Yes, yes, we all know that MB is the Australian doomsayer. Except of course we’re right that the economy sucks and the world’s worst share market represents that nicely. UBS today shows why it sucks too:

Australia Lacking Earnings Leverage

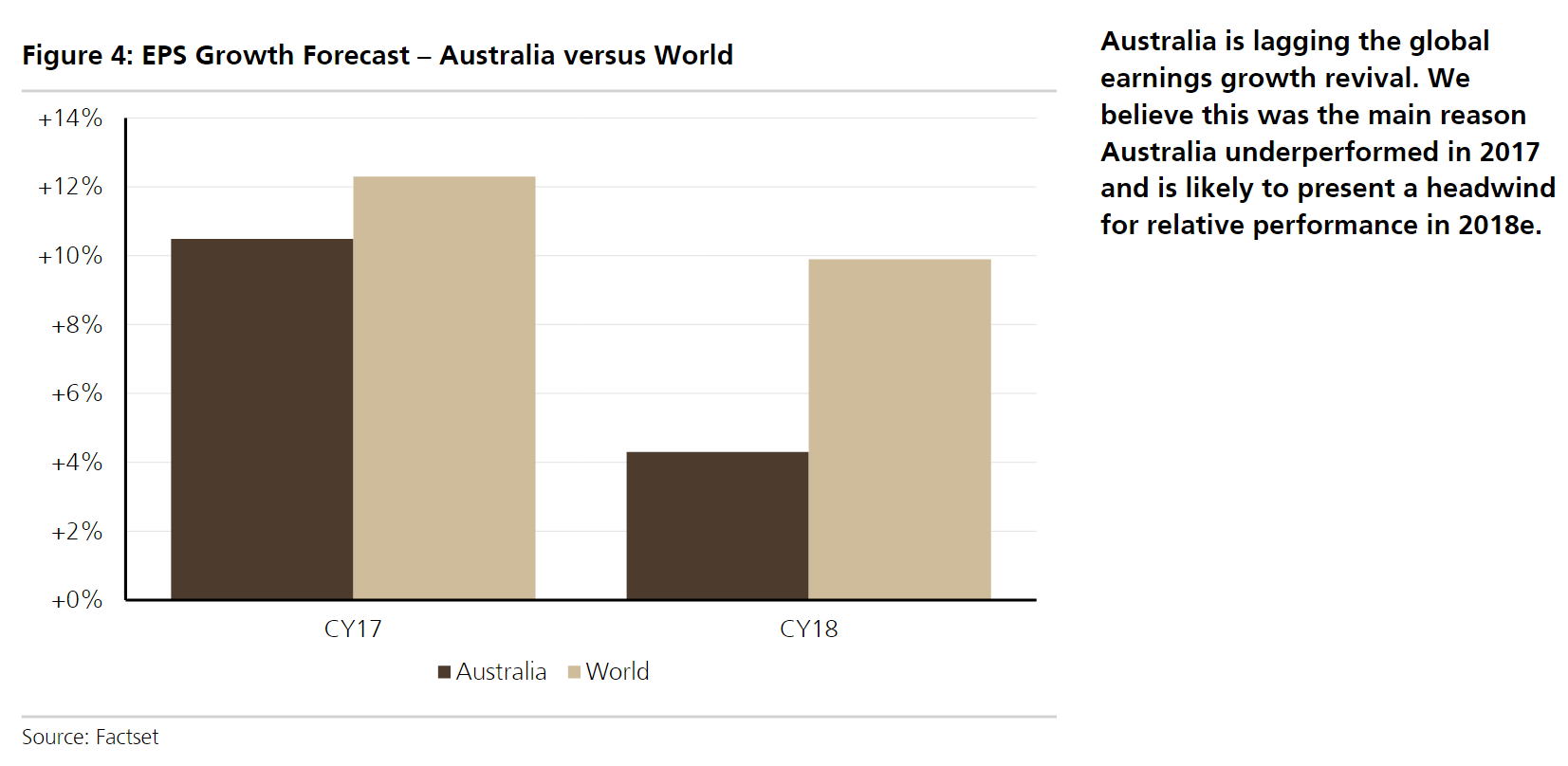

2017 was a strong year for global and regional equities. Australia has lagged the global rally but at this point looks on track to deliver a total return of 9.5% for 2017, which is close to the long-term average and well above cash and bond returns.

