The chief executive of the Association of Superannuation Funds of Australia, Martin Fahy, is getting nervous. He fears a ‘populist’ future government might end the compulsory 9.%5 superannuation guarantee, thereby ending the rivers of gold flowing to the sector. From The AFR:

The scenario goes something like this: a populist politician gets elected sometime in the 2020s on the back of a promise to end the super guarantee levy. This simplistic, backwards policy option hands every Australian an instant cash bonus each week equal to 9.5 per cent of their pay, less tax.

It would mark the destruction of former prime minister Paul Keating’s vision for a privatised savings system that progressively makes an increasing number of Australians self sufficient in retirement while lowering dependency on the aged pension.

Fahy, who this week hosts 1800 people at the ASFA annual conference in Sydney, worries that superannuation is becoming increasingly vulnerable to this sort of super Armageddon…

“I think all the vocal criticisms of financial services, and within that superannuation, means that the narrative that is superannuation is vulnerable to short-term populist thinking, where somebody would try to appeal to people with an offer to have a sudden increase in take-home pay at the cost of long-term retirement funding,” he says.

“We need to be conscious of that because the 9.5 per cent super guarantee levy won’t get us there. We need to get to 12 per cent. For most people, absences from the workplace and potential disruption to careers … mean we need to stay the course and play to our better selves.”

Maybe if Fahy wants to see off a populist attack on superannuation, then he and other leaders in the industry should address the extortionate fees that it charges its members.

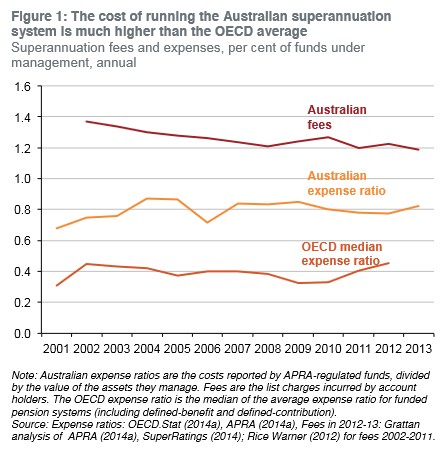

Despite the huge explosion of superannuation balances since the superannuation guarantee (compulsory super) was introduced in 1993, average fees and expenses have barely changed and are way above the OECD average, according to the Grattan Institute (see below charts).

As noted by Grattan:

A larger system of larger funds should have incurred lower costs and charge lower fees, because big funds have lower costs…

Australian funds charge fees that are three times the median OECD rate, on average… Many countries have superannuation pools much smaller than Australia’s, yet their funds charge customers much less.

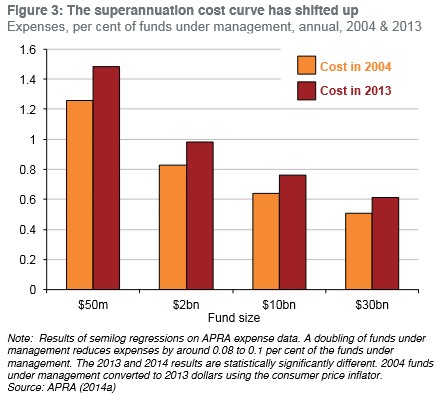

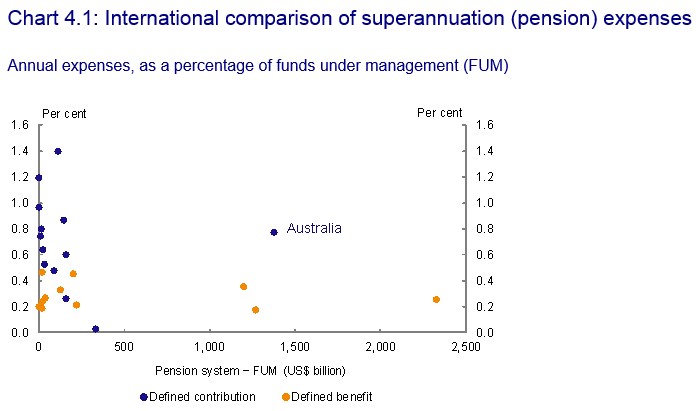

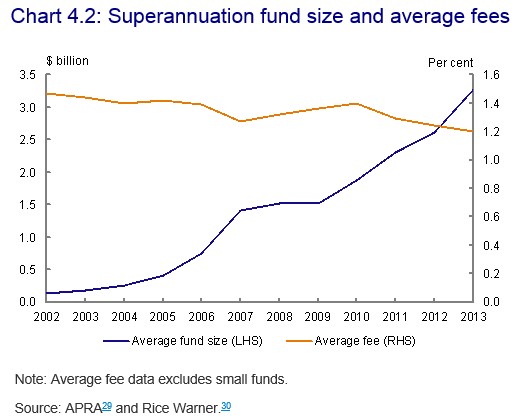

The Draft Report of the Murray Financial System Inquiry noted similar concerns, as illustrated in the below charts:

And that super fees had not fallen in line with what could have been expected given the substantial increase in scale:

If superannuation was a well functioning and competitive market, average fees would have fallen as the value of funds under management has risen. This is because it should not cost ten times more to manage $1 billion of funds under management than it does to manage $100 million – the economies of scale argument cited above.

