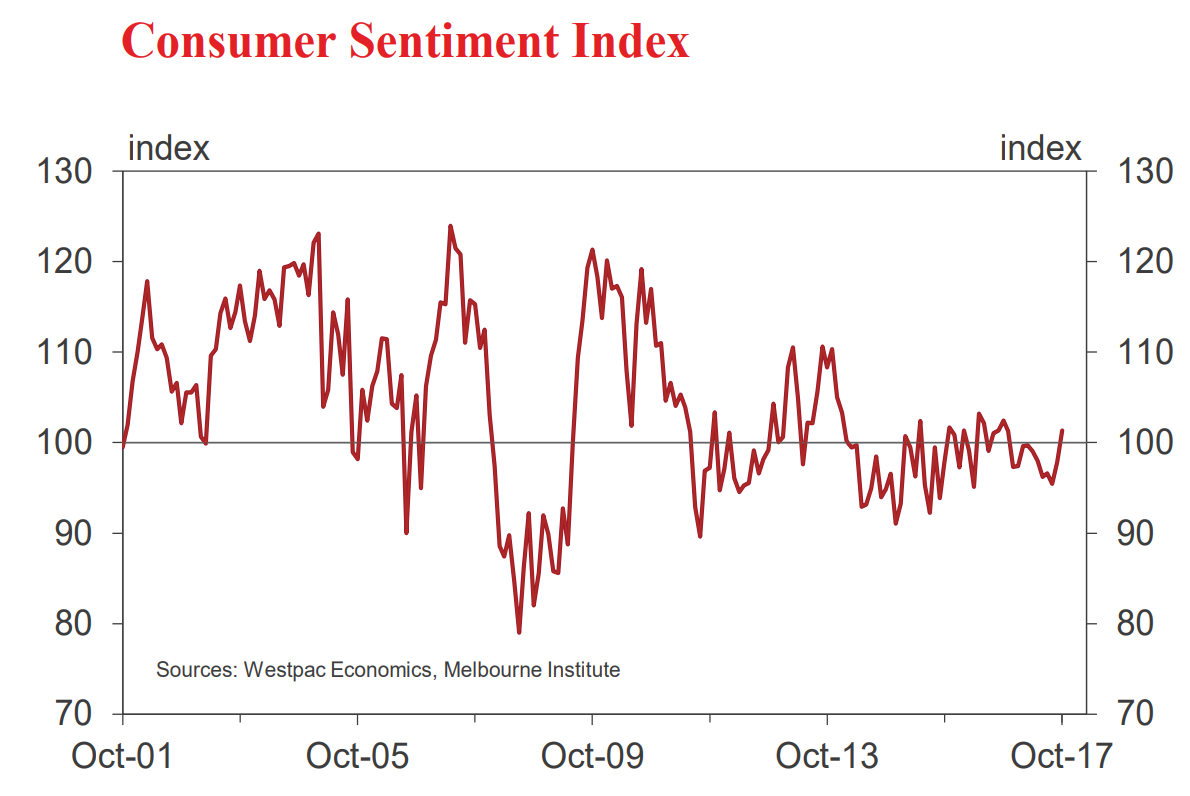

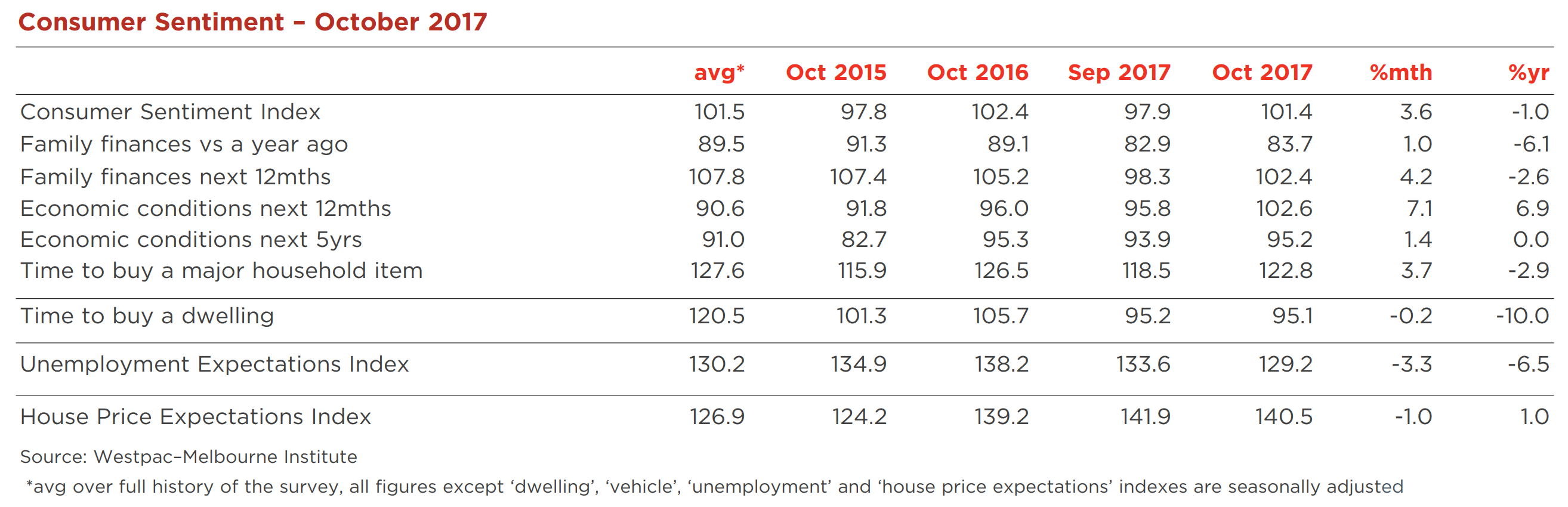

• The Westpac Melbourne Institute Index of Consumer Sentiment rose 3.6% to 101.4 in October from 97.9 in September.

This is the first time since November last year that optimists have outnumbered pessimists and represents the highest level of the Index since October last year.

Consistent reports of an improving global economy may have been a factor behind this lift in confidence. It is also likely that concerns about rising interest rates associated with overheated housing markets have eased.

Ongoing improvements in the labour market are also boosting confidence. Confidence showed stronger gains amongst those employed as tradies, ‘paraprofessionals’ (typically in the health and education sectors), or labourers. The rise in confidence was particularly strong for ‘trade’ workers, up 22% in the month, suggesting the continued strength in residential building was a positive factor.

However, confidence is still not particularly strong, with views on family finances a clear weak spot. Whereas the overall Index is down 1% on a year ago respondents’ assessments of their own finances relative to a year ago have fallen by 6.1% and the outlook for finances over the next 12 months is down by 2.6%. Offsetting that ongoing weakness in respondents’ assessments of their own finances is a lift in the 12 month economic outlook of 6.9% relative to last October.

All sub-indexes recorded a lift in October.

The ‘economic conditions, next 12 months’ sub-index posted the strongest gain, rising 7.1% to a four year high. Some of this likely stems from consistent coverage of the continuing improvement in the global economy with, in particular, improved confidence in the US growth outlook. Longer term economic prospects showed a more muted rise. The ‘economic outlook over the next 5years’ sub-index rose just 1.4%.

Consumers’ views on family finances also improved but the gains were more mixed with readings still weak overall. The sub-index tracking expectations for ‘finances over the next 12 months’ posted a solid 4.2% gain. An easing in concerns about potential interest rate rises was a likely factor. The ‘finances vs a year ago’ sub-index posted a more muted 1% rise.

Consumers were more positive about making major purchases, the ‘time to buy a major household item’ sub-index rose 3.5% in October after a 2.1% lift in September. However, the sub-index remains well below its long run average (down 2.9% over the year), suggesting that the sluggish spending evident through most of 2017 is likely to extend into year-end.