Our global equity colleagues covering the US, Europe and Asian equity markets are looking for the bull market to extend through 2018 with another year of aboveaverage returns driven by above trend EPS growth.

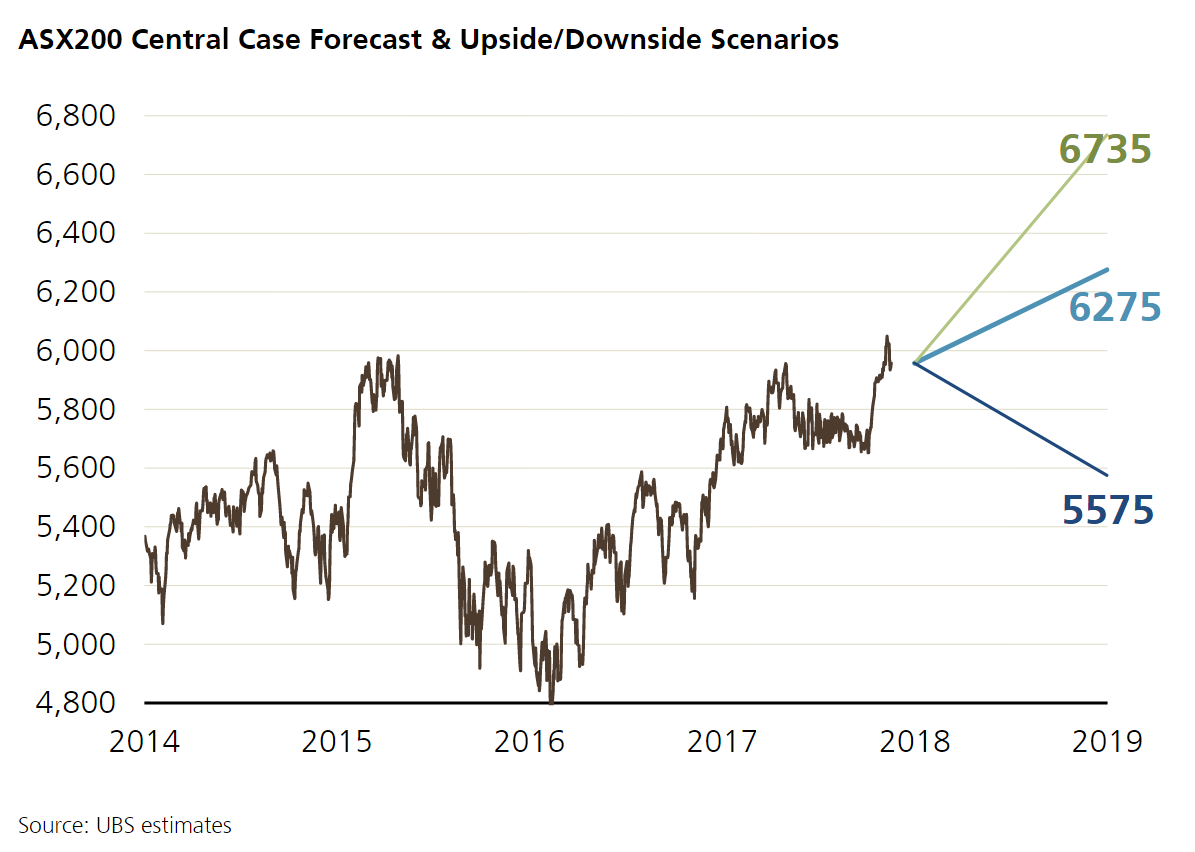

Under this scenario we continue to see Australia as a laggard (on a local currency basis) though the market appears capable of posting another trend-like return (8- 10%).

Once again Australia’s key relative headwind is likely to be comparatively sluggish EPS growth relative to what UBS expects to be posted globally and regionally.

We think the current consensus of c5% EPS growth in FY18 and CY18 looks about right (possibly some upside in resource estimates). This also looks like a reasonably good estimate for capital gain potential, in our view. Further re-rating into a maturing bull market is not without precedent, and equities continue to offer relative value versus bonds, but we pitch our central case return target with the assumption that the already above-average P/E ratio holds fairly steady.

