by Chris Becker

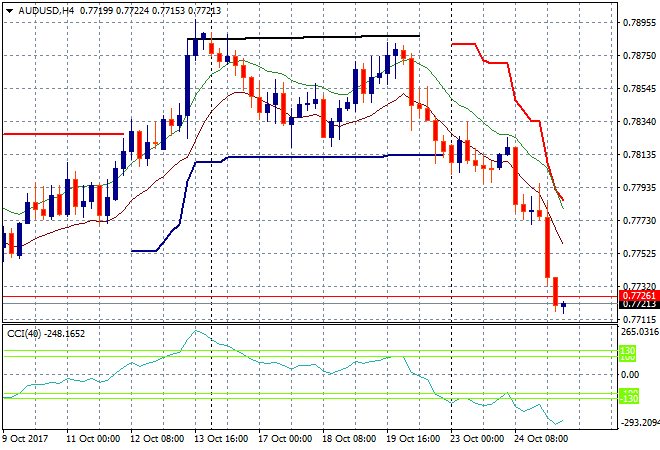

Japanese stocks finally caved in today as Yen slipped only slightly against USD. The real casualty in the currency wars was the Pacific Peso which fell abruptly on an “unexpected” poor CPI print, sending the Aussie dollar plummeting almost to 77 cents against the USD.

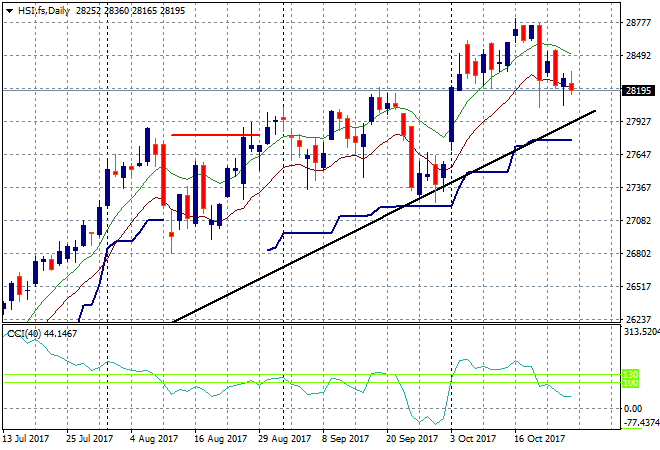

In mainland China the Shanghai Composite has lifted slightly, up 8 points or nearly 0.25% to almost close at 3400, a key resistance level that has been doggedly stubborn for awhile and closely watched by all! The Hong Kong based Hang Seng Index is up 0.4% to claw back some of its previous losses, currently at 28268 points but the short term downtrend has not yet finished here:

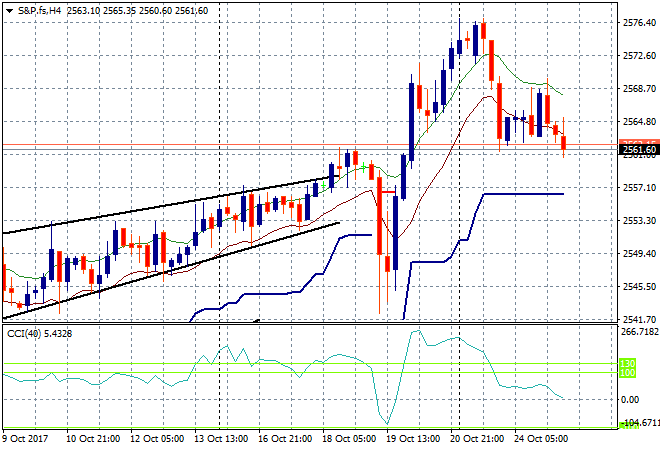

S&P futures are off slightly, indicating a poor start as earnings season rolls on and durable goods orders on the radar:

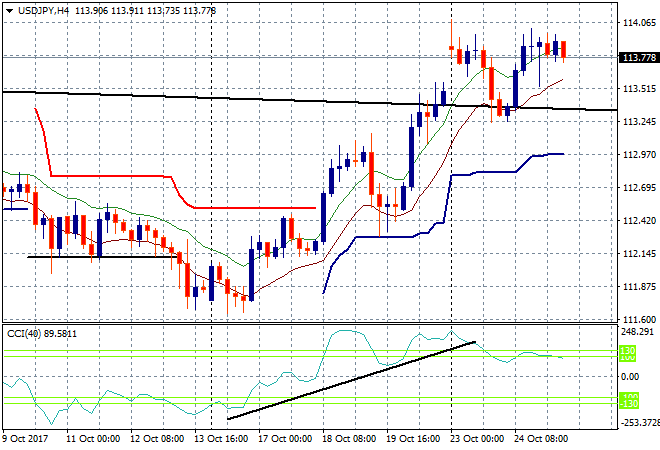

Japanese stocks finally put in a red session, with the Nikkei closing down 0.4% lower to be at 21707 points. This is probably not the first selloff as the overbought momentum readings remain in huge blowoff territory. The USDJPY pair is stubborn here, sitting right on key resistance below the 114 handle, still not above the July high:

The ASX200 put in another weak session, finishing just 8 points higher to be just above 5900 points. Last week’s breakout is not yet following through as today’s CPI print took the confidence out of the banks and other financials.

The Aussie dollar is having a doozy of a day, stalling and then plummeting on the CPI print to be just above the 77 handle against the USD going into the City open. This is a key level to watch and good see a big unwind of unwise long positions:

The data calendar continues tonight with three important releases to watch out for, first being UK 3Q GDP, then US durable goods orders and finally the Canadian central bank interest rate decision. We also get an oil rig count which might enlighten the bulls under the crude contracts.