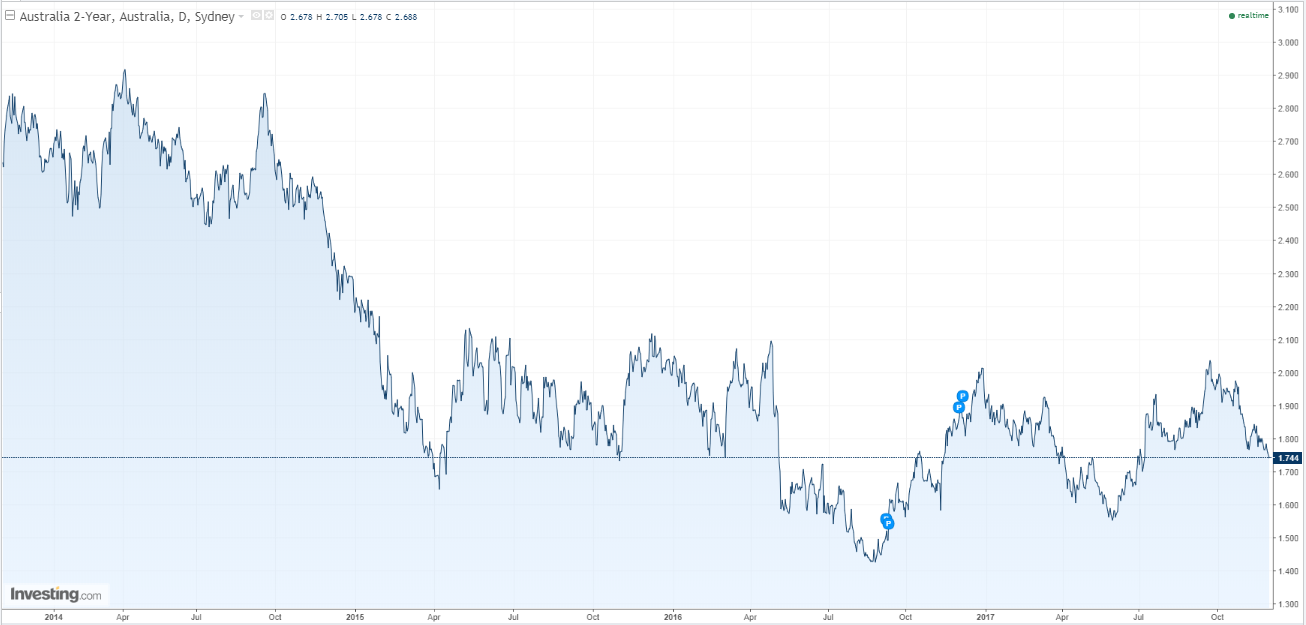

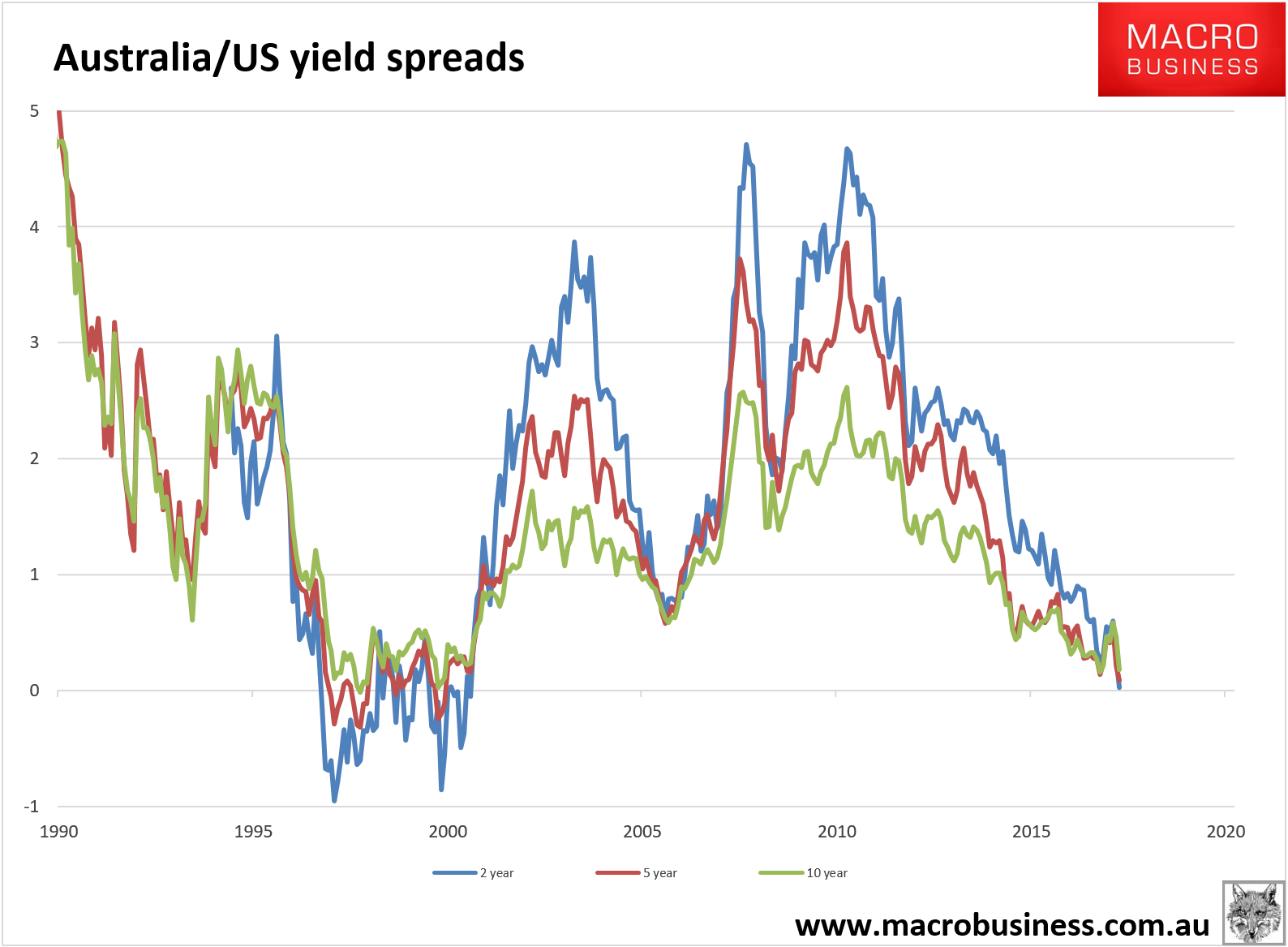

It’s happened. The 2 year Australia/US bond yield has inverted for the first time in 17 years:

There’s more ahead as US rate hikes are priced-in and Australian priced-out:

Yet the markets remain mis-priced with Australian yields higher out the curve than US:

Even though US growth prospects are clearly superior with:

- looming tax cuts;

- cheap energy and shale oil revival;

- hurricane reconstruction;

- strong asset markets;

- recovering housing markets;

- soaring consumer confidence, and

- moderate output.

Versus Australia’s:

- falling and stalling house prices;

