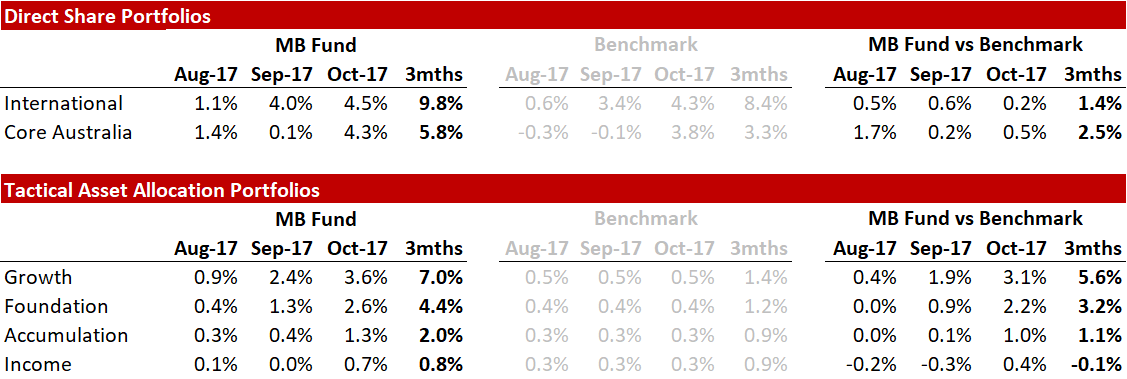

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long international equities that benefit from a falling AUD so he is definitely talking his book.

Here’s the recent fund performance:

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If the themes in this post and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.