By Martin North, cross-posted from the Digital Finance Analytics Blog:

Traditionally in the Australian context loans to property investors have tended to perform better than loans to owner occupiers. This is because investors receive rental income streams to help pay for the mortgage costs, they are willing to carry the costs of the property against future capital gains, and many will be able to offset costs against tax, especially when negatively geared. In addition, occupancy rates in most states have been stellar.

But things are changing, as the costs of borrowing for investment purposes have risen (thanks to the banks’ out of cycle rises), while rental returns are flat, or falling and costs of managing the property are rising. The supply of investment property is rising, and occupancy rates are declining in a number of key markets.

So today, we look at the latest gross and net rental yields by using our Core Market Model.

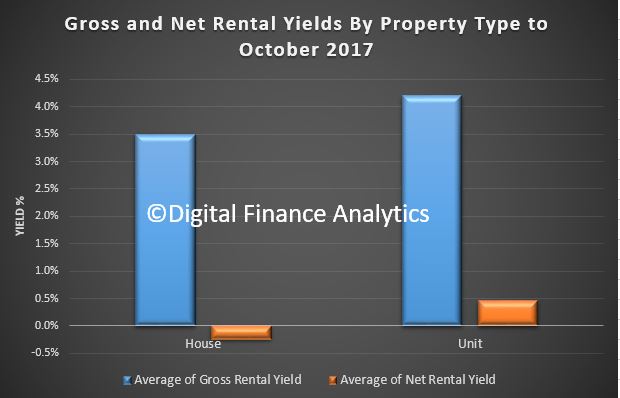

First, we look at yields by type of property. Gross yield is the rental streams received compared with the value of the property; before costs. Net yield is calculated by subtracting the costs of the property, including interest costs on mortgages, management costs and other ongoing maintenance costs. We calculate the net yield before any tax offsets.

Across the nation, units overall are providing a slightly better net return than houses.

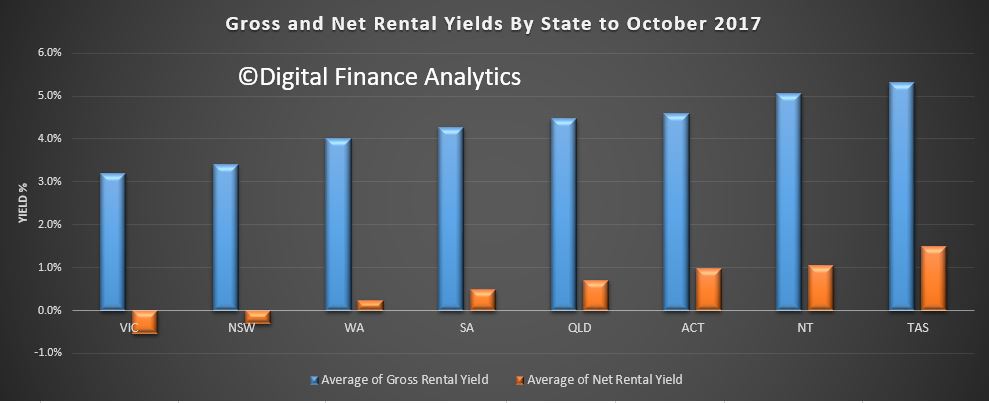

By state, VIC has the average worse net rental yield, followed by NSW, while TAS, NT and ACT have the highest net returns.

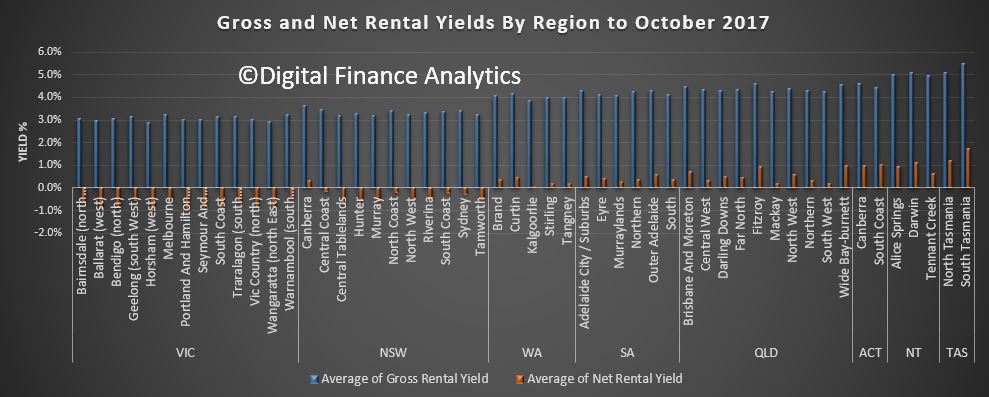

If we drill down into the regions in the states, we see some significant variations.

