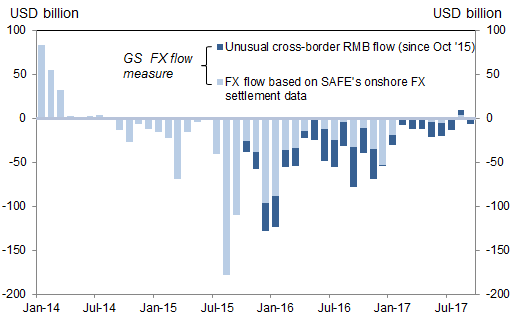

Our usual preferred gauge of underlying flows suggests a total net FX outflow of US$7bn in Sep (US$2.4bn from net FX demand onshore plus US$4.9bn in FX outflow routed through the CNH market).

According to the SAFE dataset on “onshore FX settlement”, net CNY demand by non-banks onshore in Sep was -US$2.4bn (vs. +US$3.1bn in Aug). This is composed of +$5.1bn net inflows via net outright spot transactions and net outflow of US$7.5bn via net freshly-entered forward transactions. In particular, demand for short-CNY forwards rose significantly (from US$10bn in Aug to US$28bn in Sep), following the cut of reserve requirement for sales of FX derivatives to zero in early Sep, which made it less costly for onshore entities to hedge against CNY.

Another SAFE dataset on “cross-border RMB flows” shows that net flow of RMB from offshore to onshore was -US$4.9bn in Sep (vs. +US$5.8bn in Aug).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.