By Gareth Aird, Senior Economist at CBA:

Key Points:

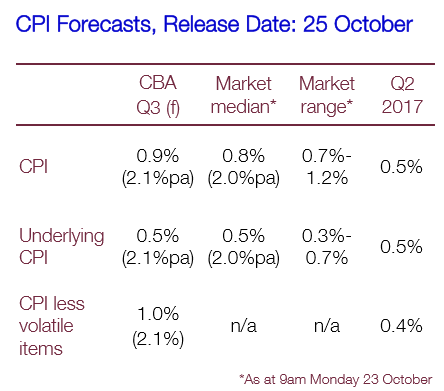

- We expect the headline CPI to rise by 0.9% in Q3 (2.1%pa), boosted by a large rise in electricity and gas prices.

- The underlying CPI on our forecasts will print at 0.5% (2.1%pa).

- Weak core inflation and little sign of inflation pressures building means monetary policy should remain on hold well into 2018.

Overview:

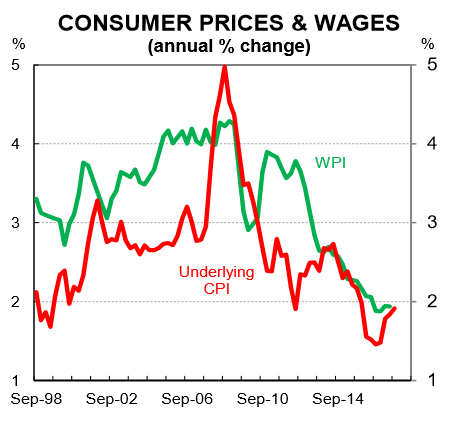

It’s fair to say that the inflation debate has very much centred on wages growth over the past year. The RBA has joined a raft of other central banks in commenting on the need for wages growth to lift in order to propel core inflation higher. The Australian labour market has tightened, but there is still plenty of spare capacity in it that is weighing on wages growth and inflation. We expect a gradual lift in wages and inflation over time. But not sufficiently so to bring a rate hike into the frame until well into 2018.

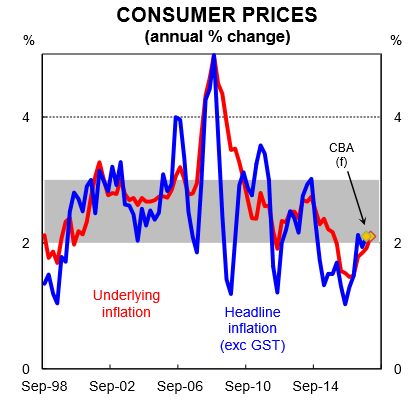

For Q3 2017, we expect the annual rate of both headline and core inflation to step up to within the RBA’s target band. The solid lift in headline inflation over the quarter will be driven by a lift in energy prices. Core inflation, meanwhile, is forecast to continue to lift by 0.5% which is broadly in line with wages growth.

Headline

We expect the headline CPI to rise by a sizeable 0.9% in the quarter after posting a small 0.2% lift in Q2. On our forecasts, the annual rate of inflation would step up to 2.1% from 1.9%. A solid 0.7% q/q increase in Q3 2016 will drop out of the annual calculations. On our forecast, real wages growth (i.e. the latest Wage Price Index deflated by CPI) will move into negative territory.

