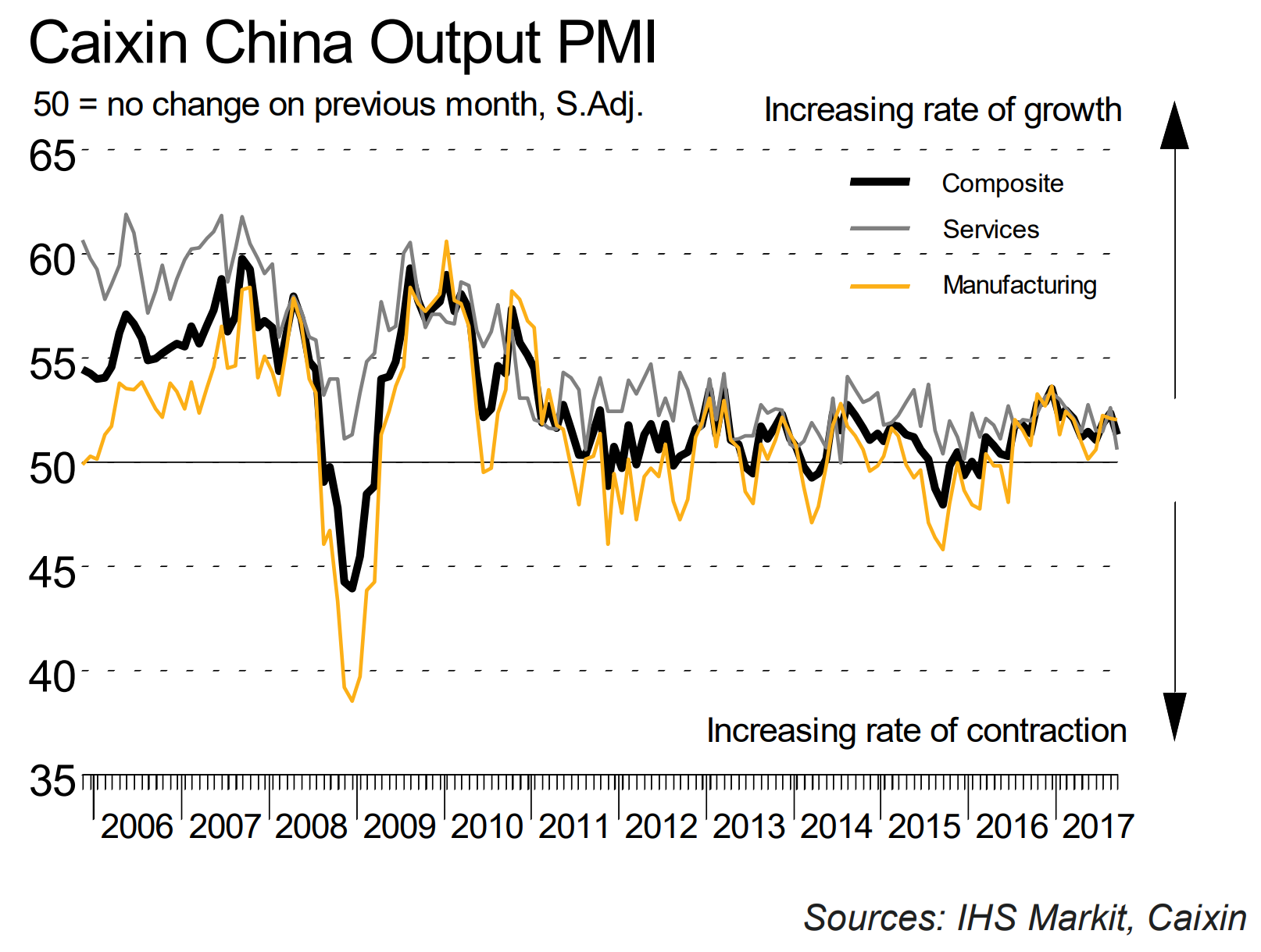

The Caixin China Composite PMI™ data (which covers both manufacturing and services) signalled a weaker expansion in total Chinese business activity at the end of the third quarter. Notably, the Composite Output Index fell from 52.4 in August to a three-month low of 51.4 in September.

The slowdown was driven by weaker increases in output at both manufacturing and services companies. A drop in the seasonally adjusted Caixin China General Services Business Activity Index from 52.7 to 50.6 in September pointed to only a marginal increase in services activity that was the slowest for 21 months. At the same time, growth in manufacturing production edged down to a three-month low.

Weaker expansions in activity coincided with a slowdown in new order growth across both monitored sectors. While manufacturers signalled the softest increase in new business for three months, service providers saw only a modest upturn in new order books. A number of companies mentioned that relatively subdued client demand had weighed on sales at the end of the third quarter. As a result, composite new work increased at the weakest pace since June.

In line with the trend for new orders, services companies increased their staffing levels at a slower rate in September. Furthermore, the latest expansion of payroll numbers was only marginal. At the same time, goods producers signalled a further decline in employment, though the rate of job shedding eased to a six-month low. Job creation across the service sector largely offset job cuts at manufacturers to leave overall employment little-changed for the second month in a row.

After a four-month sequence of accumulation, the level of outstanding work at Chinese services companies declined during September. That said, the rate of depletion was only slight. In contrast, backlogs of work continued to rise at manufacturers, though the rate of expansion was the weakest seen since April. At the composite level, the level of work-in-hand (but not yet completed) rose at the softest pace for a yearand-a-half.

Services companies signalled only a marginal increase in cost burdens at the end of the third quarter, despite the rate of inflation picking up for the second month in a row. This contrasted with a sharp and accelerated rise in manufacturers’ input costs. Notably, goods producers saw the steepest rise in input prices since last December, with many firms linking the increase to greater raw material costs. Consequently, the rate of composite input price inflation quickened to an eight-month high.

Reflective of the trend for input costs, output charges set by services companies rose only slightly during September. This contrasted with a marginal drop in prices during August, however. Meanwhile, stronger cost pressures at manufacturers led factory gate charges to increase sharply as firms sought to protect their margins. Moreover, the rate of inflation was the quickest recorded for nine months. Selling prices at the composite level subsequently increased at the fastest pace since last December.

Slower growth in output and new business dampened overall business confidence in September, with both manufacturers and service providers expressing a weaker degree of optimism compared to the previous month.

I expect this to get worse as the winter shutdown shock transpires then take off again Q1 before falling all next year.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.