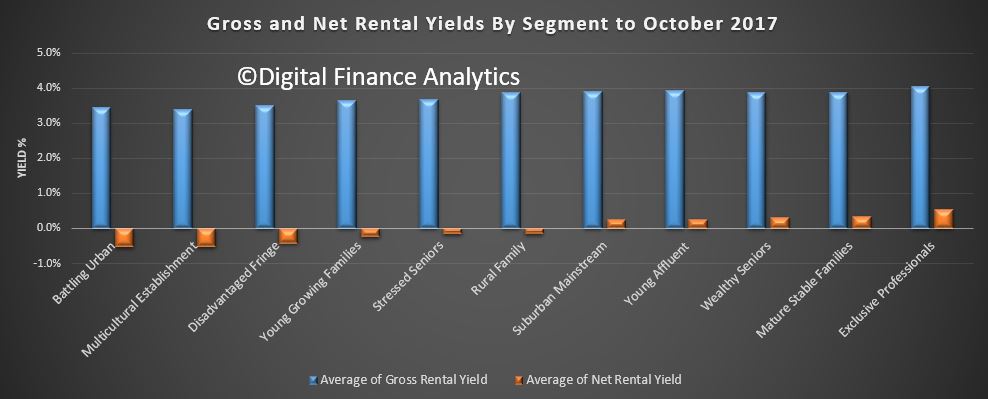

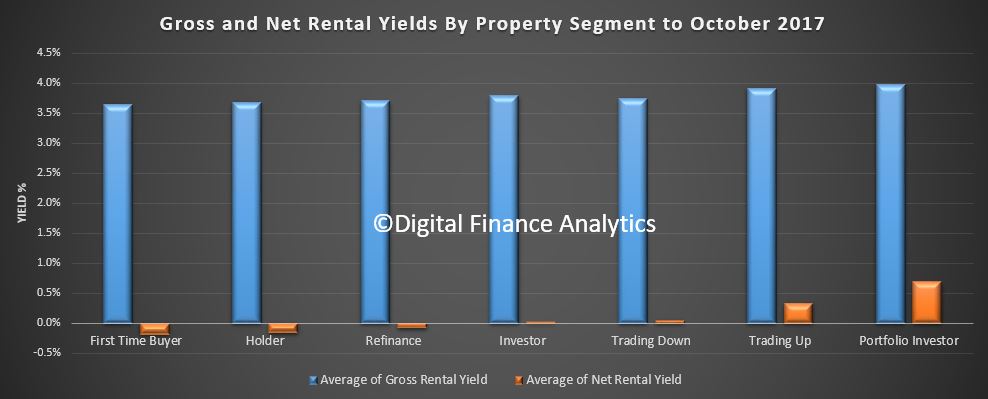

If we apply our core market segmentation, we find that more affluent households are getting better returns on average compared with the battlers and younger buyers. Perhaps experience counts.

We also see that Portfolio Investors, those with multiple properties, are on average getting better returns, whilst first time buyers are the least likely to get a positive net return. Again, experience seems to count.

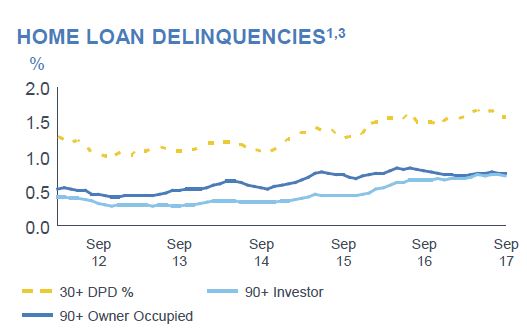

Finally, in the ANZ data today, released as part of their results pack was this slide. It shows a trend which we have been observing too, that is delinquencies are rising faster among property investors (to the point where the same ratio ~0.7% applies to both investors and owner occupiers).

More, concerning, our forward modelling suggests that investors are likely to become a significant higher risk as rates rise, rental returns stall, and occupancy rates fall. Just one more reason why we think the property investment party may be over.

Higher risks need to be factored into the banks’ modelling, especially as home price momentum is ebbing, so the value of these investment properties may start to fall.

By state, VIC has the average worse net rental yield, followed by NSW, while TAS, NT and ACT have the highest net returns.

If we drill down into the regions in the states, we see some significant variations.

If we apply our core market segmentation, we find that more affluent households are getting better returns on average compared with the battlers and younger buyers. Perhaps experience counts.

We also see that Portfolio Investors, those with multiple properties, are on average getting better returns, whilst first time buyers are the least likely to get a positive net return. Again, experience seems to count.

Finally, in the ANZ data today, released as part of their results pack was this slide. It shows a trend which we have been observing too, that is delinquencies are rising faster among property investors (to the point where the same ratio ~0.7% applies to both investors and owner occupiers).

More, concerning, our forward modelling suggests that investors are likely to become a significant higher risk as rates rise, rental returns stall, and occupancy rates fall. Just one more reason why we think the property investment party may be over.