USD does not have a compelling story to drive it sustainably in either direction

We think the currency market’s focus needs to shift from being completely USD-centric to focussing on the drivers of risk appetite

That framework dominated before the 2008 crisis, and it will likely dominate once again

With global central banks moving broadly in the same direction (towards tighter policy), we also think that relative monetary policy will drive tactical trading opportunities, rather than strategic trends

Shifting frameworks to focus on the level of aggregate policy accommodation and aggregate growth and using risk appetite rather than the fortunes of the USD as the focal point for FX market forecasting will generate more sustaining and trending outcomes

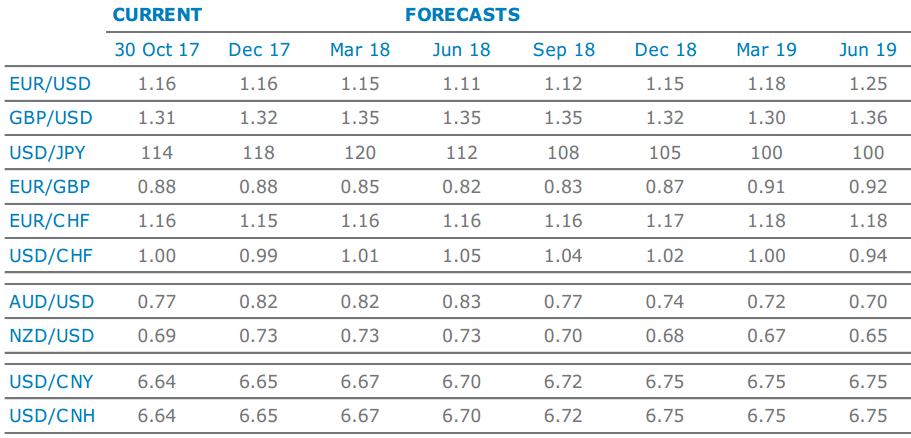

The JPY is set to weaken as USD/JPY pushes back towards 120.

The EUR will also weaken as its low yield means it remains a funding currency.

A cautious cycle from the ECB – which has one eye on the impact that the EUR can have on financial conditions – will also provide a lid.

In the UK, the Bank of England cycle will be shallow and its ability to sustainably support the GBP is limited.

For the AUD and NZD, we continue to look for further strength. Domestic stability, strong global growth, low volatility and attractive valuation should all provide tailwinds.

We have downgraded our forecasts for both the EUR and the JPY and look for further weakness in both from here, particularly against the AUD and NZD.

Amusing stuff. EUR is going to fall but AUD rise. Fat chance.

The EUR forecast looks about right. That by itself will lift USD and DXY nearly 5%. So, the Aussie dollar will have to strengthen by roughly the same amount to remain flat. Then add another 7% to reach 83 cents.

This is an uber-bullish AUD outlook based upon ANZ’s previous notion of five drivers:

Advertisement

USD is due for a correction

Risk sentiment remains supportive

RBA still on track to hike in 2018

Outlook for iron ore remains positive

Technicals bode well

All wrong:

The market is still short USD;

Risk sentiment is one thing, slowing China another;

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.