Borat would blush at the Australian energy rogering

The gas cartel straight up lied to your face yesterday at the AFR:

Santos’ head of strategy Angus Jaffray told the summit that were it not for the LNG projects in Queensland, the gas market on the east coast would be tighter rather than looser.

Mr Jaffray said the domestic market couldn’t have supported the development of Queensland’s large coal seam gas resource because the market was too small and the cost of producing the gas is much higher than historic, cheaper fields, requiring higher prices to be economic.

“Without the LNG projects, most of the gas produced in Queensland today would still be in the ground and the tight supply scenario on the east coast would be much worse since we couldn’t simply lean on Queensland for their gas,” he says, rejecting suggestions the LNG exporters are the villain of the piece in the east coast gas shortage.

Mr Jaffray says the two main reasons for the shortage are the decline in supply from fields in Victoria’s Gippsland Basin and the lack of investment in new gas projects due to a lack of clear policy supporting the developments from governments that are often being influenced by scare-mongering activists.

If that were true then STO would not be buying half of its gas for export from third parties.

Shell lied too:

Shell Australia executive vice president Zoe Yujnovich is explaining two myths of the gas market: that all gas is exported starving the domestic market and that Australian gas can be bought cheaper overseas.

Ms Yujnovich says the “myth” that exported gas is cheaper than gas sold locally has been manufactured by detractors of the industry to erode trust around pricing and diminish public support for an export sector.

“Allow me to be absolutely clear on this point – Australian gas is never cheaper for manufacturers in Japan than it is for Australian factories,” she says.

“To suggest otherwise is a classic example of a disingenuous comparison, or shenanigan, designed to diminish public support for an export industry.”

Ms Yujnovich says that quoting the LNG export price ignores the huge volumes that the importing utilities buy and the costs for processing, storing and transporting gas that they pass on to their customers.

She also debunks the idea that the development of the LNG industry has resulted in shortages of gas for domestic customers, saying that Shell’s QGC business in Queensland has been able to increase local gas supply well beyond what it could have without the export market.

Yesterday Aussie LNG could be bought in Japan on contract for $10Gj. In Australia it cost anywhere up to $16Gj, down from $20Gj. Even with storage and transport you decide whether that’s cheaper.

Anyway, it’s really all besides the point. The first benchmark for sense to return to the market is export net-back prices – the Japan price minus the cost of shipping and liquifaction – which is about $8Gj.

But, in actuality, that should be the worst case outcome. We should be aiming to preserve our cheap energy advantage with much lower prices than export net-back. That’s what everyone else does.

