Weak wages, falling import prices and fierce retail competition have overwhelmed a spike in energy prices, putting downward pressure on inflation and cruelling prospects of any near-term Reserve Bank of Australia interest rate hike.

Were it not for rising electricity and gas bills, as well as government-mandated “sin tax” hikes on alcohol and tobacco, inflation may have cooled even further below the Reserve Bank’s 2-3 per cent target range.

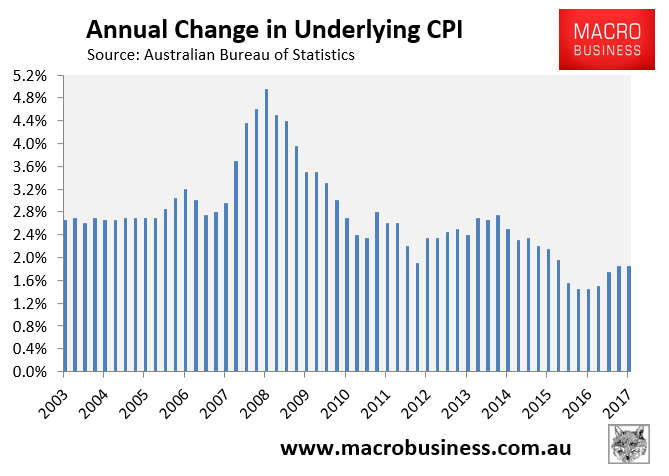

Financial markets and economists were left wrong-footed after official figures showed core inflation growth slowed in the September quarter to 0.3-0.4 per cent from 0.5 per cent in the second quarter. Annual core inflation was little changed near 1.8 to 1.9 per cent.

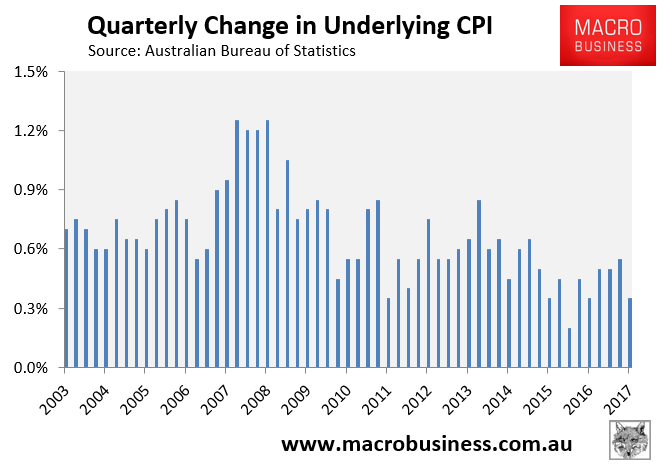

As we know, there ain’t no inflation. We’re in the midst of a suicidal energy shock and we still can’t vault ourselves back into the RBA target band above 2%:

Advertisement

We’ve got little bit of firming in local inflation thanks to the energy shock but it’s going to wash out over the next year as well without leaving a mark. Next QTR sees another 0.4% drop out then two times 0.5%.

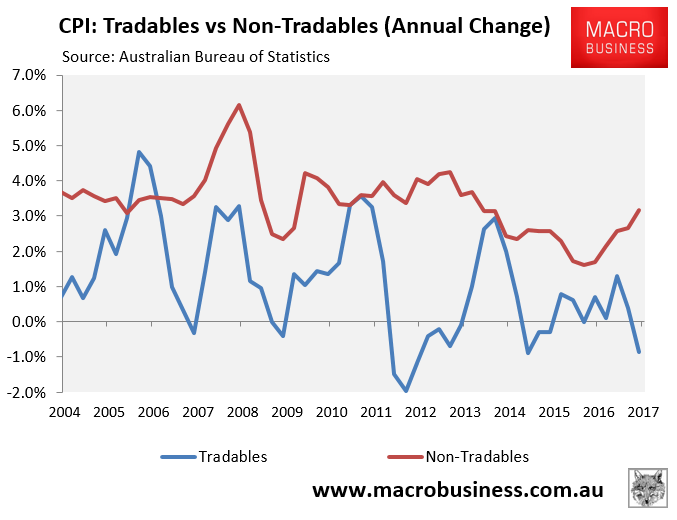

Meanwhile, there is no tradable inflation at all:

Advertisement

The pattern of the two working conversely is also likely to be sustained given how sensitive the currency has become to changes in inflation expectations.

