Fairfax’s Jessica Irvine has done a good job debunking the Turnbull Government’s company tax cut agenda:

…with so many other nations engaged in a race to the bottom on corporate tax rates, can Australia afford to leave its 30 per cent rate where it is?

The first point to remember is that Australia’s company tax system is unique in the world in that domestic shareholders are actually rebated for every cent in company tax paid, so-called “franking credits”. So while our 30 per cent headline rate looks high, it is less of a burden than global comparisons of headline rates imply.

To the extent that foreign business people decide to move to Australia, naturalise and set up businesses here and issue shares to domestic investors, they too will benefit from the franking credits on offer here.

But it’s true that foreign owners of businesses who operate in Australia get no such credits, and so – based on a simple tax arbitrage analysis – face an increasing disincentive to invest in Australia relative to elsewhere…

All taxes are a discouragement to economic activity that would otherwise occur, and it’s true that, in a world of more mobile capital, a higher company tax rate may prompt some businesses to choose to invest elsewhere.

But other considerations influence investment decisions, particularly ones made with a long time frame in mind…

In a recent essay for the Lowy Institute, former Reserve Bank deputy governor Stephen Grenville weighed in on the corporate tax issue, arguing cutting Australia’s headline rate would have only a “minuscule” impact on foreign investment here.

Grenville points out that many foreign companies have demonstrated themselves more than willing to invest in Australia, attracted by our relatively concentrated markets with few suppliers and large “super profits” on offer. Think of the foreign retail invasion of Aldi, Costco and Zara, to name just a few.

And if global investors did suddenly prefer to invest in the US over Australia, this would push up the value of the US currency and reduce the value of ours – acting as a countervailing force and making it even cheaper to invest here, Grenville observes.

And given that foreign companies have proved so successful at avoiding paying tax here, anyway, Grenville sees little reason to give them a further discount…

The real problem with Australia’s company tax rate is that it is already substantially lower than our top personal income tax rates, creating an opportunity for tax minimisation for high-tax-bracket individuals who can create a company or trust structure to delay paying tax on their income, and thus benefiting from the time value of money.

“Perhaps some of those lobbying for lower company tax rates are the beneficiaries of such schemes,” Grenville muses…

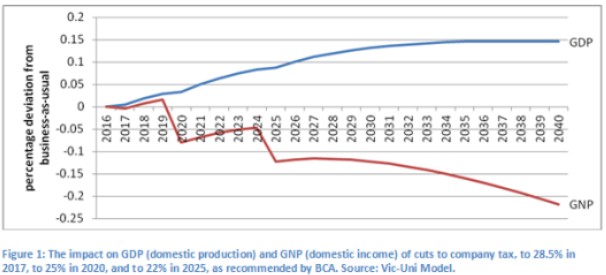

That’s a good summary of the key issues by Irvine. Although I would also have pointed out that the Treasury’s own modelling of the company tax cut showed almost zero impact on either jobs or growth, whereas modelling from Victoria University senior research fellow, Janine Dixon, found that cutting the company tax rate would actually lower national income (GNP) and living standards because of the benefits flowing offshore:

The Grattan Institute has also pointed out that if companies pay less tax, then some could reinvest some of what they save. But in practice, most profits are paid out to shareholders. So the tax cut won’t have much of an impact on domestic investment or jobs.

There is also the inconvenient truth that 76 of Australia’s biggest companies paid an average effective tax rate of just 16.2% in 2013 and 2014 – roughly half the corporate tax rate – costing the federal government $5.4 billion in potential tax revenue.

Ultimately, there is one threshold issue that needs to be overcome in deciding whether to cut Australia’s company tax rate to 25% from 30%:

Would cutting company taxes generate enough investment, jobs and growth to justify the estimated $8.2 billion cost to the Budget each and every year, and are there better uses of scarce taxpayer money?

Given the modelling surrounding the tax cut is at best unflattering, it shouldn’t be hard to find better alternative policy options to boost productivity, jobs and growth, such as:

- undertaking critical infrastructure investment and restoring Australia’s dilapidated infrastructure stock;

- boosting spending on education; and

- using direct measures to spur business investment, such as accelerated depreciation allowances, investment allowances, or some other measures.

Finally, as noted by Irvine, the proposed company tax cuts would disproportionately benefit the wealthy and worsen inequality, whereas the first two alternative policy options offered above would improve equity.

The bottom-line is that there is little justification for cutting company taxes beyond a blind faith in flawed ‘trickle-down’ economics. Such a policy would merely represent a financial windfall gift from Australian tax payers to foreign owned corporations and shareholders, robbing the Federal Budget of billions in tax revenue and lowering Australian living standards.

unconventionaleconomist@hotmail.com