The Turnbull Government and the Business Council of Australia (BCA) will today step-up their efforts to cut Australia’s corporate tax rate from 30% to 25% for all companies. From The AFR:

Big business will step up its campaign to extend corporate tax cuts to all businesses this week with a campaign to persuade non-Coalition politicians to stop Australia being left behind as one of the highest taxing developed countries…

“We are kidding ourselves if we think we can impose one of the highest tax rates in the developed world on Australian businesses and expect them to thrive, invest and create jobs,” BCA chief executive Jennifer Westacott said…

“As other countries have slashed their company tax rates to improve their competitiveness, Australia has been left to languish with a rate that has been unchanged for 16 years,” she said…

During a visit to the US last week, Mr Morrison cited Treasury estimates that cutting the corporate tax rate from 30 per cent to 25 per cent would generate a sustained lift in Australia’s GDP of just over 1 per cent.

He said cutting taxes would be important to boosting investment, productivity and wages.

“[Wages are] only going to change through greater investment and improved productivity,” he said.

The Treasury’s own modelling on the company tax cut package showed minimal benefits for either jobs or growth. As explained by The Australia Institute’s Richard Denniss:

According to Treasury’s in-house modelling, and the modelling it commissioned from Chris Murphy, if the company tax rate is lowered from 30 per cent to 25 per cent then gross domestic product will double by September 2038, while without the tax cut it won’t double until December 2038. Wow, a whole three months earlier. Both modelling exercises conclude that in 20 years’ time the unemployment rate will be 5 per cent regardless of whether we spend $50 billion on company tax cuts or not…

The “benefits” are more accurately described as rounding error than significant reform.

Advertisement

The Grattan Institute has also pointed out that if companies pay less tax then some could reinvest some of what they save. But in practice, most profits are paid out to shareholders. So the tax cut won’t have much of an impact on domestic investment or jobs.

And yet despite these minuscule benefits to jobs or growth, the full company tax cut package would cost the federal budget a small fortune in lost revenue.

Again, the modelling of the company tax cut package conducted by Independent Ec0nomics on behalf of the Australian Treasury estimated that the full company tax cut package would cost $11.3 billion per year. However, this would be reduced to $8.2 billion due to “a gain in personal income tax and superannuation income tax of $3.1 billion as the cut in company tax automatically reduces the value of franking credits”.

Advertisement

Obviously, the loss of revenue from company tax cuts would need to be made up somewhere, such as by raising personal income taxes, cutting government investment in infrastructure, or slashing welfare expenditure. Such cuts would necessarily reduce jobs and growth.

The fact of the matter is that Australia’s unique dividend imputation system strongly undermines the case for company tax cuts, since the lion’s share of the benefits from cutting company taxes would flow to foreign owners/shareholders, thus representing a direct fiscal transfer from Australian taxpayers to foreigners, and lowering national income in the process.

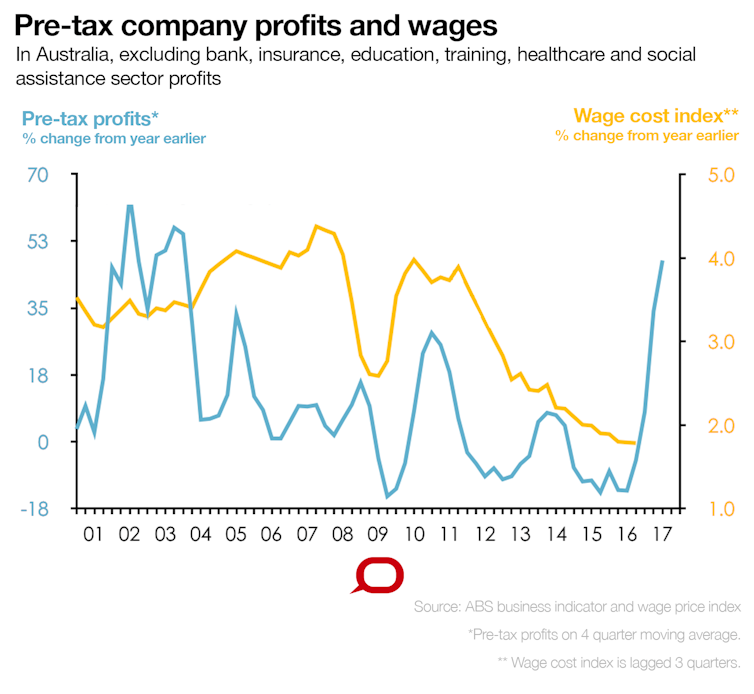

Scott Morrison’s claim that cutting company taxes would stimulate wages growth is also highly spurious. As noted by Saul Eslake last week, there is minimal link between company profits and wages growth:

Advertisement

…there is little data to support the idea that wages and profits are connected.

There does not appear to be any “leading” relationship between growth in pre-tax company profits and growth in wages, even if the mining sector (which accounts for a good deal of the fluctuations in profit growth over the past dozen years) is excluded.

Some relationship between profit margins (that is, profits as a proportion of sales revenue) and wages might have existed in the past. However, that appears to have broken down in the years since the peak of the commodities boom, in 2011-12, as you can see in the following chart.

Since then, aggregate profit margins have risen to levels not seen since the early 2000s, but wages growth has continued to slow.

Rather than being a precursor to faster growth in wages, the growth in Australian company profits in recent years appears to be part of a broader global pattern: the share of aggregate income accruing to capital is rising while that accruing to labour is falling.

…there’s absolutely no evidence that preferentially taxing small businesses will do anything to boost innovation, productivity, investment or employment. Hence, there’s no reason to think it will do anything to lift wages growth.

Nor is there any compelling empirical evidence to suggest that across-the-board tax cuts for larger companies will have any significant impact on employment and hence on wages.

Rather, an acceleration in wages growth is more likely to come from policies that directly boost economic and employment growth – such as increased spending on (well-chosen) infrastructure projects – and that boost productivity growth (including well-targeted education and training initiatives).

A more controversial proposition may be that measures designed to reverse, in part, the shifts in the shares of national income accruing to labour and capital over the past decade or so could also help accelerate wages growth.

Partly because real wages have grown more slowly than labour productivity since the turn of the century (as you can see in the previous chart), the “profits share” of Australian national income is well above its long-run average. The “wages share” is close to a record low…

So. while labour has been doing a good job, as evident by its strong productivity performance, its efforts are getting killed by dismal capital productivity as savings are massively mis-allocated into profitless houses, profitless energy and a profitless government that wouldn’t know a reform policy if it ran over it in a bus.

Advertisement

Therefore, the last thing that Australia should do is lower the company tax rate, which would unambiguously benefit the wealthy and worsen inequality.

Rather than this blind faith in flawed ‘trickle-down’ economics, Australia needs tax reforms that encourage capital to be once again deployed into productive investments.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.