Just as Australia’s bank-owned superannuation funds are calling for greater competition and more choice, Australian Prudential Regulation Authority (APRA) member, Helen Rowell, has given a speech to the Association of Superannuation Funds of Australia conference in Sydney, whereby she expressed unhappiness at the “astonishing” complexity of Australia’s superannuation system which is “certainly not [working] in the best interests of those fund members”:

If growth trends persist broadly in line with the past five years, by 2022 the superannuation sector will be managing roughly $4 trillion on behalf of Australians, give or take a few billion.

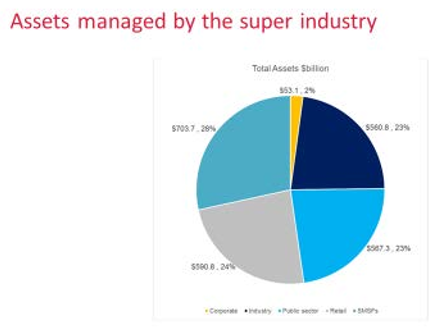

As of September 2017, the breakdown of the current $2.5 trillion of assets managed by the industry was:

2.1 per cent in corporate funds;

22.2 per cent in industry funds;

17.0 per cent in public sector funds;

23.4 per cent in retail funds; and

27.7 per cent in self-managed super funds…

[An] area that warrants consideration as part of any member outcomes assessment is the number and nature of the different investment options that are offered to fund members. Australians in 2017 have the option of choosing between 209 super funds; and within those funds there are an astonishing forty one thousand [41,000] investment options. That’s an average of 196 investment options per fund.

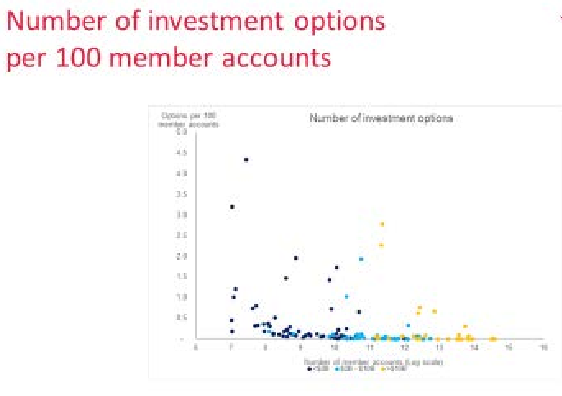

This graph plots the number of investment options per 100 members for different size super funds, colour coded by size of fund as for the previous slides. (A few outliers have been excluded.) You can see from the number of dark blue dots on the left-hand-side of the graph that it’s generally smaller funds that offer more options per 100 member accounts. When looking at this data, the obvious question it raises is whether those smaller RSEs offering a large number of options for their membership have the capacity and resources to properly manage this degree of investment complexity.

From the member’s perspective, the question is: at what point does the level of choice become more a headache than a help? It seems legitimate to ask why the industry offers members an average of nearly 200 investment options when many funds have a significant proportion of members in their default MySuper products and hence relatively few members in each of the many choice investment options on offer. And that is particularly the case when many of the options don’t appear to be markedly different in their asset allocation or risk/return characteristics.

I have previously expressed the view that there are too many investment options within super. Research published in 2015 out of the University of Pennsylvania concluded that over a 20-year investment horizon, funds that provide an excessive number of investment choices reduce member value by nearly $10,000; a not unsubstantial financial hit, given the average fund balance for the industry is $55,7776, and certainly not in the best interests of those fund members.

Under APRA’s proposed member outcomes assessment, and as part of sound strategic and business planning, we would expect trustees to seriously consider the optimal number of investment options they should be providing to efficiently deliver quality outcomes for members. Might the time and fees dedicated to administering so many options, many of which appear to be very similar, be better directed elsewhere? In particular, might members be better off with a smaller number of options delivering appropriate risk/return outcomes and a reduction in both fees and fund administration costs? I suspect, in many instances, the answer to both questions is yes…

These are excellent points made by APRA.