The fact that fees have not fallen suggests that Australia’s compulsory superannuation system is working more for the benefit of its industry players than for its members, with Australia’s compulsory contributions (currently set at 9.5% of employee wages) providing the industry with a “sheltered workshop” by which to operate, as well as an ever-growing pool of funds under management to ‘clip the ticket’ on and earn fatter profits without even trying.

The argument that compulsory super relieves pressure on the Aged Pension is also spurious, as noted in the Intergenerational Report [my emphasis]:

In 2013-14, around 70 per cent of people of Age Pension age were receiving the Age Pension. Of these, 60 per cent were in receipt of the full-rate pension. As Australia’s superannuation system matures, and compulsory contributions increase, many Australian workers will retire with much larger superannuation balances. The proportion of part-rate pensioners relative to full-rate pensioners is expected to increase. The proportion of retirees receiving any pension is not projected to decline.

Despite a lifetime of compulsory contributions, the superannuation system is not projected to significantly reduce reliance on the Aged Pension. Sure, there would be less people on the full Aged Pension and more claiming the Part Pension, but not nearly enough to justify the huge and growing costs to the Budget from superannuation concessions.

In any event, Fahy’s argument to raise the super guarantee to 12% is hardly surprising. After all, more funds under management means more fees to be gleaned and more profits.

Unfortunately, it would also be very poor policy.

The cost of compulsory superannuation contributions falls on the employee, not on the employer, and any increase in the superannuation guarantee will lower one’s take home pay. This point was explicitly acknowledged by the Henry Tax Review when it stated:

Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement.

Given this fact, I do not believe that forcing lower income earners to sacrifice more of their pay into superannuation would improve their living standards. Many are already struggling with the high cost of living, so it makes little sense to reduce their disposable incomes even further.

The Henry Tax Review agreed, which is why it recommended that the superannuation guarantee be retained at its current level, not raised to 12%:

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners.

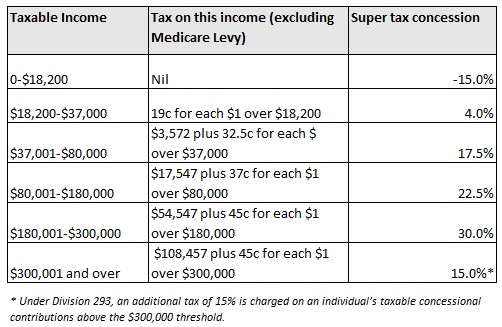

If the superannuation industry genuinely cared about ordinary Australians, rather than it’s own profits, it would instead be lobbying to change the current 15% flat tax on superannuation contributions/earnings to something more progressive. The current 15% flat tax system is highly regressive and provides the lion’s share of benefits to upper income earners, while providing minimal benefits (or penalising) lower income earners (see below table).

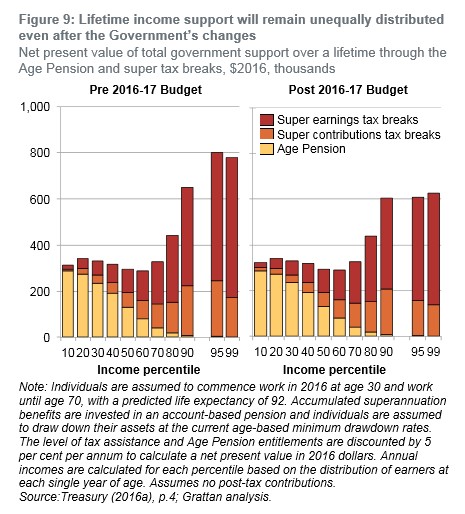

Indeed, even following the Turnbull Government’s recent modest super reforms, high income earners continue to make out like bandits (right panel below):

As noted by the Grattan Institute:

Before the changes, someone in the top 1 per cent of income earners could expect to receive two and a half times as much in tax breaks from super over their lifetime as a retiree with no assets receives in pension. This is also two and a half times as much as the average income earner receives in pension and super tax breaks combined. The Budget changes merely trim the worst of these excesses: the top one per cent now receives just twice as much as low or average income earners.

So, by making the super concession system more progressive, lower income earners would enjoy a boost in their retirement savings without incurring a reduction in their take home pay.

Further, without changes to the way that superannuation concessions are distributed, higher income earners would gain even bigger tax benefits under a 12% superannuation guarantee, whereas those at the lower end of the tax scale would receive minimal benefits (again, see above table and chart).

Again, let’s not forget that tax concessions on superannuation already cost the Budget an inordinate sum, and are growing rapidly. Raising the superannuation guarantee to 12% would mean they become an even bigger Budget drain over time, whilst doing little to boost superannuation savings for lower income workers – those most likely to become reliant on the Aged Pension.

In short, raising the superannuation guarantee to 12%, without reforming the way that contributions/earnings are taxed, would merely heighten inequities already present in the system. It would rob younger (and lower paid) workers of much-needed disposable income and worsen the long-term sustainability of the Budget.

About the only winners from such a policy would be the superannuation industry rent-seekers, which would get to ‘clip the ticket’ on more funds under management and earn fatter profits.

unconventionaleconomist@hotmail.com