Our economic forecasts (see NZEP 8 September) reflect our base-case scenario election outcome i.e. that the National Party will form a government with the support of NZ First (see NZEP 1 September). While there could also be potential ramifications for the economic outlook from such a coalition arrangement, the implications of a change to a Labour-led government are likely more material. If a Labour-led government is made up of Labour, Greens and NZ First, then (from a macro-economic perspective) some basic features are likely to be:

• Monetary policy: Add maintaining full employment to the RBNZ’s mandate; move to a decision-making committee (see NZEP 25 August); and potentially add a new clause to the PTA requiring the RBNZ to have regard to the desirability of a ‘competitive’ exchange rate.

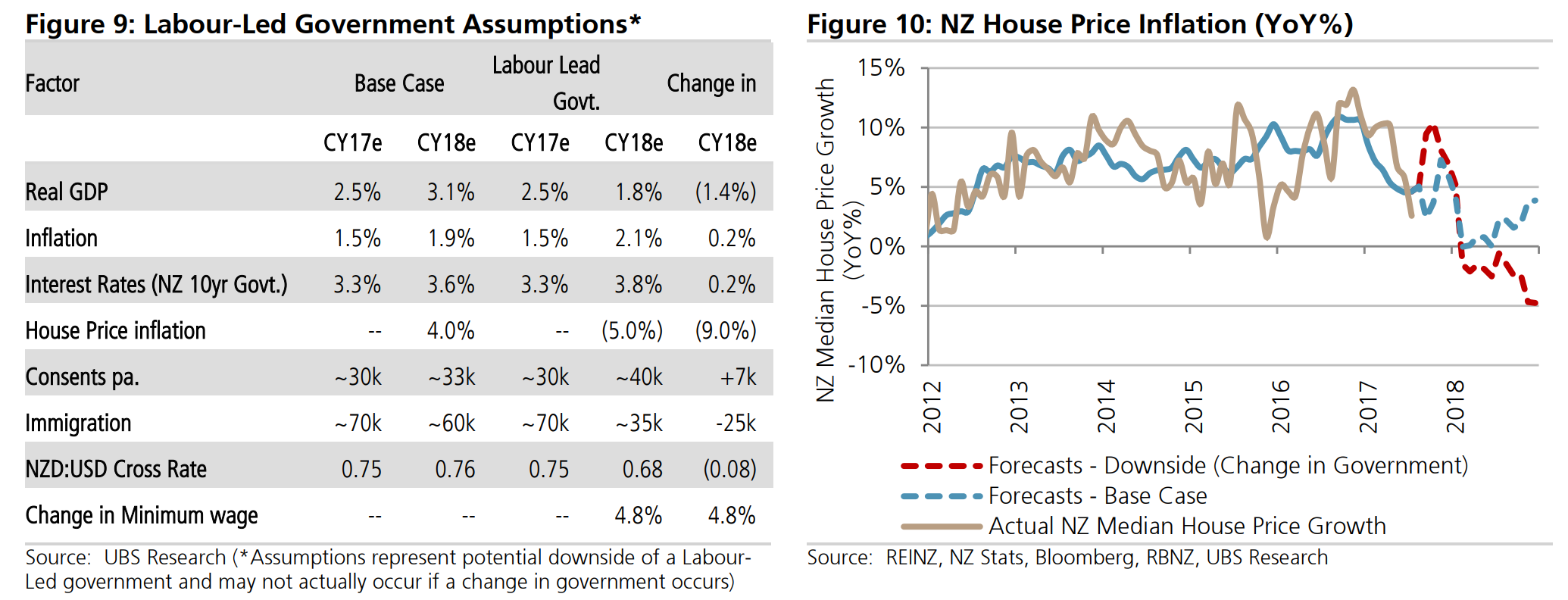

• Taxation: Cancel the tax relief announced in this year’s Budget, which was due to come into effect on 1 April next year, and re-direct to planned spending priorities. Labour also plan to add a levy to commercial water usage, tax overseas visitors and allow councils to impose regional fuel taxes.

• Fiscal policy: Planning to run lower fiscal surpluses than the current government projections (see PREFU), which will mean a higher path for government debt.

• Immigration: All three parties favour lower immigration, so more a question of degree and timeframes. Labour aims to reduce immigration by 20-30k pa, which would cut roughly ½% from population growth.

Growth: In the very near term, growth may be dampened if business confidence deteriorates, although the export sector may receive a boost from a lower exchange rate (see next section). Lower immigration will likely undermine the already capacity-constrained construction sector, despite the Labour Party’s plan to build an extra 100k houses over the next 10 years, and also aggravate labour shortages in other sectors. The latter could also be exacerbated by the absence of a labour market supply-side response that was anticipated with the planned tax cuts. Longer term, higher tax burdens, a weaker housing market, and less focus on securing external trade agreements could also subdue potential growth. Real GDP growth could be ½-1% lower on average over the next few years.

Inflation: The initial impact on CPI inflation could come via a lower exchange rate and higher tradable inflation. Beyond that, labour market outcomes would be critical, with labour shortages finally spilling over into wage pressures, fuelled by higher headline inflation and moves to raise the minimum wage and introduce a ‘Living Wage’ for workers in the core public service. Proposed changes to industrial relations, including ‘Fair Pay Agreements’, and additional business costs (like the water tax), may also add to inflationary pressures over time.

Interest rates: With the labour market still expected to be stretched, and a lower exchange rate probable, the RBNZ will still be facing the need to respond to higher inflationary pressures, despite the likely changes to the framework. Thus, short rates will likely rise earlier, and faster, than would otherwise have been the case. Along with higher government debt, this prospect suggests that interest rates across the curve will be higher should the government change post-election.

We can’t entirely isolate the immigration cuts in terms of outcomes but the conclusions are right:

higher wages and inflation;

lower currency, and

lower house prices.

Higher interest rates are perhaps a consequence of this but not necessarily depending on how heavily falling asset values weigh on consumption. UBS doesn’t discuss productivity but I’d guess it would be higher over time as infrastructure is de-bottlenecked.

Advertisement

NZ’s labour market is tighter than Australia’s though its wage growth is just as weak so if you were to do the same here then the we’d see the same mix of impacts but on a more muted basis.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.