by Chris Becker

Not the greatest start to the week here in Asia with most stock markets in the red as Chinese bond markets roil under the continued pressure from Chinese authorities on reducing leverage. Big banks are reporting at the same time in China, with commodities also under pressure while traders await big heavyhitters in US stock earnings report overnight amid continued speculation about the new Federal Reserve chair.

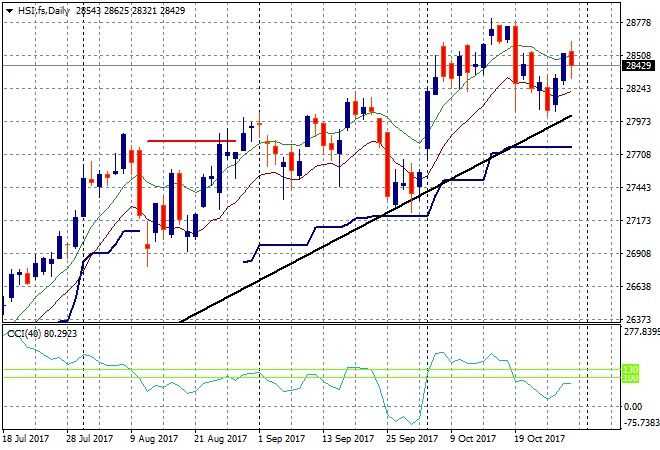

In mainland China the Shanghai Composite is back below previous resistance at 3400 points, down nearly 1% lower to 3390. The Hong Kong based Hang Seng Index is steadier, putting in a scratch session, up a few points to 28446 points as it reverts to mean against the long held uptrend on the daily chart:

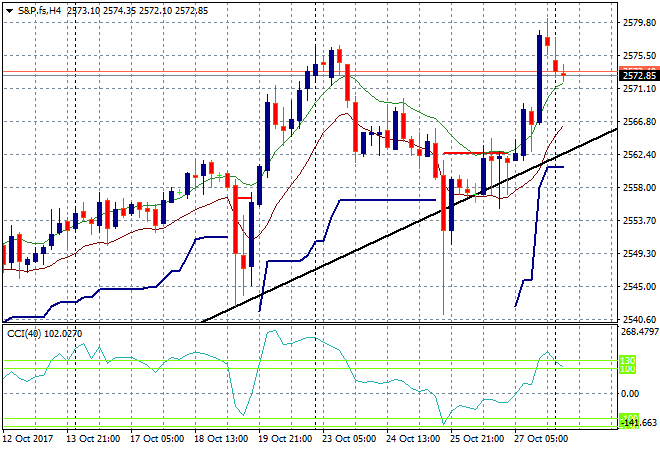

S&P futures are down slightly as earnings season rolls on, unable to double down on the gains from Friday night:

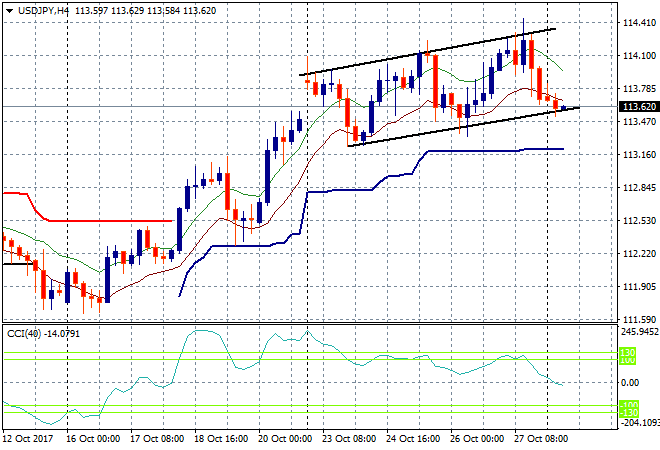

Japanese stocks have basically put in a scratch session, with the Nikkei closing down only a few points lower to be at 21988 points. The USDJPY pair gapped down on the Monday morning open as Yen strengthens, with price hovering on the lower end of the uptrend channel on the four hourly chart:

The ASX200 was basically the best performer in the region, closing 0.3% higher to 5919 points in a basically steady session from the open to the close. The major banks were mixed, as were the iron ore producers with no clear trend for the day.

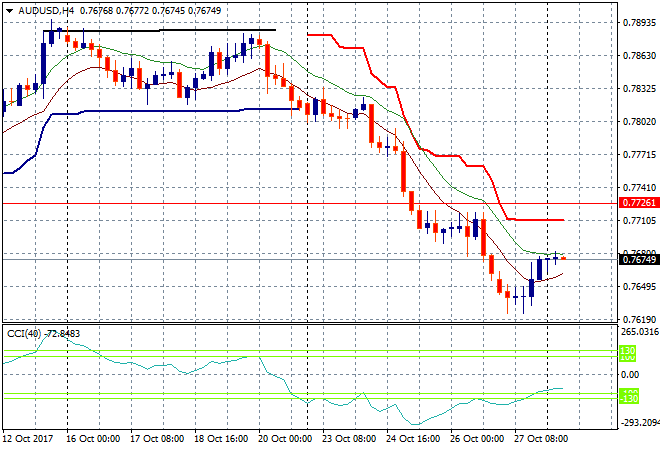

The Aussie dollar is trying to find a bottom here after the small bounce on Friday night after its very bad performance from last week which saw it fall nearly 200 pips. Its currently right where it started the morning at 76.75 or so and is looking weak going into the City open:

The data calendar starts the week with two major releases tonight, with German October CPI and US personal consumption expenditure (PCE).