The bullish global underpinning for equities is premised (in part) on continued solid global GDP growth (3.8% in 2018e) being once gain converted to above-trend global EPS growth (est. c10%). Global inflation is forecast to rise, but only modestly, with US 10-year bond yields expected to rise modestly to 2.7%.

While Australian GDP growth is forecast to do a little better in 2018, Australian Economic Perspectives: Outlook 2018 the composition of this growth (slower consumer and slower housing) combined with the long bank/short IT composition of the Australian stock market means that Australia is unlikely to produce the double digit EPS growth expected in other regions. The fact that Australian earnings growth expectations are more moderate could be taken positively, though UBS does not see much downside risk in global estimates (with upside risk in Europe and Japan).

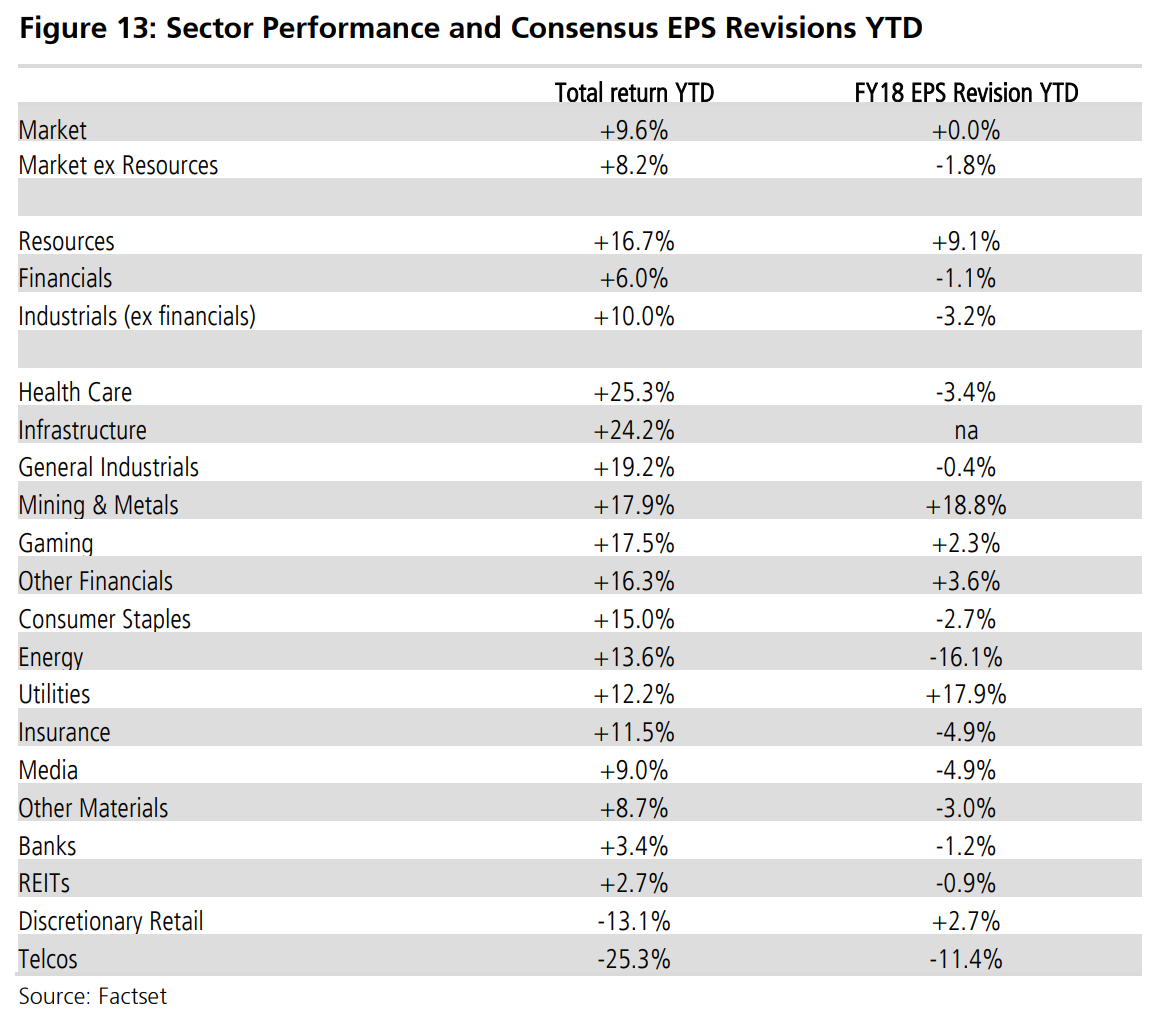

Resources Have Potential For Earnings Upside

We believe the Australian resource sector does present as a source of some potential upside to 2018 earnings estimates, as was the case in both 2016 and 2017. A simple mark-to-market of current spot commodities would suggest earnings upgrades in the order of 20-30%.

We retain our overweight in resources, in part due to an expectation of solid global growth supporting commodity prices, but also because of relatively undemanding valuations and the ability the resource sector to act as a hedge against rising inflation and interest rates. Indeed we see resources as a more effective hedge than Australian financials (in contrast to other markets).

Reasonably Priced With Conservative Estimates?

We still see the resource sector as relatively cheap with good cash-flow generation potential. The sector was able to outperform despite the iron ore price falling from c$80 to c$60 in 2017. Base metals did well while the oil price also revived, rising from moderately over 2017 albeit it hit a low of $45 in June.

Spot commodity prices for iron ore, copper and oil each sit c5-10% above the 2018 consensus. A simple mark-to-market of current spot commodities would suggest earnings upgrades in the order of 20% though UBS official estimates are close to consensus.

The UBS commodity price profile for 2018e is flat to marginally down (which admittedly rarely happens in practice) but flat prices would be more than enough to support the strong cash-flow story. Spot commodities are generally a little above our long-term estimates though the oil price is still below. We have a preference for energy on a view that the spot price of oil is still below long term pricing and the implicit linkage of oil demand to global over China growth. We prefer Origin Energy and Woodside Petroleum.

