I have previously argued that Australia’s private health insurance system is facing forces similar to the electricity “death spiral”, which arises when demand for power declines, due in part to customers taking up solar, leading to higher prices to cover fixed network costs. That is, the more people that take-up solar power, the faster decline in electricity demand, and the more fixed costs must be spread over a smaller volume of electricity, raising costs for everyone else.

Recently, actuary Jamie Reid claimed that many Australians would soon find it cheaper to pay the Medicare Levy Surcharge than to have private health insurance.

The surcharge is meant to penalise high-income earners who do not have health insurance, but Reid noted that the combination of higher insurance premiums and a reduction in the impact of the health insurance rebate is making paying the surcharge an increasingly attractive alternative. As a result, more people may opt out of health insurance, placing more pressure on the public health system.

In an attempt to avert the ‘death spiral’, the federal government recently announced that young Australians would be targeted with premium discounts in a bid to arrest falling memberships and ensure the overall financial viability of the system.

Last week, The Australian reported that the rate of private hospital cover continues to fall ahead of the new measures:

The latest figures from the Australian Prudential Regulation Authority, released yesterday, put hospital cover at 45.8 per cent of the population in the September quarter, down from 46.1 per cent in June. That is the lowest rate of coverage since early 2012, a downward trend blamed largely on the cost of premiums and erosion of the government rebate.

And today, The Australian reports that Australians are losing faith in the private health system:

Consumer confidence in private health insurance as value for money continues to fall as more people place their trust in the quality and service provided in the public system…

The industry head said that in a time of slow wages growth people were starting to focus on private health insurance as a burden on the family budget rather than an investment in their future health security…

The research has also showed that for the first time people are more confident in the quality and services provided by public hospitals than the private sector…

It’s hard to see how the ‘death spiral’ can be avoided.

Premiums continue to rise every year, which comes at a direct cost to the federal budget of some $6.5 billion. At the same time, consumers continue to view private health insurance as poor value for money.

As more younger Australians perceive that it is cheaper to simply pay the penalties than hold private health insurance, they will continue to exodus from the system. This will leave the private health system with a larger proportion of unhealthier, older, expensive users, forcing premiums up and leading to a further exodus of the young, and so on.

Not that the ultimate collapse of private health insurance would necessarily be a bad thing.

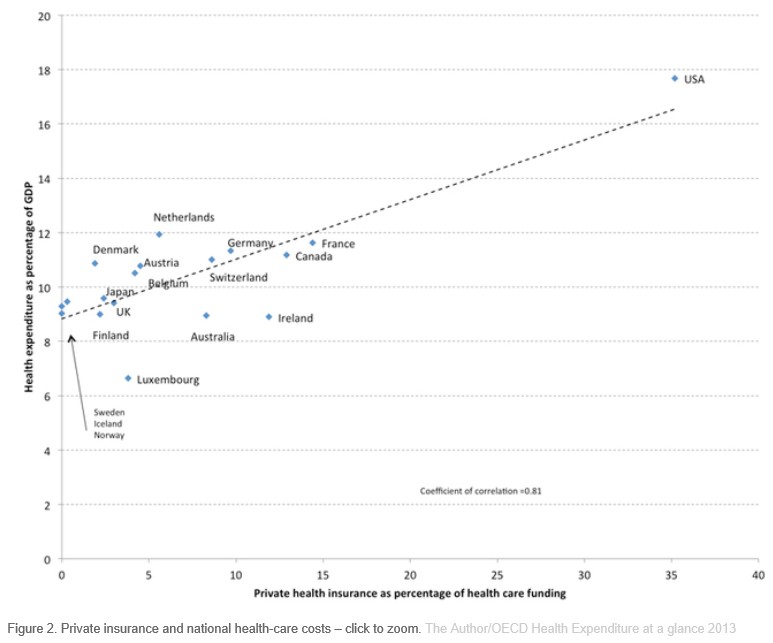

There is no evidence that private health insurance buys patients extra quality and safety. The Productivity Commission (PC) found that the larger, most comparable public and private hospitals had similar adjusted premature death ratios. Further, the PC found that the team-based care in large public hospitals also leads itself to better coordination of care.

In fact, in Australia’s case, private health insurance is likely raising overall health costs. This is because the high financial overhead of private insurance means that only 84 cents in every dollar collected by private insurers is returned as benefits, with the rest going to administrative costs and corporate profits. By contrast Medicare returns 94 cents in the dollar, even after the cost of tax collection is taken into account.

A single national insurer, like Medicare, also has the monopsony buying power to control prices demanded by powerful service providers.

Diverting subsidies away from private health insurance into the public system might actually lead to more efficient health outcomes.