Westpac has some texture:

Housing & tobacco boost the CPI but there is not much else

In the September quarter the components of the CPI came in broadly as we expected which is unusual. Normally, what we see is a significantly different to expected mix of change in components generating an expected aggregate outcome. But in this case our 0.7%qtr on headline inflation and 0.3%qtr forecast for core inflation were both very close to the mark as we most of our component forecasts. Where there were some differences it tended to be on the lower, rather than the higher, side of our estimates. But we do note that holiday travel was a clear exception to this.

ABS estimates a negative seasonality in the June quarter

In the quarter the CPI rose 0.6% for an annual pace of 1.8%yr while the average of the core measures rose 0.4%qtr/1.9%yr. The ABS analysis also confirmed significant seasonality in the September quarter CPI with the seasonally adjusted estimate rising 0.4%qtr which was 0.2ppt lower than the headline estimate. Westpac’s forecast for the seasonally adjusted CPI was also 0.4%qtr.

After trimming the core measures rose 0.4%qtr

The core measures, which are seasonally adjusted and exclude extreme moves, rose broadly as we had expected (0.35%qtr vs our 0.29%qtgr forecast). In the quarter, the trimmed mean gained 0.37% while the weighted median lifted 0.33%, highlighting just how modest the broader inflation picture is outside of housing. The annual pace of the average of the core measures was 1.9%yr, flat on the Q2 print and just a modest acceleration from the recent low of 1.5%yr in 2016 Q4.

More importantly the six month annualised pace of core inflation has dipped below the RBA target band printing 1.9%yr. With revisions, the six month annualised pace has only broken into the RBA target band once in the last two years with a 2.1%yr print in the June quarter 2017.

For a broader core inflation measure, more in line with some international measures, all groups excluding food & energy rose 0.5%qtr/1.3%yr.

Food was weaker but it was due to fruit & vegetables

Food was softer than we expected falling 0.9% but this was mostly due to a larger than expected fall in the very volatile fruit & vegetables (–6.0% worth –0.1ppt compared to our forecast for the headline CPI); we expect this to be reversed in the December quarter. The rise in tobacco prices were a bit stronger than expected (4.1% worth +0.05ppt compared to our forecast) while clothing & footwear fell broadly as expected (–0.9%). The drop in clothing & footwear was broadly in line with the trend seen unfold through the previous three years.

The more interesting story is with housing costs which rose 1.9% vs our expectation 2.6%. Dwelling purchase were a little stronger than we thought they would be (0.8% vs 0.7% expected) but the bigger surprise was the softer than expected rise in utilities (6.8% vs 9.8% forecast). Electricity bills rose just 8.9% vs our forecast of a 13% rise. This smaller than expected rise in utility costs was worth around 0.2ppt on the headline CPI hence this discrepancy explains a large part of why the headline estimate was lower than our 0.7%qtr forecast.

The reported gains in Sydney power bills were a touch softer than we had expected but the key difference was that there was no price adjustment in Melbourne. If Melbourne electricity prices hold to the usual seasonal pattern this suggests we should be looking for a meaningful jump in Melbourne power bills in the March quarter of 2018.

The other surprise for us was there was some upside momentum in recreation with audio visual & computing prices surprising with a 1.2% rise while holiday travel was also stronger rising 1.9% vs our 0.4% forecast. All up this was worth +0.1ppt compared to our forecasts which along with the tobacco provided some of the offset to the 0.2ppt undershoot from utilities. We will be keeping a close eye on this surprising shift in audio visual & computing prices.

