Some good advice, bad advice from the AFR on stocks over the weekend:

If you’re not invested in global stocks, say the experts, you’re missing out. You’re giving up a much larger exposure to IT, healthcare and other sectors and stocks that are household entities – and therefore big earners on a large scale – in other countries. You’re also saying goodbye to far better potential growth than you’d get just from Australian shares.

Let’s look at what would have happened if you’d invested $1000 in each of the 39 overseas stocks highlighted in Smart Investor Weekend via the Marco Polo global stock pick column for the year to end-September.

While buying individual shares only is not always the wisest option, the 13 per cent return you would have made on these (compared to 4.5 per cent from the ASX/S&P 200 index of the top 200 stocks on the Australian Stock Exchange) highlights the benefits of tapping into markets much more diversified than our own. (Neither of these returns factor in dividends and are based on marked to market capital gains, points out Fat Prophets, which supplies the weekly stock picks.)

Global shares have been outperforming Australian shares since October 2009 (see accompanying table). And it’s likely to continue, says Oliver: “Underlying profit growth at around 5-6 per cent in Australia is well below that in the US (at around 11 per cent) and Europe and Japan (at around 20-30 per cent) so the underperformance of Australian shares may have a while to go yet – which argues for a continuing decent exposure to global shares relative to Australian shares.”

Another reason to seek more global exposure is to mitigate the risks around the domestic property market. “It’s expensive by global standards (notably now in Sydney and Melbourne),” says Oliver, noting that Australians are heavily exposed both directly and via bank and listed property shares in their Australian share market exposure.

And then there are potential currency wins. As you’ll see from the table showing how $1000 invested in each of our weekly Marco Polo global stock picks would have performed, many of those investments would have benefited from fluctuations in the Australian dollar.

He [Oliver] advocates investing, as he does, in a fund that gives global exposure. “Exchange traded funds (ETFs) have made the whole process a lot cheaper and easier, and going down the passive route does make some sense as the US share market dominates global share indices (at over a 50 per cent weight) and it is a hard market for individual fund managers to add value in as it is so analysed by fund managers,” he says. “That said, emerging markets are easier to add value for fund managers and the case to go down an active path there is greater.”

…Europe, Japan and parts of the emerging world (eg Asian shares) look the most promising, says Oliver. “Compared to the US they are all cheaper, are providing stronger earnings growth and mostly (at least in Europe and Japan) have central banks that are yet to start monetary tightening in contrast to the Fed in the US.”

It’s certainly good advice to get offshore with Australia ex-growth and the dollar so high, even if backwards looking media like the AFR has finally figured it out suggesting that we’re closer to the end than the beginning. At some point over the medium term the trade is going to reverse and Australia outperform. Just not yet. First we need a much lower dollar.

In the meantime, where to go and how to do it are the crucial questions. Oliver’s suggestion that Europe and Asia are overweights is wrong. Europe has been OK but is held hostage by the exchange rate. There is an almost one-to-one relationship between its currency and share market moves for Aussie investors which wipes out the gains (and losses), unless you’re stock picking can outdo the index.

Advertisement

Emerging Asia may be cheaper but it rises and falls on fundamentals with China which is going to slow materially in 2018. And on forex, it rises and falls conversely with the USD. So you also have to believe that the USD will fall to buy Asia (again if you’re not stock picking). And if that happens, again, the AUD will hurt your gains.

On the other hand, the US may be expensive but that’s for a good reason. Profits are high, margins are good, the forex trend is your friend and the macro tailwinds are obvious:

a lower currency for the past year set to rise;

low interest rates, a slow Fed and low mortgage rates;

hurricane reconstruction;

tightening labour market and slowly firming wages;

tax reform;

hurricane reconstruction, and

firm shale activity.

Advertisement

Exposure to the US economy remains the pick.

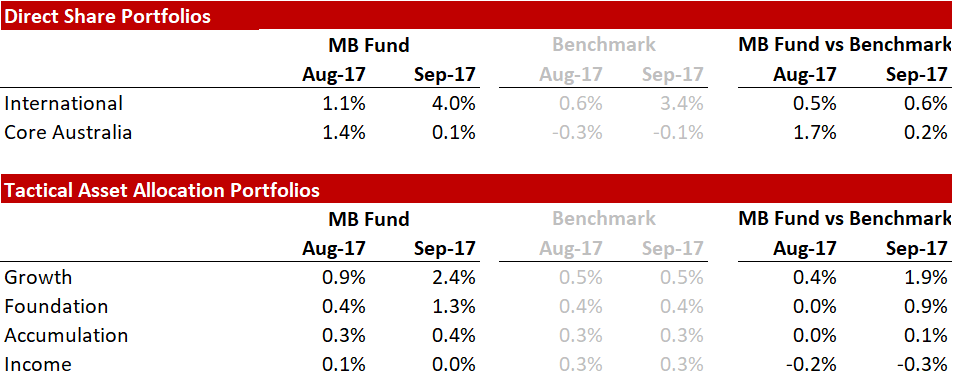

David Llewellyn-Smith is chief strategist at the MB Fund so he is talking his book. At the MB Fund we’re over-weight the US with good exposure to Europe and Japan:

Advertisement

The fund’s first two months of performance was good in absolute and relative terms (full report here):

So far in October, Growth, International and Aussie portfolios are up roughly an additional 2% apiece.

Advertisement

If you’re interested in the fund, register now and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Chief investment officer, Damien Klassen, is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.