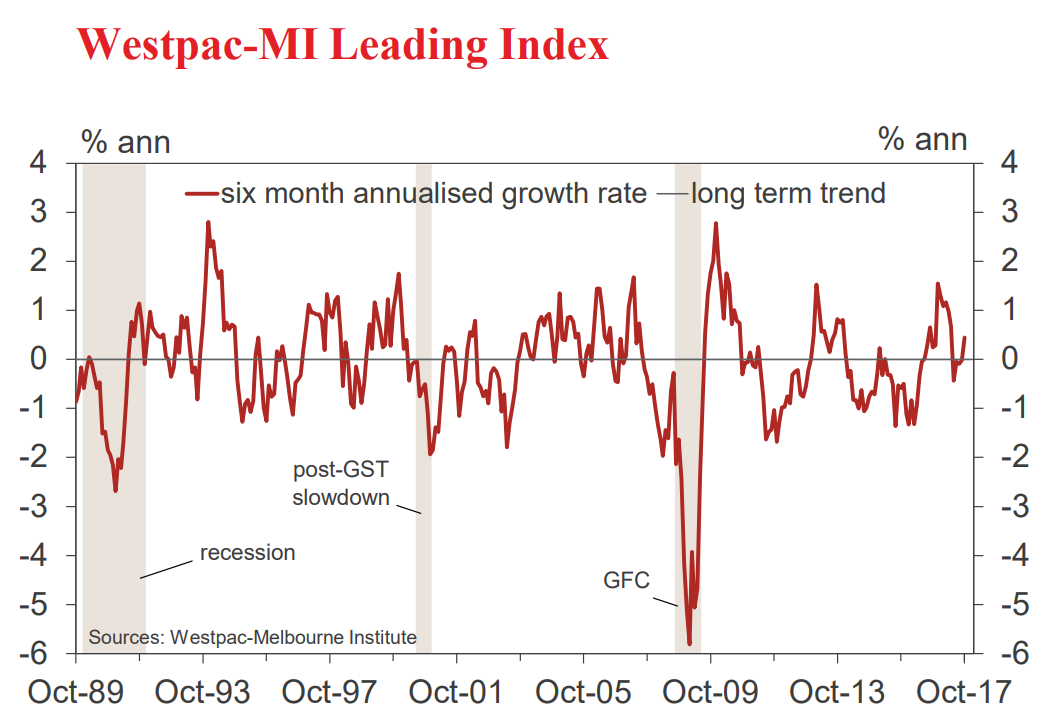

• The six month annualised growth rate in the WestpacMelbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, lifted from –0.02% in September to +0.44% in October.

This is the first above trend reading on momentum since mid-year and suggests some of the headwinds to growth evident earlier in the year have eased. That said, the signal still looks fragile in our view with key negatives around commodity prices, housing, labour market conditions and the consumer likely to contain any upswing in 2018.”

While having recovered, at least temporarily, from the slow patch in June – September, the growth rate in the Index is still below its level six months ago in May. In May, the growth rate printed +0.67% compared to today’s reading of +0.44%. The main shifts in component contributions over this period have been from renewed softness in commodity prices in AUD terms (–0.24ppts), slowing growth in US industrial production (–0.19ppts) and a more mixed performance from the S&P/ASX200 (–0.16ppts); partially offset by a widening yield spread (+12ppts) and small improvements in other components (adding +0.24ppts on a combined basis).

The Reserve Bank Board next meets on December 5. The Board is certain to keep rates on hold for the 15th consecutive meeting. The Reserve Bank released its November Statement on Monetary Policy on November 10. There were some significant changes in the Bank’s forecasts in this document. The Bank lowered its forecast for underlying inflation in 2018 to 1.75%, below the bottom of the 2–3% target zone. This compares with the forecast in the August Statement of 1.5–2.5% (a mid-point at the bottom of the target zone). Furthermore, it is now forecasting underlying inflation at 2% in 2019 – down from 2–3% in August.

It continues to forecast growth of 3.25% in 2018 – 0.5% above potential growth of 2.75% although it has lowered its forecast for growth in 2019 from 3–4% to 3.25%.

Our interpretation of these forecast changes is that whereas in August the Bank expected to be raising rates some time in 2018 that prospect is now much less clear. 22 November 2017.

In fact, if their lower inflation forecasts prove correct the Bank is unlikely to move in 2018. Markets and most commentators continue to expect a higher cash rate in 2018, although this conviction has eased in recent weeks. We are maintaining our long held view that rates will remain on hold through 2018.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.