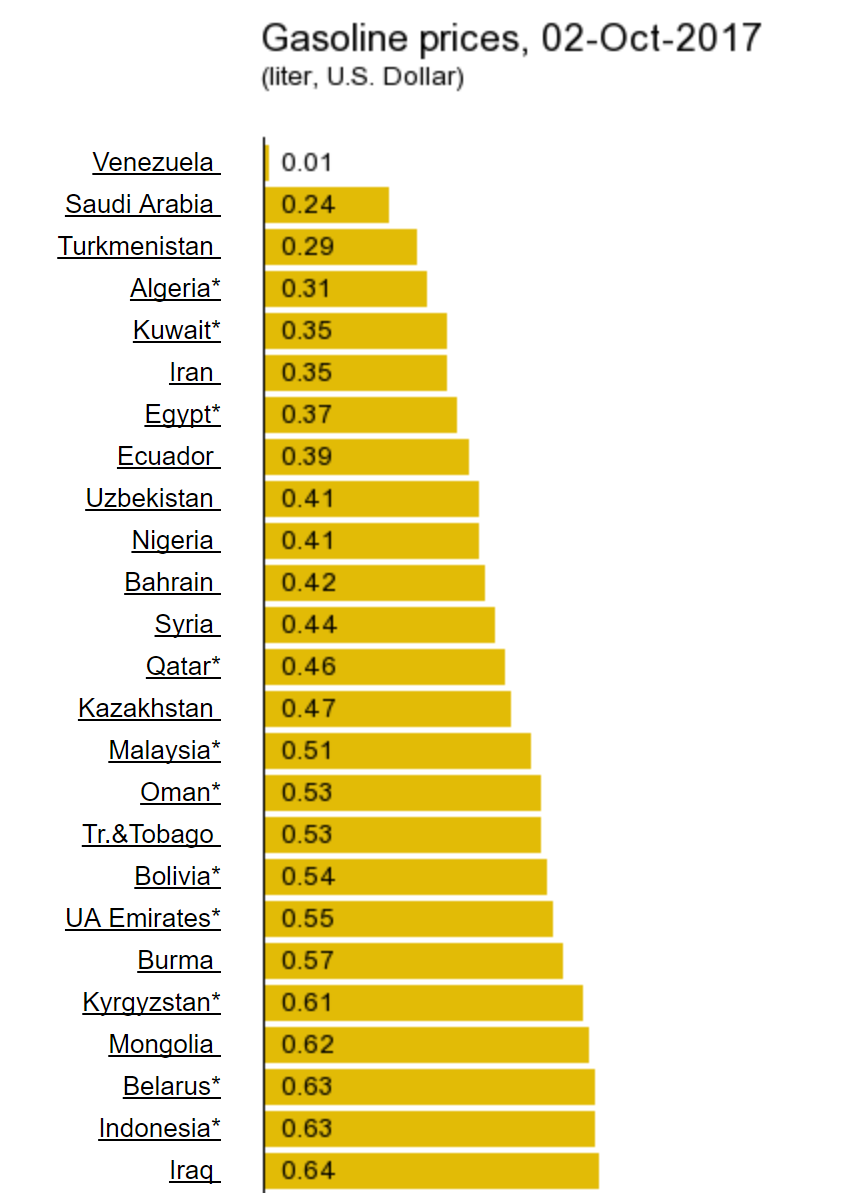

An analogy with other energy exporters makes the point. Do you think that Saudi Arabians pay export net-back for the petrol that they produce? No. In fact, no oil-producing two-bit, one horse, slack-jawed, Borat-run emerging market pays export net-back prices. Look at the local petrol prices for these oil-producing failed states:

But we pay well above export net-back for our gas.

So, the next time you look down your nose at Borat and his mankini just remember that you’re over a barrel in a way that would make him blush.

And is it any wonder? The AFR editorial today is a press release of Big Gas lies:

The political class has a bipartisan consensus on sovereign-risk-inducing, populist gas controls and bashing the big energy producers. But at The Australian Financial Review National Energy Summit yesterday, the gas producers fought back. Santos and Shell – both responsible for massive gas investments in north Queensland – forcefully put the case that Australia’s massive LNG export boom has been responsible for more domestic gas, not less. Export controls now will only crimp future investment in further supply. The problem is the opposite of the popular narrative. Far from gas being sucked up north to be exported, it is now being piped down south to shore up under-investment in Victoria and NSW.

The point is that Australia would be in a much worse gas situation without coal seam gas, and that gas would still be in the ground without the $60 billion to $80 billion in investment that turned Australia into the world’s second biggest LNG exporter. NSW and Victorian state governments, via gas moratoriums or overly restrictive and prescriptive gas restriction regimes, have just made the situation worse, by locking coal seam gas and even conventional gas explorations out of their states. By pushing up gas prices, manufacturing gets hit twice by higher feedstock and electricity prices.

Santos knew it was short of gas when it commissioned its second LNG train. LNG was a massive bubble of mal-investment and we’re all paying huge prices to bail this out.

As well, the AFR’s Energy Summit yesterday was a cavalcade of corruption. The scab grab lurched from LNG carteliers, to a discombobulated government hellbent on saving coal, to an opposition with no balls, to a distracted Alan Finkel and ACCC:

Australia’s Chief Scientist Alan Finkel has vigorously defended his energy review, saying the crisis can be solved within three years and that going back to coal is not the answer.