- downdraft in dwelling construction;

- sorry consumer and retail recession;

- energy shock;

- weak asset market;

- tax hikes and

- weak output.

That makes Australian bonds a buy with pretty much everything else Australian a sell, including the currency.

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long local bonds and international equities that offer superior growth and benefit from a falling AUD so he is definitely talking his book.

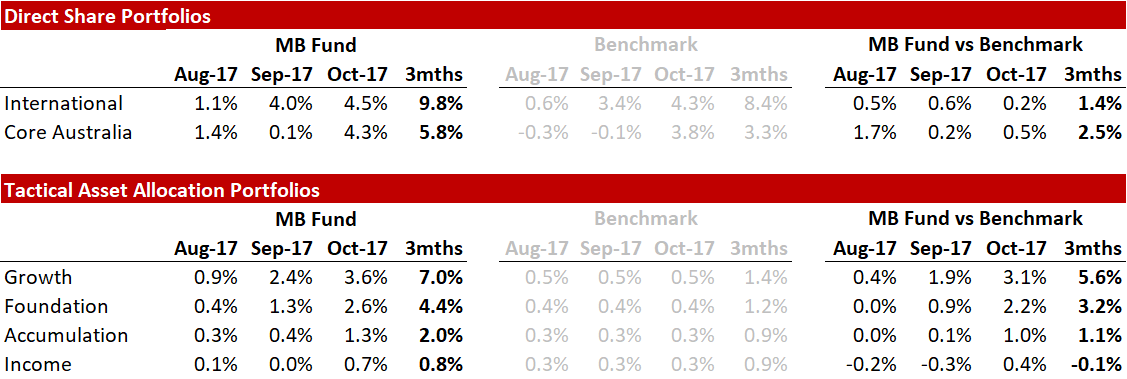

Here’s the recent fund performance:

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If the themes in this post and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.