Some folks just won’t take yes for an answer:

Today’s Q3 CPI print delivered a downside surprise, with underlying inflation still below the RBA’s 2-3% target band

The key measures of underlying inflation showed it running at 1.85% y-o-y (the market had expected 2.0% y-o-y)

We still expect a tightening labour market will mean that hikes are coming in 2018 but now expect Q2 (previously Q1)

Still on the path, but inflation might take a little longer

Today’s Q3 inflation print surprised the market, the RBA, and HSBC, on the downside. The key underlying measures of inflation – the trimmed mean and weighted median – were both below the bottom edge of the RBA’s 2-3% target band in both q-o-q and y-o-y terms. The average of the two preferred measures of underlying inflation was 0.35% q-o-q and 1.85% y-o-y. The market had been expecting 2.0%, we had pencilled in 2.1%, and the RBA had been forecasting a slight rise in the y-o-y rate for the trimmed mean in its August official statement.

However, a deeper dive into the details still suggests that domestic inflationary pressures are gradually rising. The main measure of domestic inflation (nontradables) showed a further lift in the quarter. The weakness in the quarter was mostly in tradables inflation, with food prices surprising to the downside. Nontradables inflation was supported by rising housing costs, including for electricity.

Growth is also expected to pick up pace from here, supported by a lift in global growth, the end of the mining investment decline, a significant rise in infrastructure investment, and ongoing growth in exports. The expected pick-up in growth is already showing through in surveyed business conditions, which are at their highest level in a decade, and a tightening labour market. Employment growth has picked up strongly and businesses are starting to report that it is getting harder to find ‘suitable labour’. We expect this to put some upward pressure on wages growth in coming quarters.

Nonetheless, the RBA is expected to need clearer evidence that inflation is lifting before it is likely to start to lift its cash rate. With this in mind, we are pushing back our call on the RBA hiking cycle. We have held the view since December 2016 (see The RBA Observer: Game Changer: Commodities and Trump, 2 December 2016) that the RBA would start to lift its cash rate in Q1 2018. We still expect the cash rate to rise in 2018 but now expect that it may take a little longer for the RBA to get started. We now expect the first cash rate hike to be in Q2 2018 (previously Q1 2018). We still expect the cash rate to be 2.00% by the end of 2018.

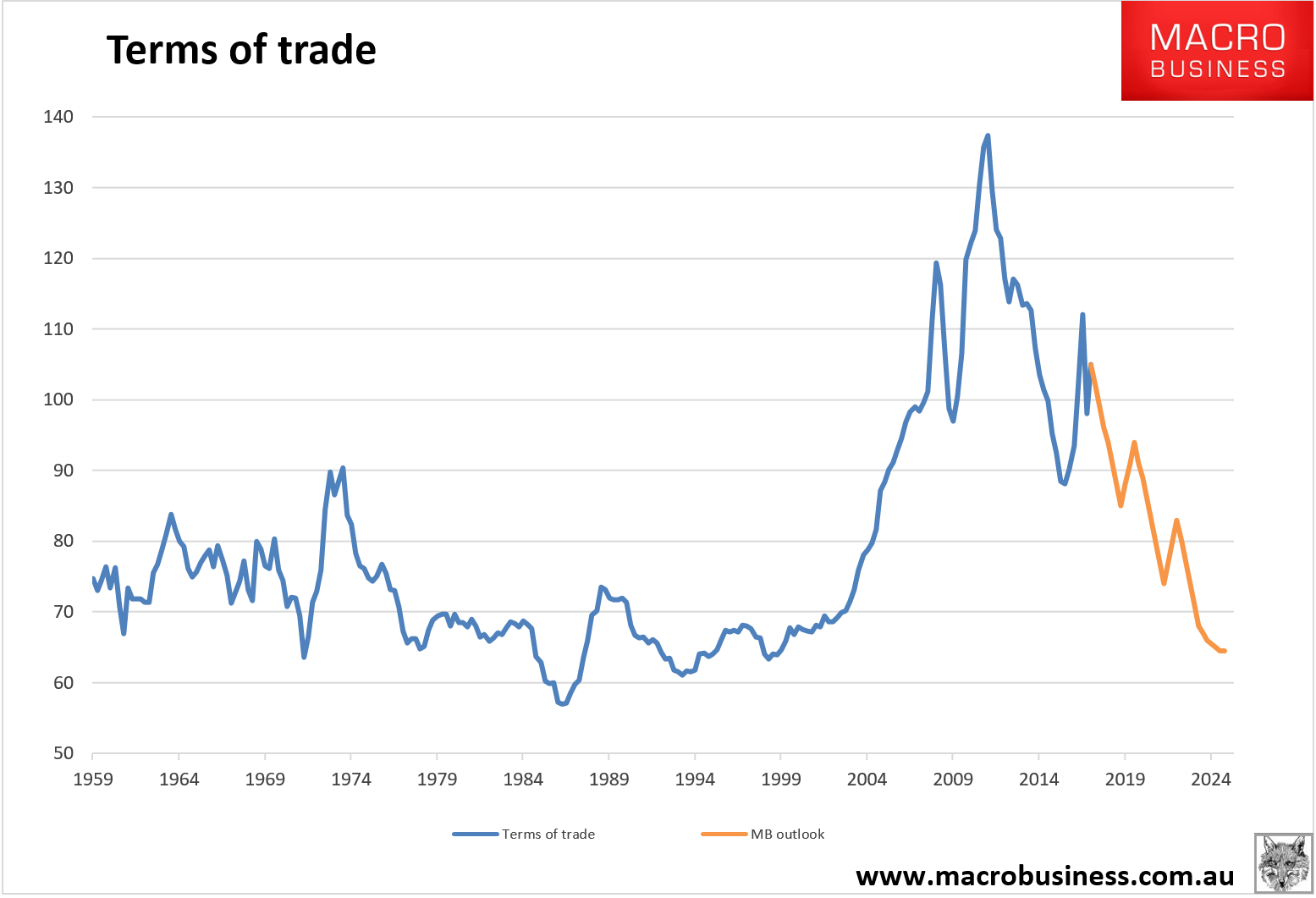

We are so not on the path. Australia’s future is deflation followed by more deflation as the historic terms of trade unwind marches on and on and on: