Should Australia end dividend imputation to fund company tax cuts?

The AFR has published an interesting article canvassing ending (or reducing) Australia’s unique dividend imputation system to fund company tax cuts:

…abolishing dividend imputation entirely… would generate $11.1 billion a year at the 30 per cent rate.

But that would be howled down by investors, who would lose credits for tax already paid at the company and therefore face individual tax rates of up to 75 per cent on distributed dividends.

With this in mind, the Australian National University scholars suggest a discounted tax rate on dividends. Indicative modelling under a “half franking” scenario indicates this would raise enough to pay for the Enterprise Tax Plan, which Treasury says will cost about $4 billion a year.

“Its time to seriously examine the structure of our company tax system and not just the rate,” ANU Tax and Transfer Policy Institute director Miranda Stewart said.

“We think it is plausible that you could finance a cut to 25 per cent by removing dividend imputation and replacing it with a discount on dividends.”

In the absence of another strategy, funding the lower 25 per cent rate will be a matter of taking on additional debt, raising other taxes (bracket creep or the GST, for example) or cutting spending on services…

The idea certainly has merit.

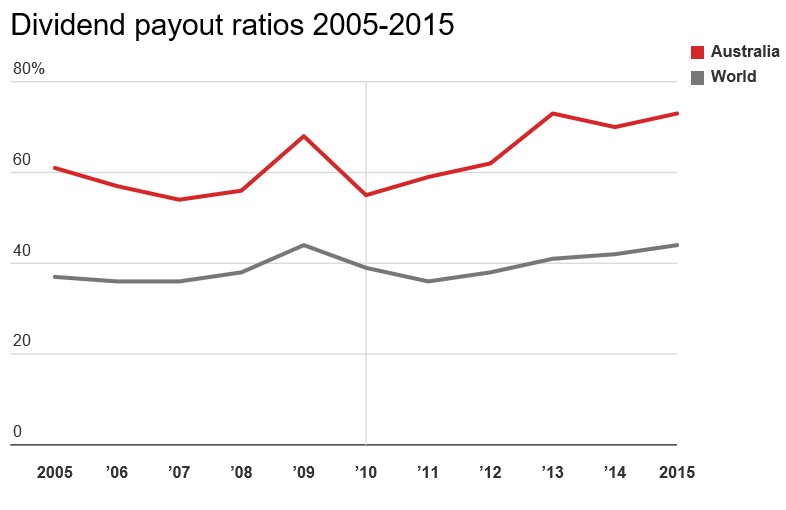

First, as argued by Paul Docherty, Senior Lecturer as the Newcastle Business School, Australian firms have high dividend payout ratios by international standards, and these have grown consistently faster than earnings over recent years.

The average firm around the world currently returns less than half of profits to shareholders, whereas Australian firms return more than 70%:

This high payout ratio in Australia arguably comes at the cost of economic growth via less business investment. That is, the increased demand for dividends within an imputation tax system restricts firms’ access to their preferred source of financing: retained earnings.

Second, one of the reasons why Australia’s dividend imputation system is costing the Budget dearly is thanks to the fateful decision in 2000 by former Treasurer, Peter Costello, which allowed the conversion of franking credits into cash refunds for shareholders. This enabled tax-free (mostly wealthy) superannuation holders over the age of 60 to claim imputation credits even though they pay no tax. The Australia Institute explains:

When companies pay dividends to Australia shareholders out of after-tax profit, shareholders also receive ‘franking credits’ which are a credit against their own tax obligation and based on the tax paid by the company. This system, known as ‘dividend imputation’ is unusual and only 4 other countries in the world use it.

However, in 2000 Mr Costello made the system even more generous to shareholders by allowing them to get a cash refund if they receive more in ‘franking credits’ than they actually owe in tax. Because income from superannuation is tax free for people over 60, high income retirees can use franking credits to get a cash gift of over 40 cents for every dollar they receive in dividends.

The ATO estimates that Peter Costello’s decision to allow ‘excess’ franking credits to be refunded as cash cost $4.6 billion in 2012-13.

Third, the current dividend imputation system effectively discriminates between domestic and foreign investment. This is because domestic investors receive franking credits, whereas overseas investors do not. If the government was to eliminate (or reduce) dividend imputation, and replace it with a lower company tax rate, it would remove (or reduce) this distortion in a revenue neutral way.

At a minimum, Peter Costello’s changes in 2000 should be unwound so that investors should only be allowed to offset franking credits against tax that they have paid.

If the goal of dividend imputation is purely to avoid double taxation, then it makes absolutely no sense to allow retirees paying zero tax on their superannuation earnings to then also receive cash refunds for their franking credits. Such a situation is not only inequitable and effectively a subsidy to the (mostly) rich, but the cost to the Budget is simply too high to be ignored.

unconventionaleconomist@hotmail.com