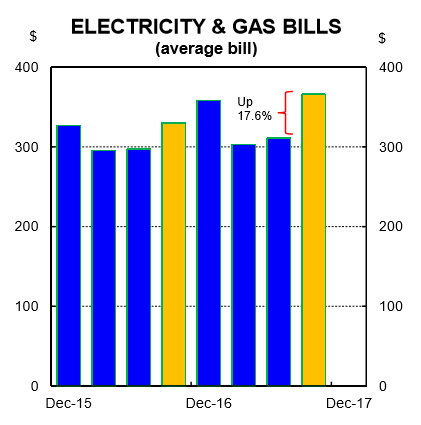

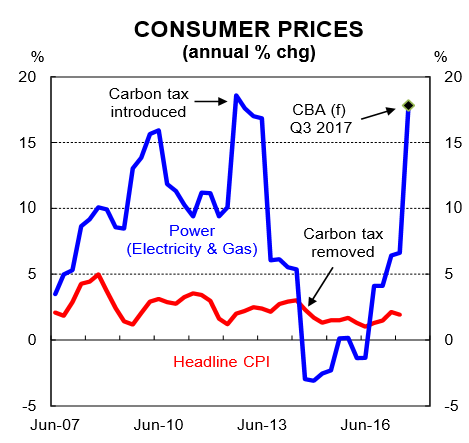

There will be a lot of focus on the utilities component of the CPI in Q3 because of the spike in energy prices. Analysis of household power bills paid by CBA customers using debit card and BPay leads us to believe that energy prices rose by 15% in Q3. Such an increase would contribute a whopping 0.51ppts to the quarterly growth rate.

Domestically generated inflation (i.e. non-tradables) is forecast to lift by 1.2%. Imported inflation (i.e. tradables) is anticipated to rise by 0.3%. Fuel prices will weigh on tradables inflation over Q3. In addition, a firmer AUD (4½% higher through the year on a TWI basis) has put downward pressure on import prices.

Underlying

The policy-relevant underlying measures of inflation should print a fair bit lower than the headline rate over Q3. We expect the average of the RBA’s preferred statistical measures to lift by 0.5% in Q3 which would push annual growth up to 2.1% – the same as the forecast headline rate.

On a six-month ended basis that smooths out quarterly volatility, some figuring shows:

- an underlying CPI of 0.4% or less would see the rate below 2.0%pa; and

- it would require a rise of 0.7% to take underlying inflation back to the middle of the target band.

The model

A top-down modelling approach to CPI forecasting shows only a modest contribution from unit labour costs, consistent with the weak wages backdrop. The inflation restraint from the output gap continues while the AUD is putting a dampener on import price growth through the year. These themes have been evident in the CPI over the past year.

The detail

The volatile items that can have a large influence on headline outcomes will be a net drag on CPI growth over Q3. Specifically,

- petrol prices fell by 2.4% over Q3 (after a 2.5% fall in Q2) and will subtract 0.07ppts to CPI growth; and

- fruit & veg prices fell at the wholesale level and are estimated to shave 0.07ppts from CPI growth. The unwind after the Cyclone Debbie price spike is complete.

As noted, the big spike in electricity prices explains most of the gap between headline and underlying inflation. Tobacco prices will continue to rise due to the effects of the excise increase. We are also expecting to see a decent lift in clothing and footwear prices. See table below for full details.

Seasonals

We expect seasonally large increases in property rates, urban transport fares and holiday travel & accommodation. Pharmaceuticals are expected to fall and seasonally low outcomes will be recorded in education.

We have the seasonally adjusted CPI rising by 0.6% so seasonal price moves should have a positive influence on headline inflation.

Risks

The NZ Q3 CPI of +0.5% q/q surprised a touch to the upside. And the tradables component, which has a reasonable correlation with Aus tradables (60%), lifted by 0.2% vs the RBNZ’s expectation of a decline of 0.5%. That said, our forecast for a 0.3% increase in AUS tradables factors in the NZ upside surprise. This means that we don’t think the risk lies with a higher Aus tradables print, particularly given the recent strength of the Aussie dollar.

Clearly, the key risk to the headline Q3 CPI is around electricity prices. Our forecast for a 15% rise in energy prices over the quarter probably sits on the ambitious side of the fence. As a result, we think that the risk lies with a surprise to the downside on utilities. And when combined with our tradables view means that the risks to our headline CPI call are to the downside. The weak retail numbers in July and August would be consistent with ongoing price discounting.

For the underlying CPI we think the risks are evenly balanced. This reflects the competing forces of the solid improvement in the labour market against continued weakness in wages growth.

Monetary policy implications

If Q3 CPI prints in line with our expectations then both headline and core inflation will move within the RBA’s target band. That alone, however, does not mean a rate hike is around the corner. Underlying wages growth (i.e. excluding the impact of the Fair Work Commission on the minimum wage) is expected to remain soft for some time. And there is still a fragility to households, as evidenced by the latest retail trade data. As such, we continue to expect the RBA to be on hold until late 2018.

A high-side CPI surprise would mean a risk that our late 2018 rate call would have to be brought forward. A downside surprise could see any move slip into 2019.