Tradable prices are deflating again

Tradables fell 0.3% in the September quarter and breaking it down further tradable goods fell 0.6%, mostly due to fruit & vegetable & auto fuel, while tradeable services rose 3.9% (mostly due to international holidays & travel). The tradables components represent approximately 35% of the CPI.

Non-traded prices, particularly goods, are where you find modest inflationary pressure

Non-tradables rose 1.0% in the September quarter. Non-tradable goods is where there is some modest inflationary pressure and in the September quarter the 2.0% in this series was on the back of rising electricity (8.9%) and tobacco (4.1%) prices. Here we would note two points t; firstly it appears that rising electricity prices are having a bigger impact on margins than overall final goods and services prices; and secondly, the impact in the surge in tobacco prices will be moderated from the December quarter by the reweighting of the CPI which will see a reduction in the effective contribution of tobacco to the CPI. Non-tradable services gained 0.5%qtr with a 2.7% rise in motor vehicle services and 2.6% rise in property rates & charges. Non-tradables represent approximately 65% of the CPI.

Looking forward risks are the Australian economy remains trapped in a low inflation environment

The September quarter continued the run of softer inflation prints as the competitive margin squeeze remains firmly in place. Dwelling costs have lifted a bit and rising power bills are coming through but rent inflation remains very modest. So even with inflationary expectations drifting back towards the long-run average (we suspect power bills are responsible for this) there is little in this release to suggested that the Australian economy is about to break out of its low inflation trap.

For now our forecast see headline inflation peaking at 2.5%yr in the September quarter 2018 but it is important to note that this is based on the current CPI weights. Our preliminary estimates suggest that the reweighting of the CPI could shave between 0.3ppt and 0.4ppts off the annual rate of inflation by end 2018. And just as importantly, given that the run of soft updates point to the Australian economy being in a low inflation trap, we would suggests the risks to the underlying parameters of these forecasts also lie to the downside.

And all of this as the Botox Boom gathers pace with monetary, fiscal and immigration spigots wide open. It only has a few more quarters to run before falling dwelling investment plateaus the labour market again. Moreover, the immigration tap is especially deflationary given it’s greatly undermining wages.

Advertisement

On top of that, the regulatory assault on household debt guarantees house prices won’t trend up further, and that they will need to be deflating at a good clip before interest rates are cut further.

Once that deleveraging starts we’ll see another leg down in non-tradable inflation. Tradable will lift as the dollar keeps falling but even that is likely to be a one-off lift as in 2013/14 given there is nothing upon which it can find traction.