The macro backdrop of decent global growth and moderately higher rates should be supportive for the resource sector though our expectation of some China slowdown complicates the decision, particularly for the China-centric iron ore market. Recent China feedback from our mining and commodity team is that the key drivers of the China commodity demand cycle, such as property and infrastructure, are entering 2018 with relatively solid order books, so demand is likely to hold up. As discussed, we are assuming flat iron ore prices with an ongoing wide quality spread (supported by high steel margins) which is supportive for our overweights in BHP Billiton and Rio Tinto. In mid-caps we prefer Iluka Resources (mineral sands) and Independence Group (nickel).

Banks Trimmed To Neutral

Post the recent marginally disappointing bank sector reporting season we have edged our moderate overweighting in banks down to neutral. We prefer “other financials” where we think there is leverage to higher rates and buoyant capital market conditions. We remain underweight REITs but less so than this point last year given better relative valuations.

Banks Relative Value Look Reasonable But Growth Is Constrained

Australia’s largest sector has lagged the market this year after a good 2016. Closer inspection of the year’s performance shows the weakness was concentrated in May/June following the surprise Federal Government bank levy. The tax is not likely to be a huge impost in terms of the EPS hit – UBS downgraded by less than 2% based on an assumption of some repricing clawback. However, the move did hit confidence toward the sector. APRA’s more ‘benign than feared’ capital decision in July briefly ignited interest in the sector, though CBA’s AML disclosures in early August short-circuited the revival. While policy and regulatory announcements have added volatility this year, from a fundamental perspective the sector has underwhelmed. Ex ANZ (FY17 growth was boosted by previous year write-downs) sector growth was 2.5-3.0%. This was a little disappointing given the benign state of the domestic macro cycle and still decent system credit growth.

We were looking for some moderate upside surprise in the recent results season – however results generally proved underwhelming. This may be due in part to temporary factors such as soft markets and wealth income, but we were still left uninspired. Valuations appear a little on the cheap side but earnings growth does look constrained at c2-3% while bad debts seemingly can’t go any lower. We are left feeling decidedly neutral on the sector.