However, the states and federal governments continue to fight over the right solution to a crisis that is fueling higher power prices and the risk of blackouts during the summer.

The closure of Hazelwood Power Station and Coal Mine in the Latrobe Valley, Victoria, left a massive gap in Victoria’s energy mix. Photo: Arsineh Houspian

Dr Finkel was speaking at an energy summit attended by government and energy industry heads in Sydney on Monday.

Australia’s chief scientist Alan Finkel, who has made a series of recommendations, said adherence to his proposed strategy and policy mechanisms could defuse energy pricing and supply issues.

“Three years from now we expect a full recovery of the energy market,” Dr Finkel said, calling his review ‘Fifty Shades of Finkel’.

“Just going back to coal is not the solution.The revolution is under way, and cannot be stopped,” he said.

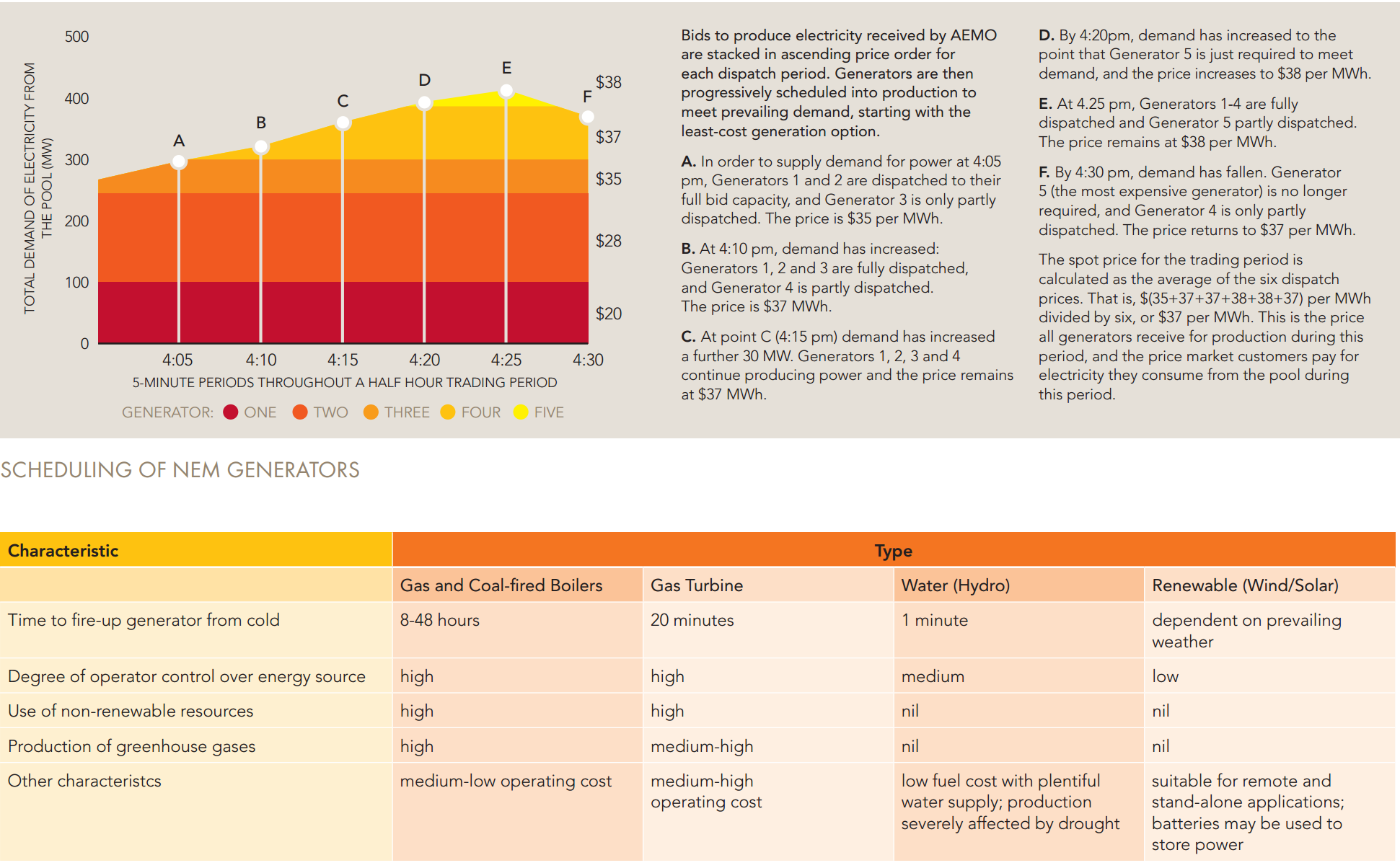

True, sure. But it won’t cure the energy crisis in three years and probably not ten. There is only one thing that will fix it over that time frame. Cheaper gas. It is gas that manufacturing needs and it is gas that sets the marginal cost of wholesale power in the national electricity market, see Australian Energy Market Operator description below:

If you build more generation capacity lower down the AEMO bid stack then the role of gas will diminish. But the gas cartel will simply restrict even more supply. That’s what the cartel does. That’s all it does. With regional LNG prices so low, local gouging is its only profit centre. So, gas will remain expensive and the marginal price setter for power even as the frequency of use diminishes. Ironically it was gas gouger Grant King that was most honest:

Business Council of Australia president Grant King has declared that the Renewable Energy Target should not be abandoned, but also not extended or morphed into a new scheme as the drop in renewable energy costs makes solar and wind competitive.

Mr King said calls for even higher mandated levels of renewables should be abandoned, as renewable energy’s increasing competitiveness means they increase their share of energy supply in any case.

Speaking to The Australian Financial Review ahead of addressing the National Energy Summit, Mr King said the surest way to reduce wholesale prices is to back out higher-priced fuels – black coal and gas – by meeting the 2020 renewable energy target of 33,000 gigawatt-hours as soon as possible.