Expectations for the labour market continue to improve. The Westpac Melbourne Institute Unemployment Expectations Index fell 3.3% to 129.2 in October, marking the lowest reading since June 2011 (recall that lower reads mean more consumers expect unemployment to fall in the year ahead). 11 October 2017 The move is broadly based with expectations improving across all the major states.

Consumer views around housing remained downbeat. The ‘time to buy a dwelling’ index dipped 0.2% to 95.1, well below the long run average of 120. State indexes continue to vary widely, ranging from very weak reads in NSW (77) and Vic (88) to a strongly positive result in WA (135.4).

Consumer expectations for house prices also softened in the month. The Westpac Melbourne Institute Index of House Price Expectations dipped 1% to 140.5. The index still shows positive price expectations nationally although the state breakdown showed a sharp 8% decline in New South Wales (to the lowest level since June last year) partially offset by stronger price expectations in Queensland and Western Australia. Evidence that house price expectations in the overheated Sydney market are cooling is likely to be encouraging for policymakers.

The Reserve Bank Board next meets on November 7. The Board is certain to keep rates on hold. In fact Westpac does not expect rates to rise at all over the next year despite market pricing and general commentary.

The key to the interest rate outlook remains the consumer and the housing market. While today’s report shows a welcome boost in consumer confidence most of the strength is centred on the one year economic outlook. Respondents remain concerned about their own finances despite an expectation that the economy over all will improve. As we saw in the data for retail sales in August, consumer assessments of family finances, which have been downbeat for some time, are likely to be a more reliable indicator of actual spending than their views on the general economic outlook.

Furthermore, the survey continues to point to an easing in sentiment in the housing markets in the major states. Interest rate increases aimed at cooling over heated housing markets appear to be becoming unnecessary as macro prudential policy tools are achieving the same purpose.

Quite right, Bill. A little Botox Boom relief there. But do not be fooled. It will run out in 2018. And sentiment remains spectacularly weak if cyclically-adjusted.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.