One unknown factor for 2018 is how the sector might perform against a backdrop of higher global interest rates. The sector did very well in 2016 as bond yields rose, rallying alongside global banks. The P&L impact of higher bond yields for Australian is minimal. To the extent that better growth suggests better credit growth and lower bad debt risk, some rally could be justified. However we think the leverage from better global growth to Australian bank profitability is likely to be weak. Australia’s Achilles heel of high household debt is vulnerable to higher domestic rates. To the extent that higher long bond yields foreshadow higher cash rates, then Australian banks have that implicit vulnerability. We could see a shortterm rally on rising global yields but are more inclined to gain exposure to this theme through the “other financials” (QBE Insurance Group, Computershare).

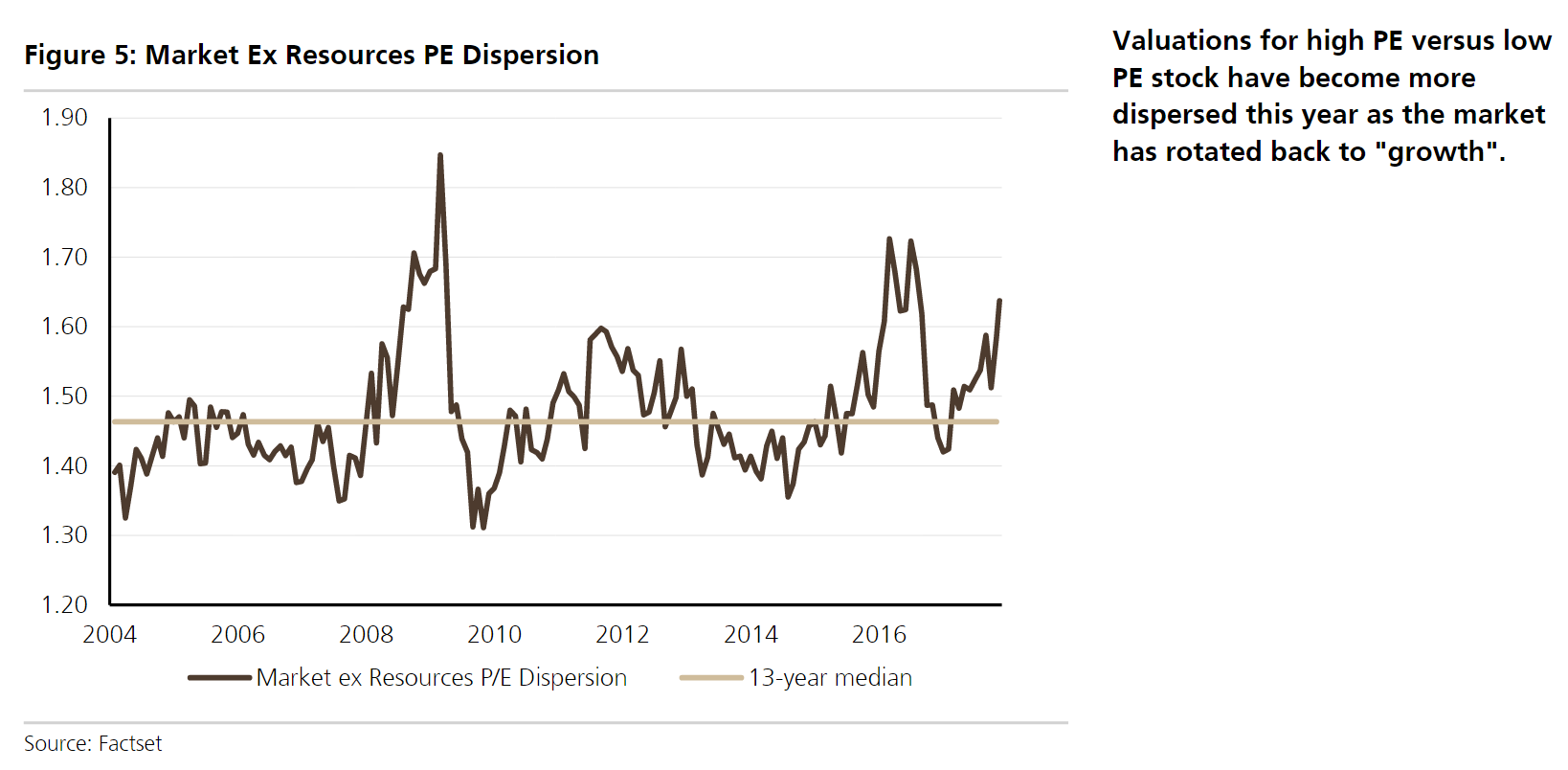

Growth Scarcity Causing Some Big P/E Rates

When looked at from a sectoral rather than aggregate earnings growth perspective, Australia’s lack of IT has been a comparative disadvantage. Our US equity strategist remains constructive on US tech while our Asian strategist is selectively constructive on Asian IT (particular the key China internet plays). Therefore, Australia is still likely to run into this headwind in 2018, albeit perhaps not to the same degree as in 2017. Australian investors have appeared to respond to the lack of IT exposure and generally sluggish market EPS growth by re-rating those select areas of the market that are perceived to have either structural growth, or the prospect of durable cyclical upturns (e.g. infrastructure exposed and mining services). Healthcare has been the strongest performing sector in 2017 led by market heavyweight CSL

Small caps have been bid up this year based on the growth themes of IT, the China consumer and mining services. The bond yield sensitive infrastructure trusts have also made significant comebacks this year, with bond yields drifting lower. This follows the bond yield induced sell-down of H2 2017.

Will The Bond Market Spoil The Growth Stock Re-Rate?

We see global bond markets developments as likely to be a key potential swing factor for sector rotation. The UBS house view is for a very moderate rise in long bond yields based on a three Fed tightenings in CY17 (the third due in December) and two tightenings in 2018, based on a very moderate lift in inflation.

We don’t see sufficient momentum in the domestic economy to trigger a big move in domestic cash rates. UBS expects one RBA rate rise in the second half of 2018. Notwithstanding the very benign domestic policy outlook, the direction for Australian long bonds is likely to come from US/Europe, as is typically the case. Therefore we see Australian 10 year yields edging higher in 2018e (2.9%).

Clearly a bigger move in bonds would have significant implications for sector rotation as we saw in 2016, though it may not necessarily be negative for the overall market as we also saw in 2016. The equity market in aggregate still appears to contain some buffer for higher rates.

