by Chris Becker

Action in Asia today was focused around the Chinese manufacturing PMI and the BOJ monthly outlook, with the latter unchanged but still mindful of its inability to create any inflation. The PMI slipped a little, weighing on Chinese stocks on the mainland and elsewhere, while tonights markets maybe watching the political newscapes as Mueller’s grand jury indictments against the Trump administration continue. Oh, let it continue!

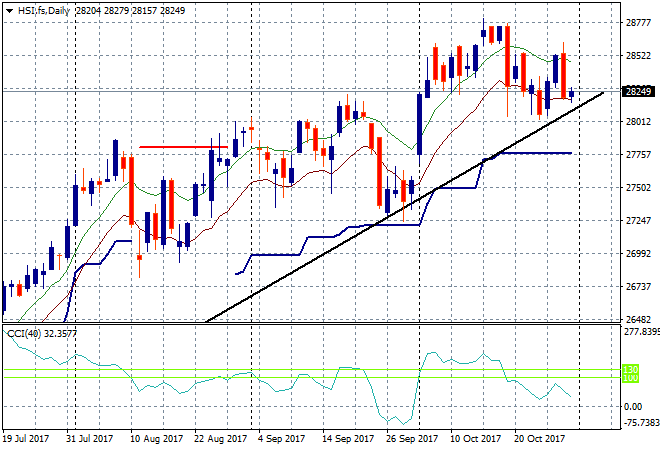

In mainland China the Shanghai Composite remains below previous resistance at 3400 points, still hovering at 3386 points. The Hong Kong based Hang Seng Index is slightly worse off, down 0.2% to 28282 points as it continues a reversion to mean dip against the long held uptrend on the daily chart:

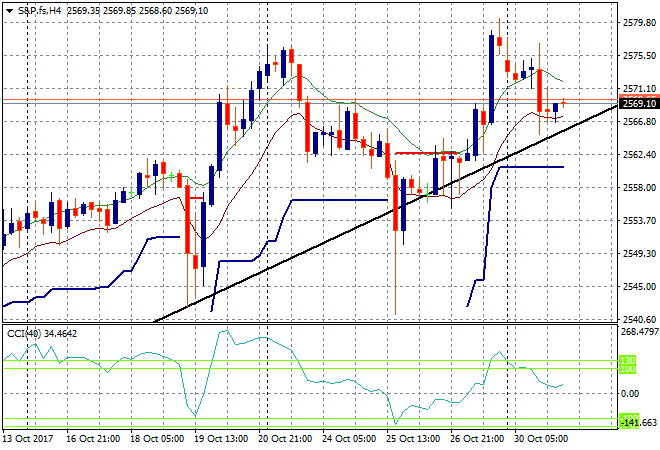

S&P futures are steady after last nights volatile session that saw small caps drag down the wider bourse with the earnings season to roll on tonight:

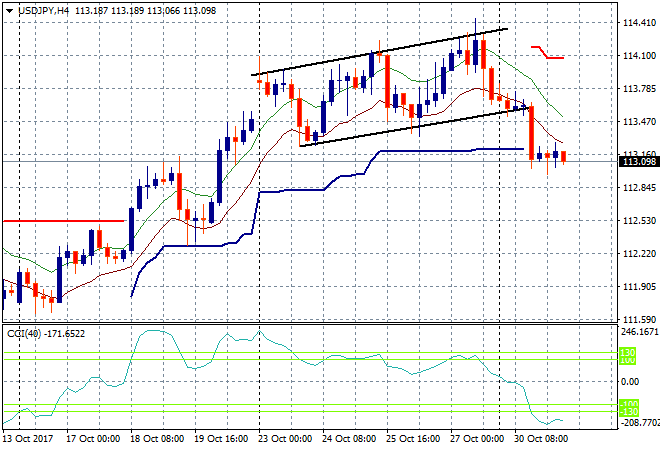

Japanese stocks have again put in a scratch session, with the Nikkei closing down only a few points lower to be at 21990 points even as Yen appreciated strongly overnight. The USDJPY pair was steady hovering just above the 113 handle during the Asian session, but has started to falter in the last hour or so, so we could see a capitulation later tonight as traders weigh up Governor Kurodas comments today:

The ASX200 had a good start today, going against the tide to rally after the open, but gave up after the Chinese manufacturing PMI was released and gave back all the gains, plus a little more, to finish 0.2% lower at 5909 points.

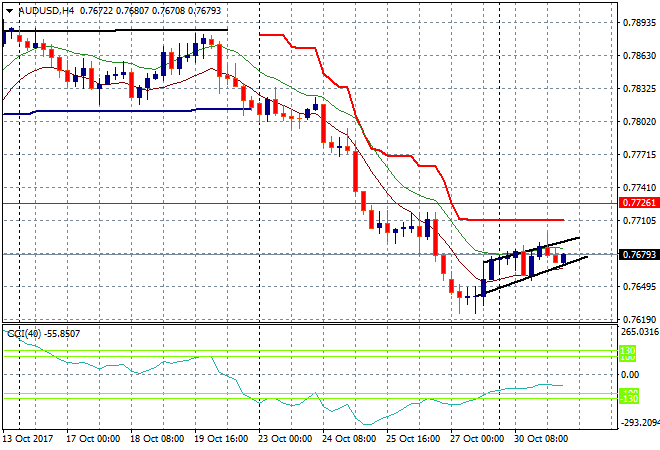

The Aussie dollar is still trying to find a bottom here after the small bounce on Friday night and did not react negatively to either the PMI or the BOJ outlook. Its currently right where it started the morning at 76.75 or so and is again looking weak going into the City open:

The data calendar continues tonight with quite a few important releases. Starting in Europe its the one-two punch of 3Q GDP and then October’s CPI print. In the US its the October consumer confidence numbers, plus house price data (but I repeat myself). In the wee hours of the morning we also have NZ unemployment numbers.