The strong growth of investor borrowing for property in recent years has potential implications for financial and macroeconomic stability. The characteristics and risk profile of households’ investment property exposures differ in important ways from those of owner-occupiers…

Because interest expenses on investment properties are tax deductible, investors have less incentive than owner-occupiers to pay down their debt. Many take out interest-only loans so that their debt does not decline over time…

Investors could amplify cycles in borrowing and housing prices contributing to economic risks. Investors might be more likely to sell their property if they expect prices to fall because it is an investment rather than their home…

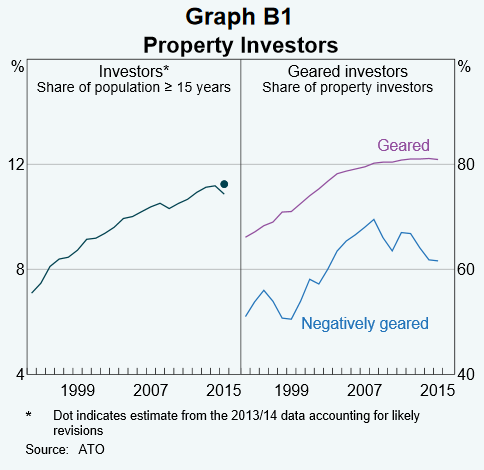

The share of taxpayers who are property investors has increased steadily over the past few decades (Graph B1). In 2014/15, 11 per cent of the adult population, or just over 2 million people, had one or more investment properties…

With many not earning positive income from their property, prospective capital gains are more likely the primary rationale for investing…

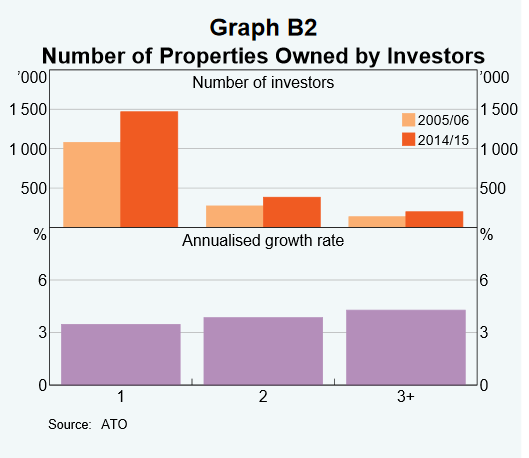

Around 70 per cent of investors own just one property. However, around half of investment properties are owned by investors with multiple properties; 20 per cent of investors own two properties and 10 per cent own three or more. The number of investors with multiple properties has grown relative to those with a single property, particularly between 2013/14 and 2014/15 (Graph B2).. investors with multiple properties have likely contributed to higher risk…

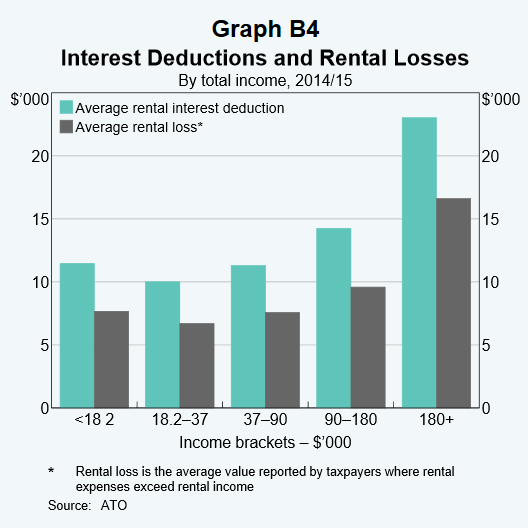

The absolute size of rental loss is largest for higher-income taxpayers (Graph B4).