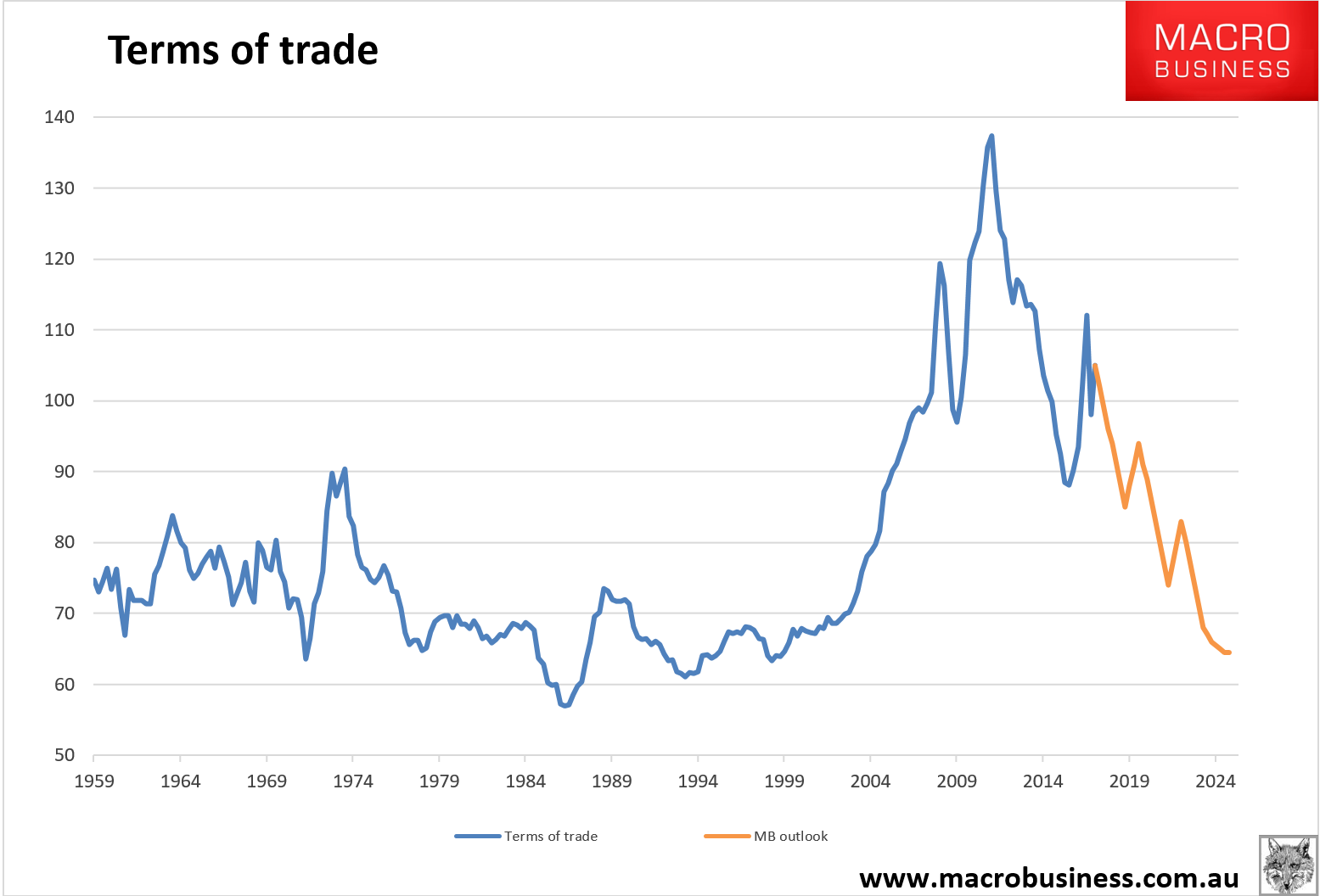

And behind all of that, the great terms of trade unwind has miles yet to run as China steadily stagnates and income is leeched from the economy:

Advertisement

Australia’s future is DEFLATION and then more of the same. As Capital Economics recently said:

We suspect that history will be turned on its head over the next decade or so with Australia and New Zealand experiencing lower inflation rates than some of their peers. It follows that their exchange rates are likely to be weaker than otherwise and that their government bond yields may be lower.

The health of demand will continue to affect inflation, but whether inflation is much higher or much lower over the next decade will mostly depend on the influence of structural forces, such as globalisation and the independence and mandates of the central banks.

At a global level these forces appear consistent with the average inflation rate over the next decade staying close to 2%, but there are likely to be important regional differences. We think that inflation will be highest in the US and lowest in Europe and Japan. In Australia and New Zealand, inflation may gradually drift lower, resulting in it being below 2% on average over the next 15 years. (See our Australia & New Zealand Economics Focus “The new long-term inflation trend”, published on 15th August.)