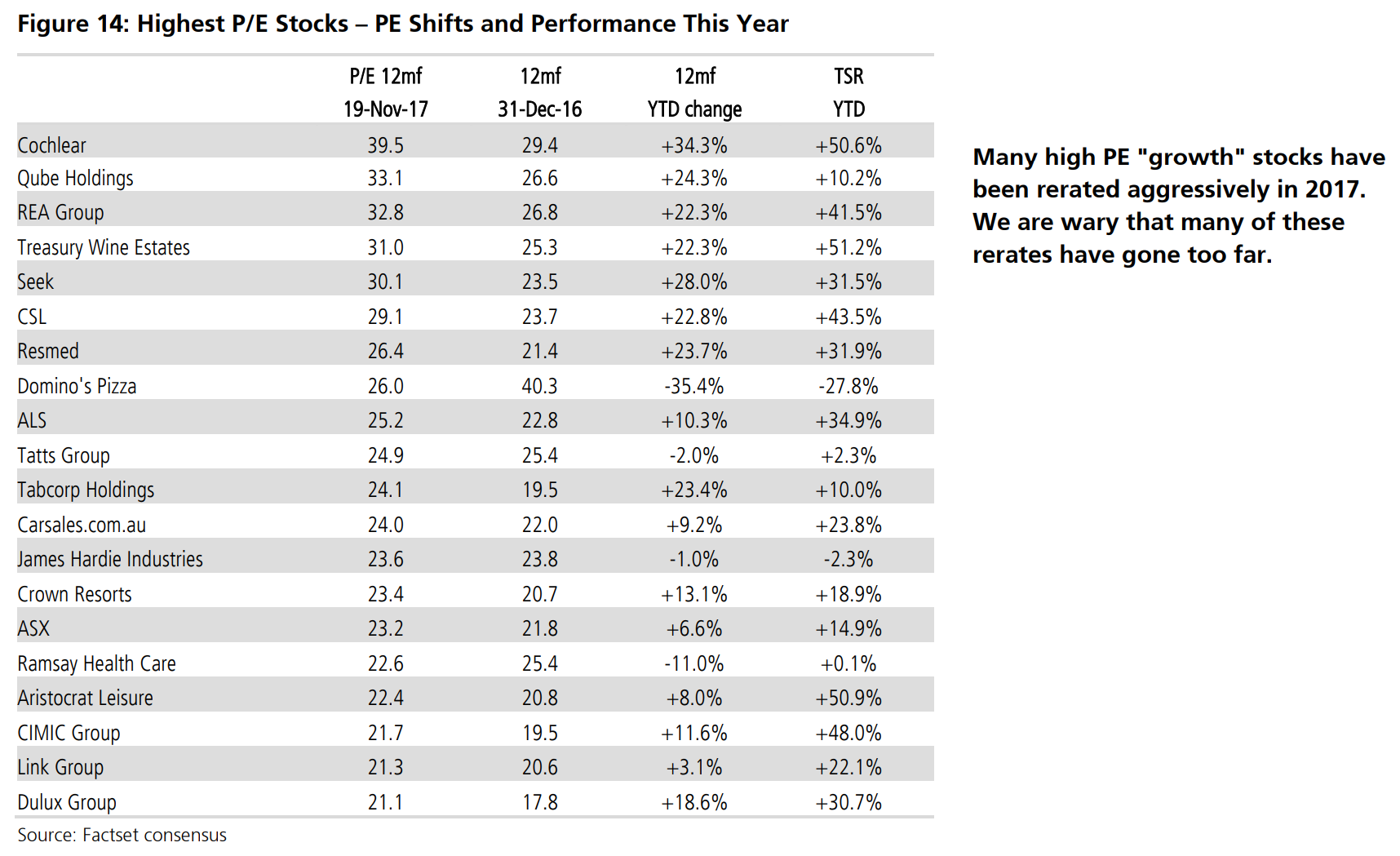

Aside from the potential impact from a shift in the long bond, we think the bar has been raised for “growth” from a stock specific standpoint with a lot of good news priced into to many stocks as we head toward the February reporting season. We hold some industrial GARP stocks in our model portfolio (e.g. Aristocrat Leisure, Brambles, Star Entertainment Group, Woolworths) but in general prefer resources and other financials (Computershare, Link Group, Macquarie Group, QBE Insurance Group) to highly priced growth plays.

In short, in the ASX you’re paying through the nose for no growth with big risks from a China slowdown and housing bust.

There are better options elsewhere.

Advertisement

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long international equities that offer superior growth and benefit from a falling AUD so he is definitely talking his book.

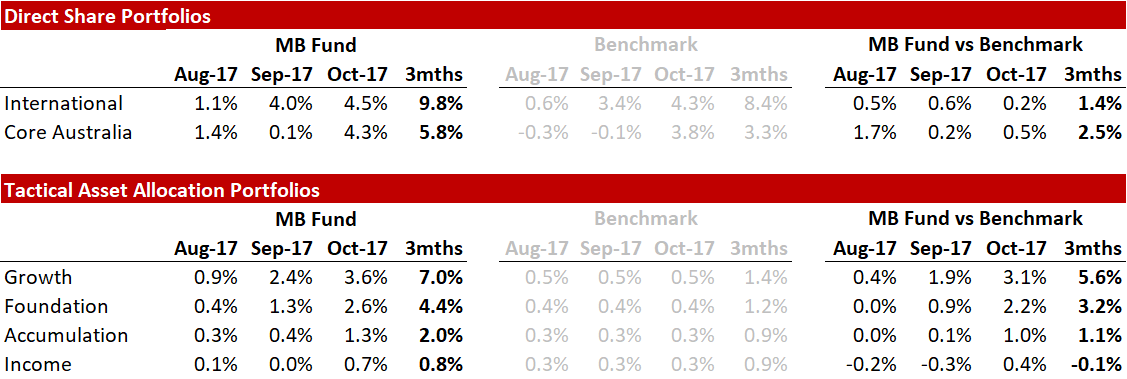

Here’s the recent fund performance:

Advertisement

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If the themes in this post and the fund interest you then register below and we’ll be in touch:

Advertisement

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.