Relative to total income, however, the rental loss is largest for the lowest income bracket and gets progressively smaller for higher income brackets. This suggests that lower-income taxpayers may be more vulnerable to increases in debt repayment obligations or reductions in income. They might also be more reliant on rental income to meet their repayments. About 35 per cent of individuals in the lowest income bracket are over the age of 60 and the majority of this income group did not have any salary income…

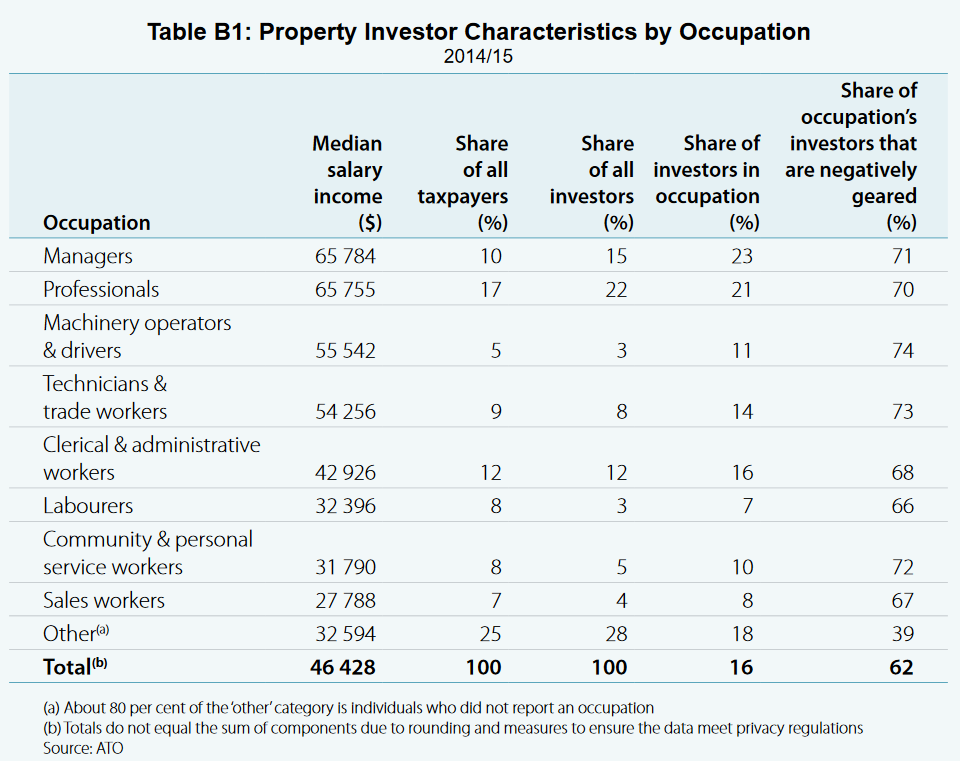

Professionals, for example teachers, lawyers and doctors, account for the largest share of property investors, reflecting their large share as taxpayers and their greater propensity to be investors…

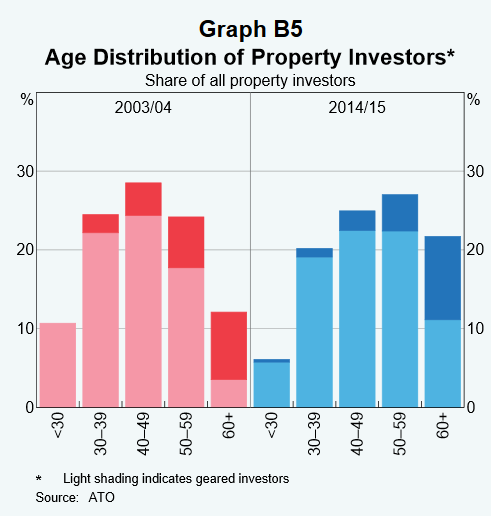

There has been a marked increase in the age of property investors since the mid 2000s. Over the decade to 2014/15, the share of property investors who were aged 60 years and over almost doubled (Graph B5)… There has also been a significant increase in the share of geared investors aged over 60…

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.