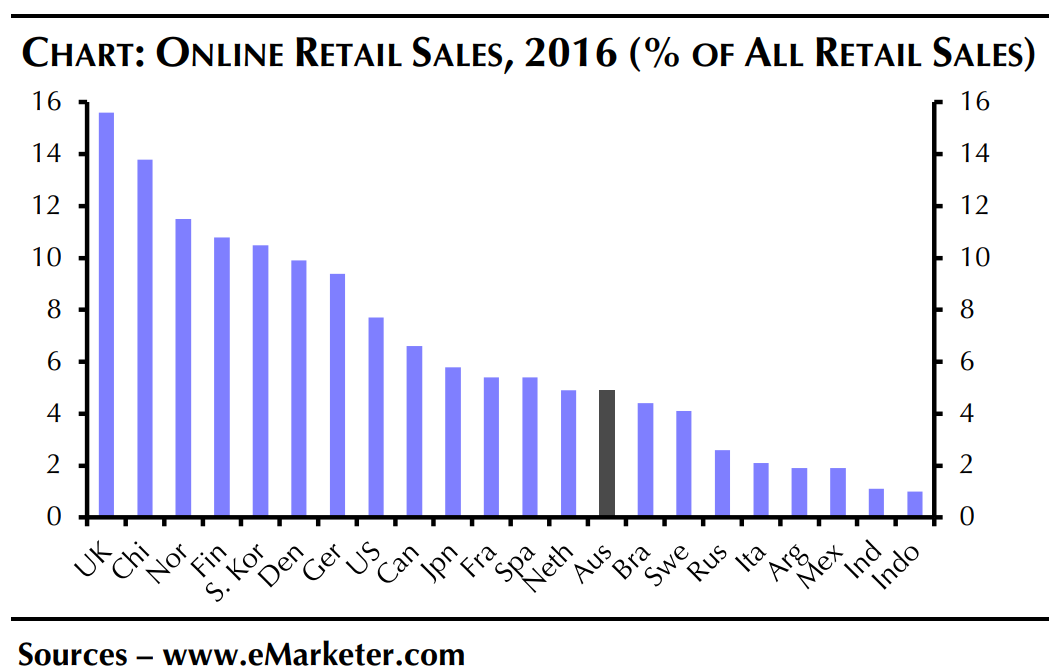

In particular, we think that a further rise in globalisation will reduce inflation in Australia and New Zealand by more than elsewhere. Both countries are keen to strike new trade deals and both are more susceptible to increased competition from foreign firms. Amazon’s plan to open in Australia next year will raise the share of retail sales that takes place online, which is fairly low at present, and lead to more price wars.

And the central banks in Australia and New Zealand will probably place less weight on their inflation targets and more on the risks to financial stability than others. That means they will keep interest rates higher than otherwise.

Low inflation may be a problem in the next downturn. It means there would be a greater risk of deflation. And the lower neutral interest rate means central banks will run out of ammunition sooner. So at some point in the next decade, Australia and New Zealand may have to turn to quantitative easing.

In short, get your money out of here.

Advertisement

———————————————————–

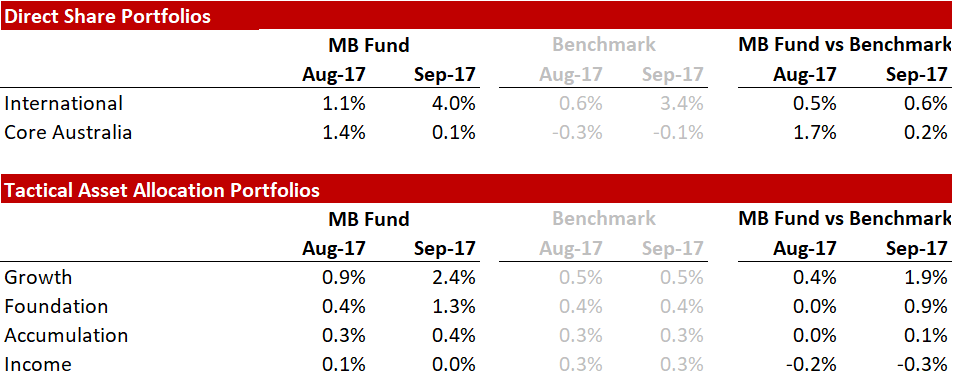

David Llewellyn-Smith is chief strategist at the MB Fund which is currently overweight international equities so he is definitely talking his book.

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October returns are currently around 2% for international and 4% for local shares.

If these themes and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.