Bartho took up the cause of the LNG giants yesterday:

Shell Australia’s new chair, Zoe Yujnovich, has injected what for some will be an uncomfortable dose of reality into what has been a generally misleading debate about the role that the three big Queensland export LNG plants have played in the east coast energy crisis.

In an address to the national energy summit yesterday, Ms Yujnovich took issue with the widely accepted narrative that exports from the three plants off Gladstone have created a shortage of gas on the east coast and driven a spectacular surge in gas prices for households and manufacturers.

While there’s a strand of truth to that storyline — Santos entered contracts for the sale of LNG that weren’t completely supported by its domestic reserves — it is based on the false premise that had there been no export LNG plants built in Queensland gas would have been available, at a much lower price, to the domestic market.

In reality, if the Shell-owned QGC and Origin Energy and Santos-led consortia hadn’t invested more than $US60 billion to build those plants, it is unlikely the gas reserves that feed them would ever have been developed.

If there was any domestic shortage the price would have risen and the reserves would have been developed. More:

The feed for those plants is coal seam methane, which is more complex and more expensive to extract than conventional onshore gas. Without the massive investment in the plants and the long-term sales contracts to customers in the Asia Pacific region to underwrite it, those reserves may never have been economic because of the scale of expenditure required to exploit them.

Some of the reserves are quite cheap and, as above, if we’d needed the gas then prices would have risen to ensure development. APLNG reserves for instance are much lower all-in cost than our current prices:

It’s no easy matter dis-aggregating capex costs, but according to Oxford, roughly half the $70bn construction cost on Curtis Island was the LNG plants themselves. A second big cost was the construction of the pipelines from the Surat and Bowen Basins to the Gladstone plants. 300-400km pipelines that were all done in triplicate when the gas was virtually sitting on the Wallumbilla Hub south. As the table hows, the actual cost of extraction of the gas is smaller and would have been developed for the local market if needed, at prices far below those of today. More:

Ms Yujnovich addressed the myth that the LNG plants are exporting gas at cheaper prices than those at which they sell gas into the domestic market.

It would be irrational behaviour, if it were true.

The plants have changed the way gas is priced in the domestic market. It is now oil-linked and based on the regional pricing of gas. The domestic price uses Asian benchmarks for LNG, less the costs of shipping and re-gasification. Then there are the costs of transmitting the gas to end-users.

…It would, in any case, be illogical for the LNG exporters, having tied up more than $US60 billion of capital in the plants — and written off multiple billions of those investments — to sell any material volumes of gas to anyone at prices lower than they could obtain elsewhere. They are desperate to improve the returns on their investments.

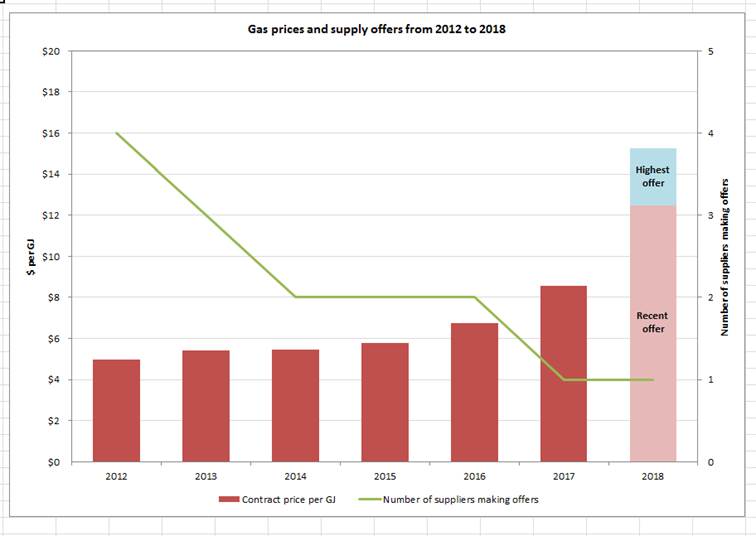

Current prices are not oil-linked, they are far above oil-linkage according to the ACCC:

Net-back prices today are at $8Gj, $10 in VIC, not $12-16Gj and those offers are only down from $20Gj thanks to the minimal gas reservation we’ve so far seen.

As for the “illogical” argument, the cartel has no choice but to fulfill take-or-pay export contracts for most of its volumes. Santos has had to buy half of its gas from third parties to fulfill these obligations, creating the shortage that has driven up local prices.

Thus they can’t divert gas wherever they want chasing higher prices. And why would they want to with the lack of competition anyway? The Gippsland JV (BHP & Exxon) is the only source of gas outside of the Curtis Island cartel. So what they all do is not develop reserves to address the local shortage and enjoy the high prices at home while profit margins crash abroad.

And that’s where it all turns very perverse indeed. When the cost of developing the LNG plants is included, the exports are all made at huge losses. Break-evens are at roughly $14-16Gj and exports are going out at $10Gj. The sunk costs on building the plants keep getting written off, along with accelerating depreciation, which means that the projects have a near permanent tax shelter with which to protect their only actual profits, which are from the domestic sales at much higher prices.

It’s all perfectly rational for the firms to recoup losses on irrational investments in this way. But man, is it irrational for a country to allow it to continue! Every household and business is literally paying a subsidy to a cartel to ship our natural resources to Asia at big losses.

When Banana Republics are studied in future, Australian gas will be chapter one.