“The very low marginal cost of renewables would reduce overall wholesale prices through lower fuel costs and lengthening the supply of electricity,” he said.

Mr King said the trend is evident in the forward prices for electricity, where prices are lower in later years after more renewable energy comes into the market, closer to $80 a megawatt-hour from today’s levels of about $100. Accelerating the growth of renewables could mean prices come down even more quickly.

“The irony is that it is going to be meeting the RET as soon as possible that provides the price relief,” Mr King said, adding that to ensure reliability, appropriate incentives would be needed to keep some exiting plants operating for longer.

He said the instructive thing out of the debate over Liddell is that large energy suppliers are saying that by 2022 a combination of renewables, gas and storage will be more cost effective than keeping an old power station in operation.

The problem is $80 is still not cheap. $40-50 is the long term average. The ACCC meanwhile was off with the birds:

Next up the regulators. Deloitte’s Ian Harper is moderating a panel with: Australian Energy Market Commission chairman John Pierce; Australian Energy Regulator Paula Conboy and Australian Competition and Consumer Commission chairman Rod Sims.

Australian Competition and Consumer Commission chair Rod Sims slams NSW privatisation of its power network, saying it had reduced competition and pushed up prices.

“NSW simply sold its assets to the three big incumbents. We didn’t have any improvement in competition,” Mr Sims said.

He said NSW unlike Victoria had prioritised getting the highest price rather than creating a competitive industry structure. “We have had an objective of maximising budget revenue and that’s been very costly.”

Honestly, Rod, who cares? Get on the topic that matters. Fix gas:

- larger domestic reservation with price fixing if necessary;

- harsh lose it or lose it laws for reserves;

- a domestically-focused national gas company to force acquire or expropriate reserves as required and develop them in ways that assuage community anxiety about fracking at the state level, as well as benchmark prices in the market via mandated margins;

- tougher pipeline regulation.

The cartel must be brought to heal with competition and appropriate regulation. It blew an huge bubble of gas mal-investment and we’re all paying to bail it out. That’s really all that there is.