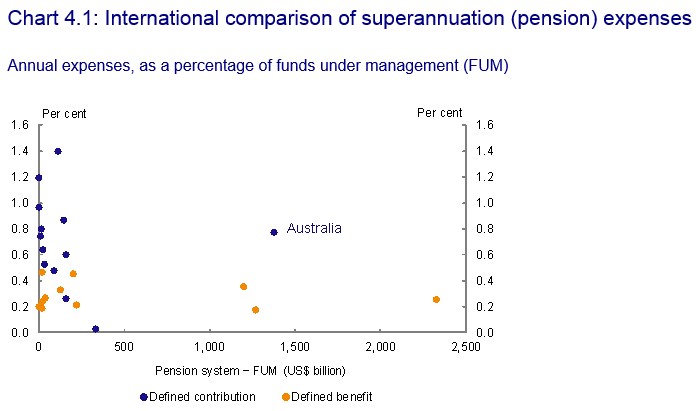

In 2014, the Murray Financial System Inquiry showed that the operating costs of Australia’s superannuation funds are among the highest in the world:

Advertisement

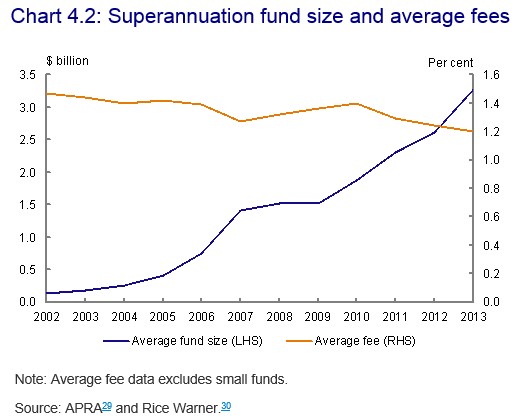

And that fees had not fallen in line with what could have been expected given the substantial increase in scale, which will dramatically reduce consumer’s retirement nest eggs:

The Grattan Institute’s Super Savings report also argued that excessive fees are reducing retirement nest eggs by some $40,000, and called for the Government to reduce fees by running a tender to select superannuation funds to manage the accounts of the nine million Australians who choose a default fund through their employer:

Advertisement

Running a tender to select these funds would save $1 billion a year in fees, or $40,000 for each account holder…

“There are too many accounts, too many funds, and too many of them incur high costs,” says Grattan’s Productivity Growth Program Director, Jim Minifie.

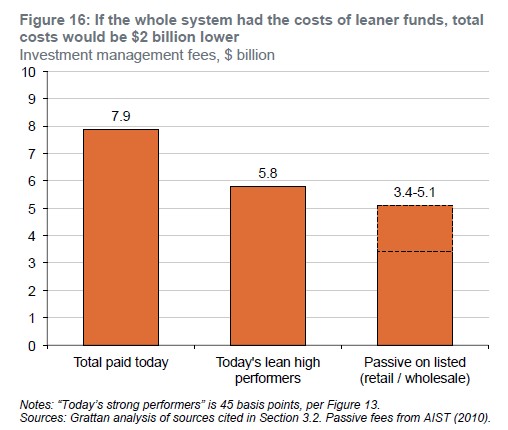

“Australia has many high-performing but lean funds. If other funds charged what they charge, account holders could get the same performance, but pay $4 billion a year less in administration and $2 billion less in investment management,” he says.

The Productivity Commission (PC) has also suggested limiting the number choices of default funds that would be offered to consumers from 110 to between four and 10, depending on how the system was devised.

Whereas Nicholas Barr, the professor of public economics at the London School of Economics, recently rebuffed the industry’s call for greater competition, claiming that allowing more competition would merely increase complexity in the superannuation system.

Advertisement

I’m with APRA. When it comes to superannuation, less (choice) is more.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.