The Parliamentary Budget Office (PBO) has released a new report claiming that middle-income earners will bear the burden of bracket creep (aka ‘fiscal drag’) as wage rises push 1.8 million Australians into higher tax brackets:

The PBO’s 2017–18 Budget medium-term projections report identified that the projected return to surplus in 2020–21 is predominantly due to a projected increase in personal income tax revenue.

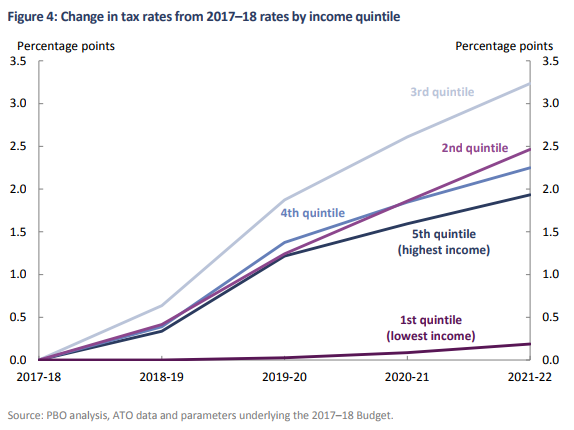

The average tax rate faced by individuals is estimated to increase by 2.3 percentage points over the period from 2017–18 to 2021–22…

The average tax rate for individuals in every income quintile is projected to increase over the period from 2017–18 to 2021–22. The largest increase is expected to be faced by individuals in the middle income quintile, whose taxable income is expected to average $46,000 in 2017–18. This group of taxpayers is projected to face an increase in their average tax rate of 3.2 percentage points by 2021–22, as a higher proportion of their income is taxed at the 32.5 per cent rate. Their average tax rate is expected to increase from 14.9 per cent to 18.2 per cent.

Increases in the average tax rate of between 1.9 and 2.5 percentage points are projected for individuals in the second, fourth and fifth quintiles. The average tax rate for individuals in the lowest quintile is projected to rise by only 0.2 percentage points because most of their income remains below the effective tax free threshold.

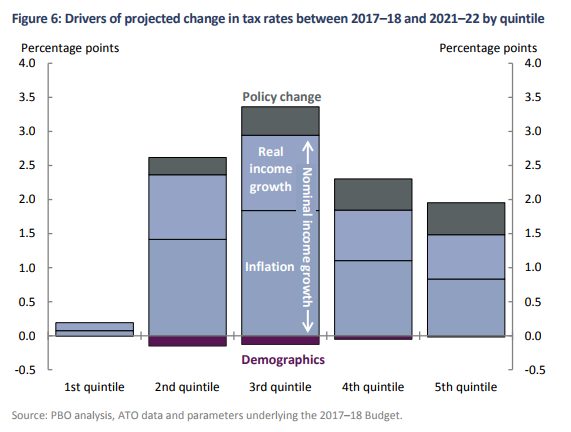

Across all quintiles, the largest driver of the increase in average tax rates is expected increases in nominal incomes. This reflects the impact of bracket creep, on account of both inflation and real income growth. In addition to the effect of nominal income growth, average tax rates are projected to increase due to policy changes, most notably the policy decision to increase the Medicare Levy from 2019–20.

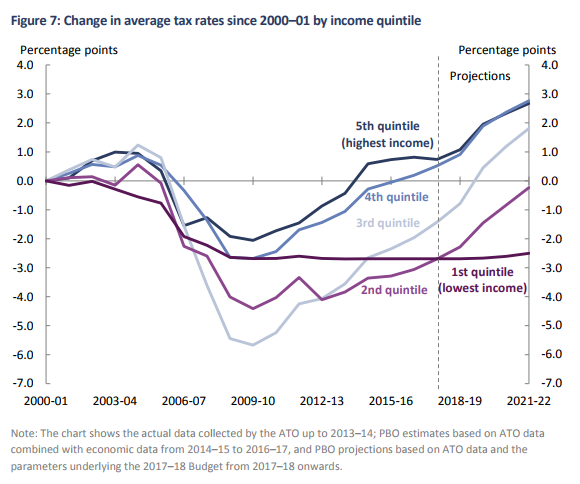

Taking a longer term perspective illustrates the net effect of nominal income growth and changes to tax policy on average tax rates over the period since 2000–01. This shows that for all but the lowest quintile, the increases in average tax rates since 2009–10 are offsetting reductions in average tax rates that occurred during the 2000s. By 2021–22, the average tax rate for individuals in the lowest two quintiles is still expected to be below its average in 2000–01, while the most significant increases will have occurred for individuals in the top two income quintiles.

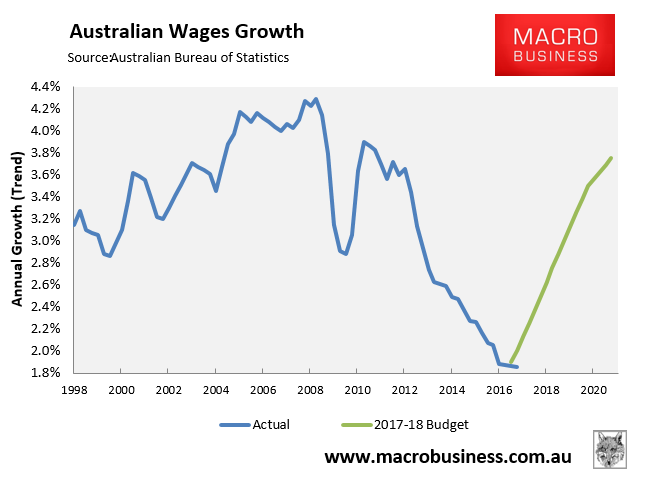

The PBO’s projections around income tax do appear inflated given they incorporate the Federal Budget’s wildly optimistic assumptions of a pending wages boom:

Advertisement

In the face of ongoing mass immigration, along with automation and other factors, wages growth is more likely to limp along at a low level, which necessarily means that the climb up tax brackets will occur much more slowly.

Nevertheless, over the long-run, bracket creep is a nasty phenomenon, particularly for lower-to-middle income earners. This is because low-to-middle income earners’ average tax rates are increased far more by bracket creep than for higher income earners.

Sadly, most of the political discussion around tax reform centers on those at the higher end of the income distribution, rather than those at the lower-to-middle end, where the impacts of bracket creep are worst and incentives to work are most distorted.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.